What is sector investing?

Key takeaway

Sector investing empowers investors to pursue specialized growth themes and adapt portfolio allocations to changing market dynamics, providing access to potential outperformers while offering a balance between diversification and focused exposure.

Table of contents

- What is sector investing?

- Diversifying with sectors: Capture upside potential while limiting single-stock risk

- What is the GICS® framework?

- What are the 11 GICS® sectors?

- How do different sectors react to economic changes?

- What are sector funds?

- Consider ETFs for cost-effective, targeted exposure to sectors

What is sector investing?

Sector investing is the strategy of allocating capital to specific segments of the economy rather than investing in individual stocks of companies or more broadly diversifying across the entire S&P 500® market. For investors, allocating to distinct segments of the economy—like technology, energy, or health care—can be an important part of a longer-term strategy for gaining strategic exposure that can complement a core portfolio. Alternatively, sector investing can be used more tactically to provide shorter-term tilts in response to changing economic or business conditions, allowing investors to tailor allocations to pursue customized investment objectives.

From a portfolio construction perspective, different sectors typically react in distinct ways to shifts in macroeconomic conditions, changes in interest rates, and fluctuations in market or business cycles. This creates a dynamic that can support investors looking to adjust portfolio exposures without relying on individual stock selection or trying to predict which single company will outperform. And rather than owning every part of the market based on their market cap, sector investing allows investors to optimize exposures and target specific objectives which include:

- Pursuing alpha across top performing growth sectors

- Expressing a macro view and diversifying to reduce concentration or company-specific risk

- Aligning portfolios with changing economic and business cycles or trends

Diversifying with sectors: Capture upside potential while limiting single-stock risk

Sector investing offers the potential for above-market returns, but without the single-stock risk and intensive company research required with individual stock selection. However, while sector investing can help reduce single-stock or individual industry risk, it does not entirely remove concentration risk as sectors represent companies performing similar business activities, making sector investing less diversified than investing across the entire market.

Sector investing does allow investors to tailor their objectives and optimize goals by gaining exposure to sector-leading companies and outperformance potential, often without the same level of drawdown risk as single industries or individual companies.

Comparing the return, risk, and downside of the S&P 500® Technology Index to the semiconductor industry (which comprises 44% of the Tech sector)1 and the constituent stocks within the S&P 500® Technology Index over the past 10 years underscores the diversification benefits of sector exposure to growth with significantly less drawdown risk (Figure 1).

As one of today’s growth themes, the Tech sector has outperformed the broad market by 8.79% on an annualized basis over the past 10 years,2 providing investors exposure to upside potential. While semiconductors historically were the clear performance leader at the industry level, outperforming the broader Tech sector by 10.4% annualized over the past decade, semiconductors have a volatility that is 1.4x greater than Tech and a larger maximum drawdown of 43%, compared to a lower drawdown of 31% for the Tech sector, and 23% for the broader S&P 500® market.3 In terms of individual stock selection represented by the constituent average, Tech Index returns outperformed the average constituent return by more than 3.5%, preserving relative upside for investors, while mitigating drawdown risk by ~20% relative to the constituent average drawdown of ~52%.

What is the GICS® framework?

Global Industry Classification Standard (GICS®) is an industry-wide classification framework developed in 1999 by MSCI and S&P Dow Jones Indices. The GICS® framework provides a universal, consistent way for investors to classify and group the business activities of public companies worldwide.

The GICS® structure is made up of four hierarchical components, with sectors sitting at the top, and includes:

- 11 Sectors

- 25 Industry groups

- 74 Industries

- 163 Sub-industries

Companies are categorized based on their principal business activity, which is primarily based on revenues, but also includes earnings and market perception. Thereafter, based on a company’s principal business activity, it is assigned to one of the 163 sub-industries, which subsequently determines the company’s membership in one of the 74 industries, followed by one of the 25 industry groups, and finally one of the 11 GICS® sectors.

Company classifications are reviewed annually to ensure the framework and company categorizations appropriately represent the evolution within global equity markets. For example, after lengthy consultation with market participants, the Telecommunications sector was broadened and renamed to Communication Services in September 2018 to include media, entertainment, and interactive services companies such as Electronic Arts, Alphabet, and Meta Platforms. The change reflected digital transformation in the way people communicate and access information by integrating telecom, media, and social platform companies into a single sector.

What are the 11 GICS® sectors?

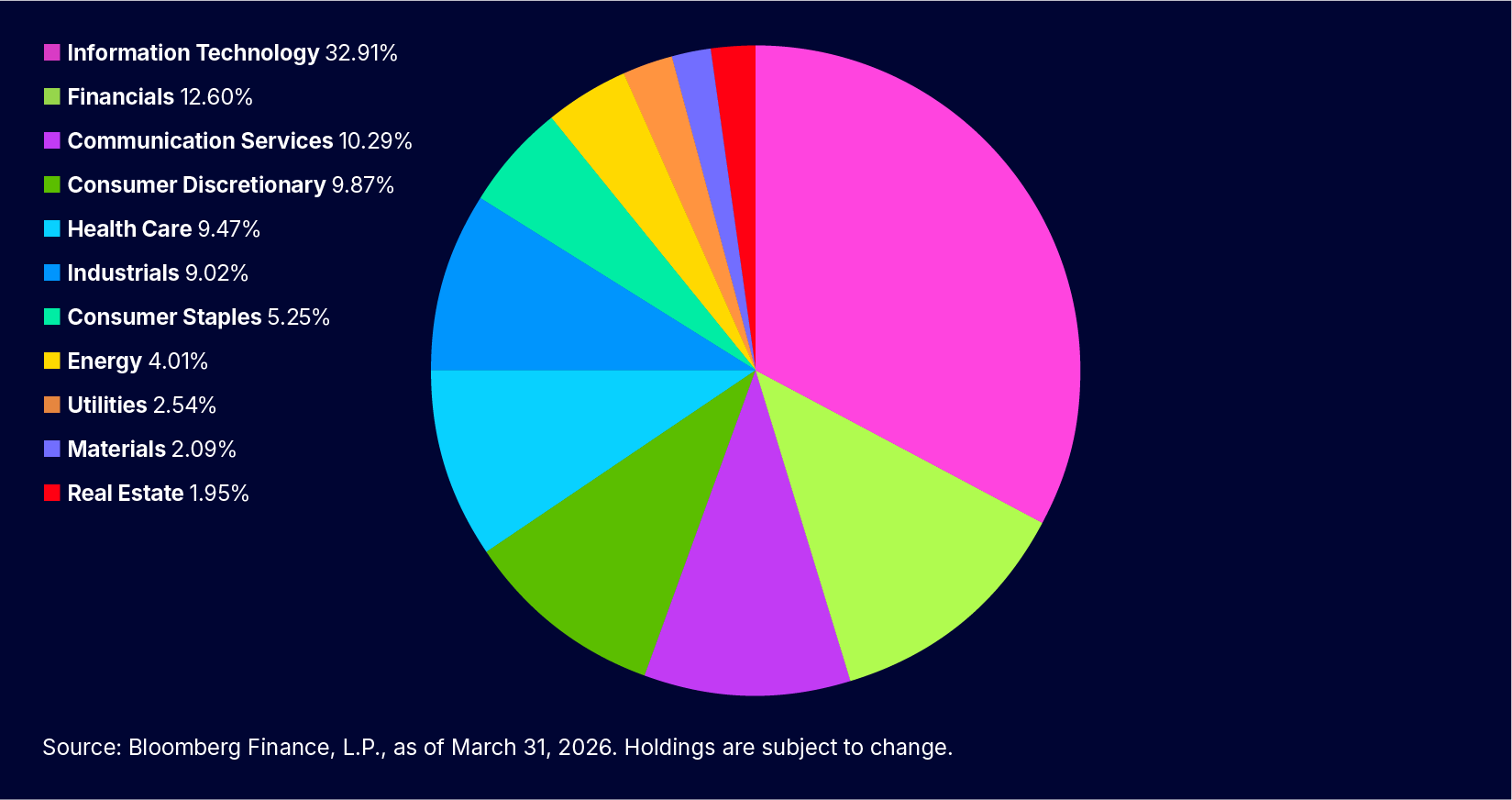

The 11 GICS® sectors represent a broad categorization of companies making up broad equity markets, such as S&P 500® and MSCI All Country World Indices. Currently, the S&P 500® includes weighted exposure to each of the 11 GICS® sectors, with Information Technology making up nearly a third of its weight.

Figure 2: S&P 500® weighting by sector

Let’s look more closely at each sector, including the types of industries that make it up, and some examples of the businesses whose activities fall within the sector. There may be a few surprises. Select + to explore more about each sector.

How do different sectors react to economic changes?

The 11 sectors tend to respond differently to changing macro-economic conditions, interest rates, inflation, and market and business cycles, making broader market analysis a key consideration for sector investors and their asset allocation strategies.

The Information Technology and Communication Services sectors’ sensitivity to business cycles is nuanced. The two sectors have secular industry trends and/or technological shifts that generally are less influenced by cyclical economic developments, and that may exist throughout multiple cycles to shape each sector’s growth trajectory. More specifically, Information Technology tends to benefit from long-term structural growth rather than short-term demand cycles.

Alternatively, cyclical sectors such as Financials and Consumer Discretionary tend to track the business cycle and be positive during periods of recovery and expansion when economic growth accelerates, business and consumer confidence are strong, and companies are replenishing their inventories. In contrast, these sectors can face headwinds during periods of growth slowdowns when monetary policy can become more restrictive in an effort to steer the economy away from overheating in the later part of the economic cycle.

Non-cyclical sectors, or defensive sectors, such as Consumer Staples, Utilities, and Health Care, generally perform well during slowdowns and recessionary periods. These businesses are typically less sensitive to economic fluctuations where products and services are tied to non-discretionary, essential spending by consumers.

What are sector funds?

Sector funds are pooled investment vehicles—most commonly ETFs or mutual funds—that focus on a specific segment of the economy, such as technology, healthcare, financials, energy, or utilities. Instead of investing across the entire stock market, or in individual securities, sector ETFs and funds target broad segments with shared economic characteristics and similar business activities and revenues. Sectors are typically grouped using standardized industry classifications, including the GICS® framework described earlier, which underpins most US sector mutual funds and ETFs.

Sector ETFs and funds help investors efficiently and cost-effectively capitalize on growth trends across broad segments of the economy—versus a narrower, single-industry exposure, or a thematic approach. Today’s investors can choose from sector, industry, or thematic ETFs and funds to express their views, but it is important to understand the differences across the broad categories and the different vehicles. ETFs and mutual funds each have their own unique costs, risks, and liquidity profile, and can play a distinct role in constructing portfolios.

From a broader category perspective, sector ETFs and funds look at macro, fundamental, and technical trends driving market performance and opportunities across a broad segment of the economy like technology or energy. Industry funds offer more concentrated and specialized exposure to a narrower group of companies that offer similar products or services (e.g., semiconductor companies within the Tech sector), and thematic funds typically aim to tap into innovative and emerging social or technological trends with more specific, yet subjective, definitions of the exposure.

Of course, how you select your sector, industry, or thematic exposures depends on both your investment goals and risk tolerance. And keep in mind that the size of your positions and rebalancing schedule will be more critical in managing industry or thematic exposures than in managing sectors, given industry funds’ narrower exposure and thematic funds’ greater uncertainty around the path of new technological developments.

Consider ETFs for cost-effective, targeted exposure to sectors

Sector investing offers investors a flexible way to tailor their portfolios—whether to pursue growth opportunities, manage risk, or align investments with economic and market trends.

Sector ETFs provide a cost-effective solution for enhancing the core of a portfolio by providing broad exposure to potential alpha generating opportunities while reducing the cost and risks associated with individual stock selection or single-industry concentration.

While sector investing does not eliminate market risk, sector ETFs can serve as a valuable tool when used thoughtfully alongside a diversified core portfolio. Understanding how sectors behave across different market environments can help investors make more informed allocation decisions and build portfolios that reflect both their long-term and shorter-term tactical objectives.

State Street launched the first sector suite in 1998. Today, the State Street® Select Sector SPDR® ETF suite covers all 11 GICS® sectors and is the largest suite, with $342 billion in assets under management (AUM) as of March 31, 2026.4 The suite also boasts the lowest expense ratios, tightest spreads, and highest options volume among similar US sector ETF suites for those seeking liquidity and option income generating strategies.5