What’s next for ETFs? 3 predictions that could shape the industry’s future

ETFs now represent a meaningful share of global investable assets—14% as of December 2025.1 But their next chapter may be even more transformative thanks to wider adoption, new use cases, and more innovative products. What’s on the horizon? Keep reading to find out.

More than 30 years after State Street Investment Management launched the first US-listed ETF, the conversation is no longer just about adoption. Rather, it’s about how far the industry can go, how investors will use ETFs differently, and what role they will ultimately play in shaping portfolios.

Here are three key predictions that could define the next era of ETF growth—made in our ETF Impact Report 2026-2027 by State Street Investment Management’s Chief Investment Strategist Michael Arone and Global Head of Research Strategists Matthew Bartolini.

1. 10-year ETF AUM growth will exceed our projection from last year

The ETF industry has already grown at a remarkable pace. But the next phase of growth could compound faster than we originally anticipated.

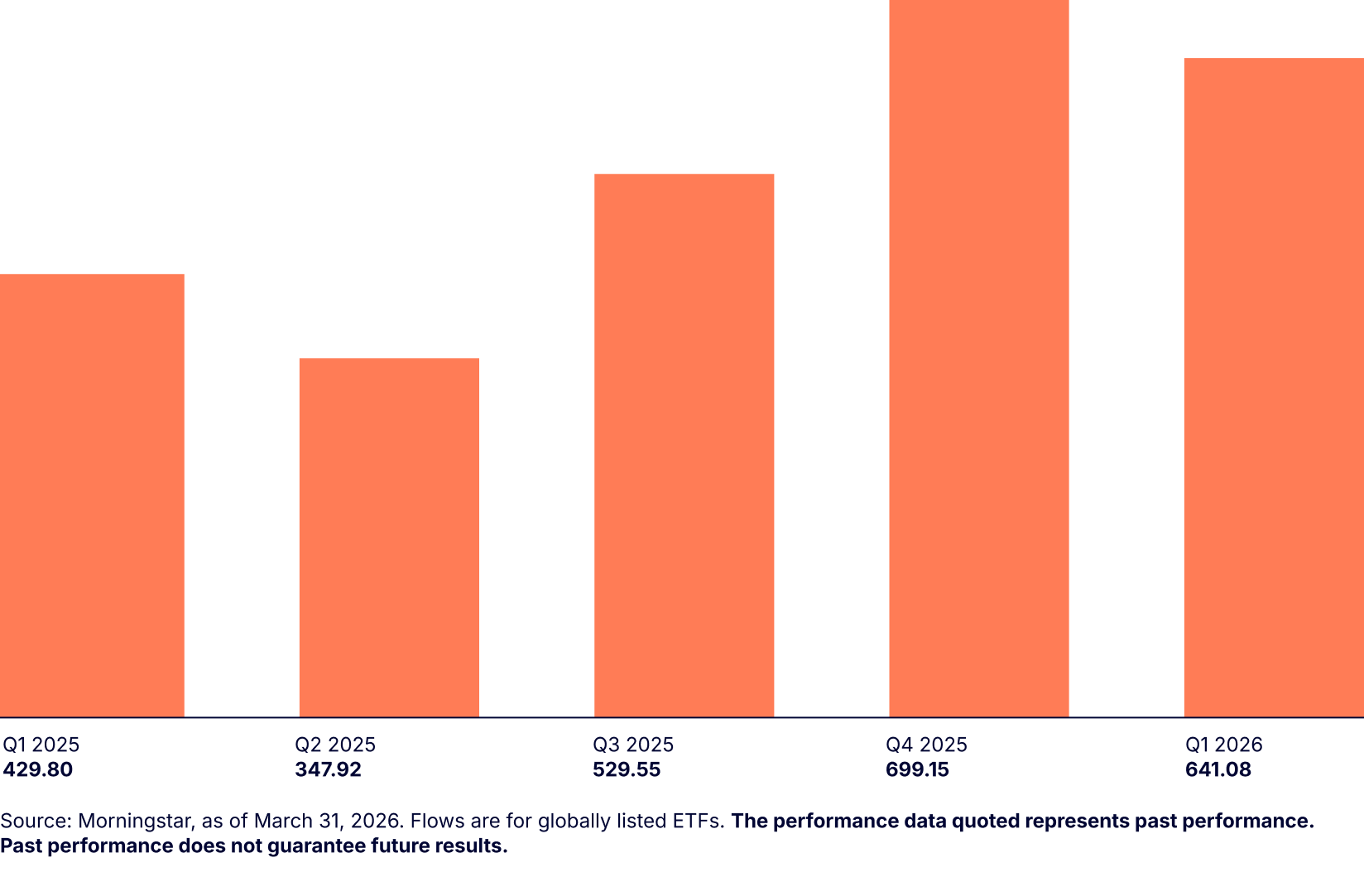

Globally, ETFs took in a record $2 trillion in inflows last year, vastly outpacing 2024’s then-record $1.48 trillion.2 December 2025 alone brought in $288 billion.3 And 2025’s fourth quarter accounted for $699 billion, triple the Q4 average of $207 billion.4 By year-end, global ETF assets under management (AUM) had surged to more than $18 trillion.5

This year, momentum has continued. The first quarter brought in $641 billion, $211 billion above the previous Q1 record (Figure 1),6 even as markets faced heightened volatility and geopolitical uncertainty.

Figure 1: Global ETF flows by quarter ($, billion)

When inflows hold up under those conditions, it underscores the structural role ETFs now play in portfolios. They’ve become the vehicle investors rely on to adjust exposure, manage risk, and maintain strategic allocations across market conditions.

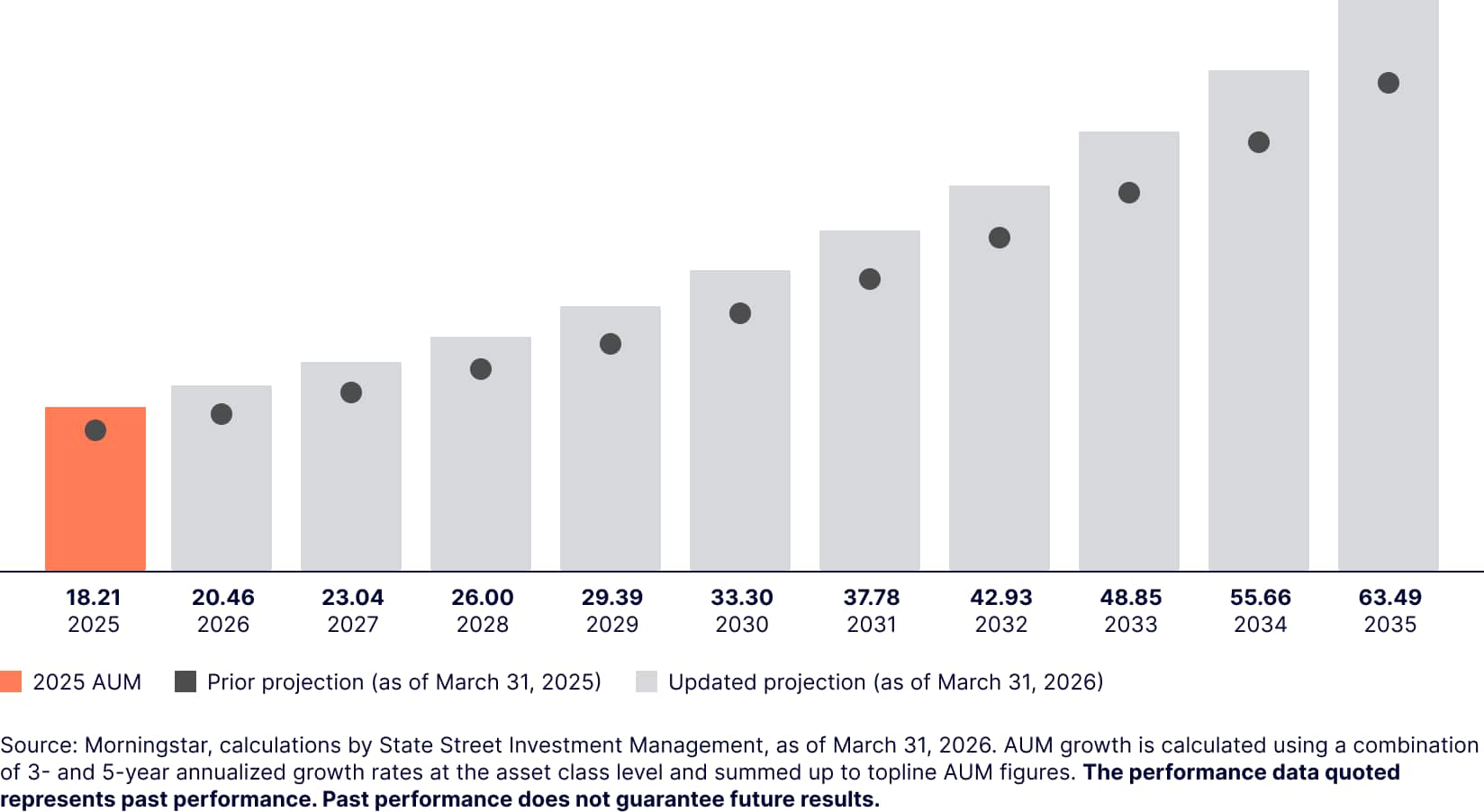

That adds conviction to our forecast from last year: global ETF AUM will reach $54 trillion by 2035. With inflows now on pace to exceed that target by 18%,7 it may be that our estimate wasn’t bold enough (Figure 2). In fact, we now predict that global ETF AUM will reach $63.49 trillion in 2035.8

Figure 2: Global ETF AUM growth is outpacing our original expectations by nearly 18% ($ trillions)

Last year’s 10-year projection versus this year’s updated forecast

Why this matters:

ETF growth is no longer just steady—it’s compounding. Scaling assets at this level reflects:

Broader adoption across investors

Deeper integration into portfolios

Continued innovation in the ETF structure

2. ETFs will soon become a household name for retail investors

For years, ETFs have steadily gained traction—but adoption remains uneven across investor segments.

That’s changing.

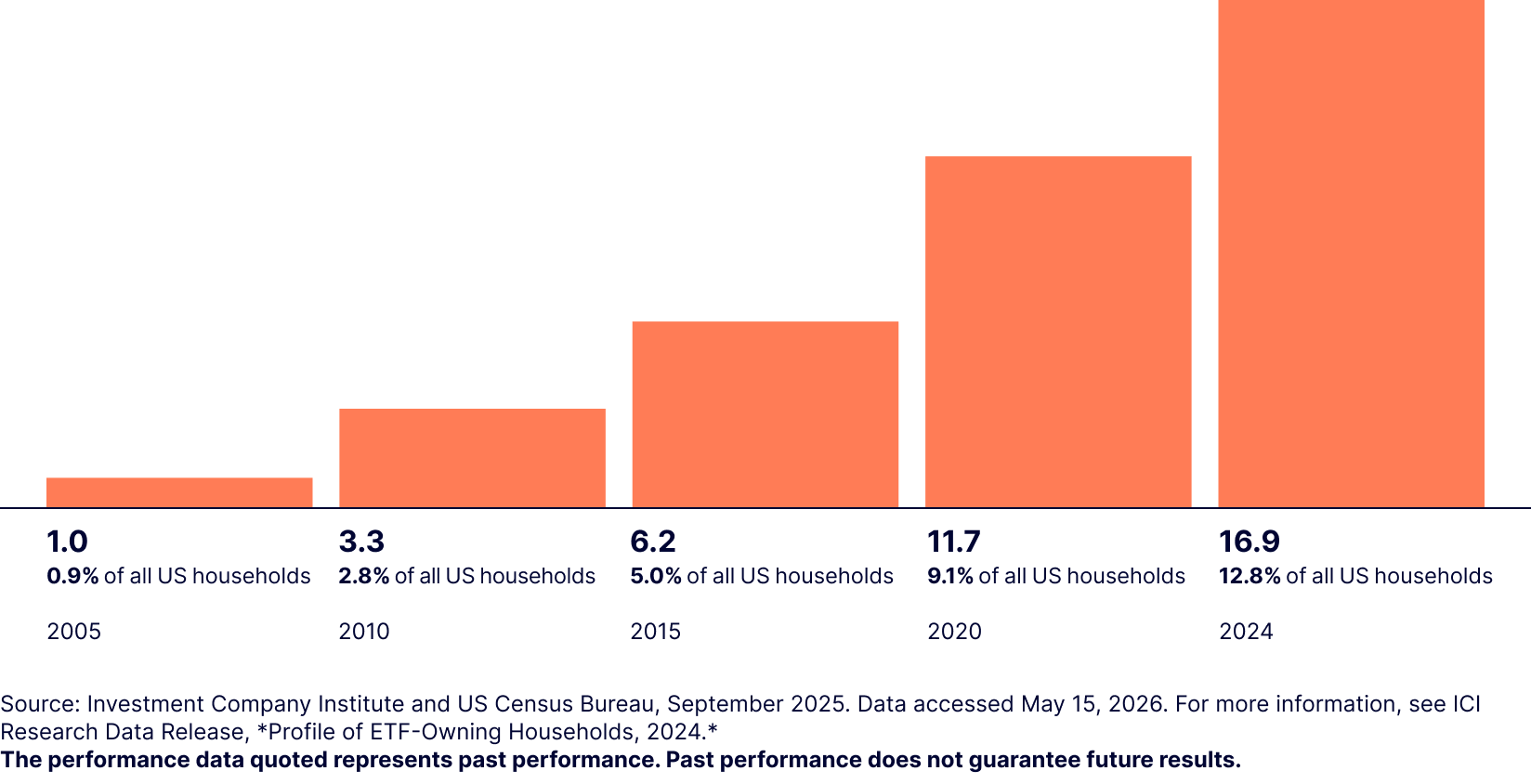

As ETF adoption expands across generations, new investors are entering the market already familiar with the structure (Figure 3). As a result, ETFs may become as recognizable to retail investors as mutual funds are today, with ETF knowledge becoming a standard part of investing literacy.

Figure 3: ETF adoption has surged among US households

Number of US households owning ETFs (millions)

A combination of factors is driving this shift:

- Digital-first investing platforms

- Lower barriers to entry

- Generational wealth transfer

- Growing integration of ETFs into long-term savings vehicles

Why this matters:

ETF growth isn’t just about assets—it’s about mindshare. As familiarity increases, ETFs likely will move from “just another investment option” to the default investment vehicle in modern portfolios.

“The next chapter of this industry’s growth is being written by everyday investors opening brokerage accounts on their phones to help build long-term wealth. It’s all fueled by an ETF structure that’s simple enough to be intuitive, yet robust enough to scale across generations.

And with Trump Accounts, long-term, tax-advantaged vehicles designed to jump-start investing for children, ETFs could shape how an entire generation experiences investing from the very beginning.”

- Matthew Bartolini, Global Head of Research Strategists

What else are we predicting for the growing ETF market?

Explore top trends and our bold predictions for the future in our latest ETF Impact Report.

3. The role of ETFs will continue to evolve from owning the market to engineering outcomes

Perhaps the most important shift in the ETF industry isn’t how much it’s growing—but how ETFs are being used. In the past, investors turned to ETFs primarily to gain exposure to markets, asking questions like “What benchmark do I want to own?” and “What index do I want to track?”

Today, the question is changing to “What outcome do I need?”

Investors are increasingly using ETFs to pursue specific goals—such as income, diversification, or downside protection—rather than simply tracking markets.

This shift is driving a new generation of ETF innovation, including:

- Defined outcome strategies

- Options-based approaches

- Multi-asset and income-focused solutions

- Alternative exposures

As a result, ETFs continue to expand beyond traditional indexing, making a broad range of strategies once reserved for institutional investors more accessible to individual investors pursuing specific portfolio outcomes.

“Investors initially used ETFs to own the market. Now they’re using them as tools to achieve specific outcomes.

That shift has expanded the ETF toolkit. Today, ETFs have increasingly become the delivery vehicle for strategies once reserved for institutional and high net-worth investors—ranging from options-based strategies, defined-outcome products, derivative income structures, multi-asset class strategies, real assets, and alternatives.”

- Michael Arone, Chief Investment Strategist

The next chapter of ETF growth is on the horizon

The ETF industry is entering a new phase—defined not just by scale, but by how deeply ETFs are embedded in the way investors build portfolios.

With accelerating asset growth, rising investor familiarity, and a shift toward outcome-oriented investing, ETFs are positioned to play an even more central role in the future of investing.

What’s next for ETFs?

Get top ETF trends and our bold predictions for the future of ETF growth inside our ETF Impact Report 2026-2027.