The new era of income investing How to design income portfolios beyond traditional stocks and bonds

The World Health Organization forecasts that by 2030, one in six people in the world will be 60 years-old or older.1 Meanwhile, roughly one in five Americans will be at or above retirement age.2 That demographic reality is reshaping one of the most fundamental questions investors face: how to convert portfolios built for growth into reliable, repeatable cash flow.

Sections at a glance

- Why yesterday’s income playbook no longer works

- From yield to outcomes: Why income investing had to change

- Income differs by level, plus source, stability, and sensitivity

- Beyond bonds: An expanded income toolkit reshapes portfolio construction

- Higher yield doesn’t always mean higher return

- Fixed income: Engineering cash flow with precision

- Equities: Income as a complement to growth—not a substitute

- Tradeoffs of pursuing greater cash flow with alternatives and hybrids

- Newer tools for income design

- From generating income to delivering income outcomes

- The future of income investing: Designed, diversified, and deliberate

For decades, income investing followed a relatively straightforward blueprint. Bonds—through predictable coupon payments—served as the primary source of portfolio income, while equities supplied growth. Within this framework, income was largely synonymous with yield, and portfolio construction centered on allocating between asset classes assumed to play clearly defined roles.

But that model is increasingly insufficient. Income is no longer defined by bonds alone, and durable outcomes now require multiple levers across fixed income and equities, deployed intentionally within a portfolio framework.

Why yesterday’s income playbook no longer works

The rising demand for dependable income is colliding with structural changes in both equity and bond markets that have quietly eroded the effectiveness of traditional income frameworks.

Most pressing, on the equity side, income generation has declined as US markets have become increasingly concentrated—both geographically and by sector. A growing share of market capitalization now resides in high-growth companies and sectors that emphasize reinvestment over cash distribution. Technology, in particular, has become a dominant driver of equity returns while contributing relatively little to portfolio income.

At the same time, corporate capital allocation has shifted meaningfully away from dividends toward share buybacks and internal investment. Rather than returning cash directly to shareholders, many firms have prioritized capital expenditure, balance-sheet flexibility, and free-cash-flow–driven growth. While this shift has supported strong price appreciation, it has reduced the role of dividends as a reliable source of income—especially for US-centric equity allocations.

Fixed income, historically the backbone of portfolio income, has faced a different but equally important structural change. Compared with the high-rate environments of the 1970s, 1980s, and early 1990s, the past few decades have been characterized by persistently lower policy rates and bond yields. While declining rates supported bond prices and total returns, they also steadily compressed the level of income bonds could deliver—eroding their role as a reliable source of portfolio cash flow.

Together, these shifts have led to a pronounced decline in income from conventional-stock bond allocations. The yield of a traditional 60/40 portfolio fell from 5.7% in January 1990 to just 2.5% by May 2026 (Figure 1).3 And it has not been meaningfully above 3% since 2009, while yielding below the rate on cash every month since 2022.4

Moreover, at a 2.5% yield, the traditional portfolio is below that of the rate of inflation for developed economies over the past 12 months.5 This negative real income trend has been in place every month for the past five years and may continue given the forward-looking consensus inflation expectations call for inflation to average 2.9% over the next three years.6

This underscores why income investing has had to evolve beyond its historical foundations.

From yield to outcomes: Why income investing had to change

Against this backdrop, four forces have accelerated the need to rethink income investing.

- Substantially higher long-term returns generated by equities over the past half century: This raised a persistent question—was the certainty of bond income worth sacrificing the potential for capital appreciation? This pushed investors into equities, namely US equities, to seek higher returns, which pushed prices up and yields down based on the inverse relationship between the two.

- Companies’ shift in the return of shareholder value: Within US equities, buybacks now consistently outpace dividends, lowering the immediate cash inflow return to investors.

- The shifting relationship between policy rates, economic cycles, and bond income: Historically, policy rates have moved in response to growth and inflation—but the income generated by bonds has not always kept pace with investor needs. During periods of high inflation and/or high growth, policy rates become more restrictive and core bonds tend to yield as much as or less than cash (e.g., 2000, 2005, 2018, 2022). And during weak growth, policy turns accommodative and lowers bond income at a time where reliable cash flow may be critical.

- Rising deficits and the increase in Treasury issuance to fund spending: In addition to exacerbating trend number three, this impacts market cap-weighted broad bond benchmarks where US Treasury debt now accounts for 50% of the exposure today compared to 25% 20 years ago.7

Together, these forces challenge the reliable income-generating role of conventional stock–bond portfolios, at a time when the demand for income is only increasing.

But investors are no longer confined to a simple set of assets. What was once a narrow universe dominated by government and corporate bonds now spans dividend-paying equities, real assets, private credit, derivative-income strategies and purpose-built retirement solutions.

With a wider range of options, income investing today requires balancing trade-offs to depart from the traditional within a portfolio construction context—layering strategies next to each other to generate income as an outcome and within a risk framework that focuses on how different sources of cash flow behave across market cycles.

Income differs by level, source, stability, and sensitivity

In practice, modern income strategies are designed with structural and operational customizations as the key to unlocking enhanced income generation potential. They combine traditional income sources with capital appreciation, structure, and time based design—reflecting a shift toward outcome-oriented income design that reframes income around three questions:

- How is cash flow generated?

- How stable is it across cycles?

- How does it align with real world spending needs?

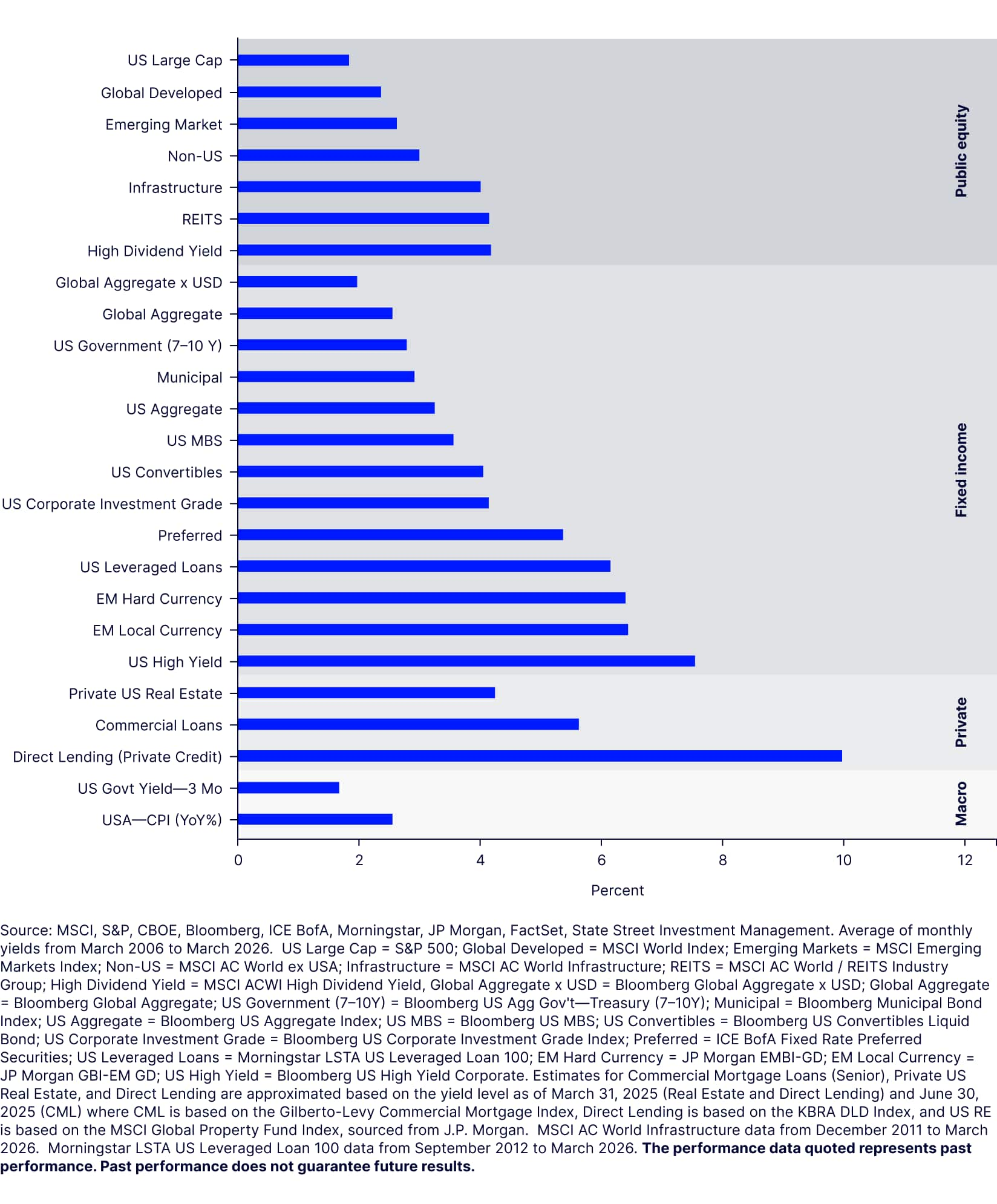

Once income is viewed as an outcome, rather than a property native to the asset class (i.e., just a stated coupon), the differences between income sources become critical. And that outcome can be created by aligning high income strategies next to each other that generate cash flows through different economic transmission channels beyond a spread over the risk-free rate. This is illustrated by the wide dispersion of average yields delivered by a broad range of asset classes.

Over the past 20 years, private market–oriented strategies such as direct lending have generated the highest average yields, followed by high yield bonds and commercial mortgage loans. Government bonds, investment grade credit, and broad equities have produced substantially lower levels of income (Figure 2).

Figure 2: Comparing asset classes’ average yields shows a wide dispersion

This dispersion in income outcomes highlights a broader reality: no single broad asset class can reliably deliver the income, stability, and flexibility investors increasingly require. As a result, modern income portfolios are drawing on a wider—and more diverse—set of income levers than in the past.

Beyond bonds: An expanded income toolkit reshapes portfolio construction

Today, investors can choose from a broader set of income levers. Income streams that were once difficult to access—due to capital requirements, operational complexity, or market structure—have become widely available through public markets and investment vehicles.

Property income is a clear example. Direct ownership of rental real estate historically required substantial capital and active management. Today, investors can benefit from rental income via REITS (real estate investment trusts) which are available as ETFs and Real Estate sector funds.

Big picture, income investing today extends well beyond its traditional fixed income roots. Investors now have a wide range of asset classes and strategies that can contribute to portfolio income, including:

- Global government bonds

- Global investment grade and high yield corporate bonds

- Municipal bonds

- Emerging market debt (hard and local currency)

- Senior loans

- Securitized assets like MBS, ABS, CMBS, and CLOs

- Global dividend paying equities

- Preferred securities

- Convertible securities

- Derivative income strategies

- Private credit

- Real estate (private and public)

- Infrastructure (private and public)

Importantly, these sources of income differ meaningfully in terms of yield levels, risk profiles, liquidity, and sensitivity to economic conditions. The challenge—and opportunity—for investors lies in combining these levers to meet income needs while managing volatility and preserving long term return potential.

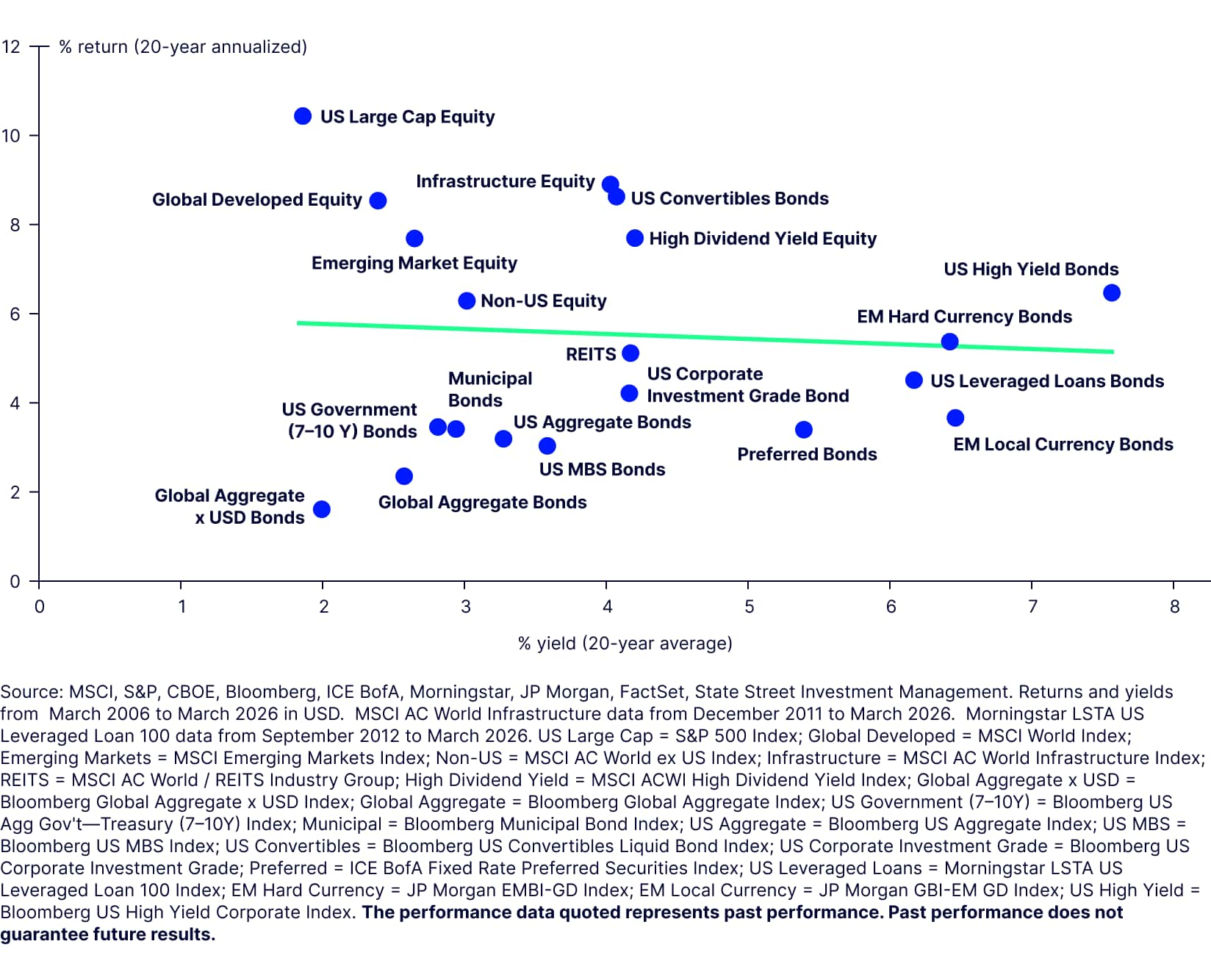

Higher yield doesn’t always mean higher return

While higher-yielding assets may appear attractive from an income perspective, yield alone does not determine overall performance. Over the same 20-year period as above, equities generated the highest total returns, despite offering lower levels of income. High dividend equity strategies, in particular, stand out: they delivered yields comparable to—or higher than—investment-grade corporate bonds, while producing meaningfully stronger total returns.

By contrast, other higher yielding equity segments, such as infrastructure and REITs, underperformed broad market-capitalization-weighted equities on a total return basis. Only high yield bonds and preferred securities delivered higher yields than high dividend equities, highlighting the importance of evaluating income and return together (Figure 3).

Figure 3: Comparing income yield versus return

Fixed income: Engineering cash flow with precision

Fixed income has historically served as a cornerstone of income-oriented portfolios. But its role has become more complex as yields have fluctuated significantly over time.

In recent years alone, yields on broad US fixed income ranged from a low near 1% in mid-2020 to over 5% in late 2023, underscoring the sensitivity of bond income to the interest-rate environment. And that wide range of income came with similarly elevated total volatility, as the macro complexities of the 2020s have transformed what constitutes a “defensive” risk profile. This is illustrated by the long-term US Treasurys trailing 1-year volatility, which averaged 16% in the 2020s versus 12% in the 2010s.8

Despite the current complexities, income generation is native property for bonds. As a result, in an income-engineered-for-outcomes framework, fixed income often serves as the primary “engineering” toolkit. This requires not just owning broad bonds in a set-it-and-forget-it approach. But investors can use multiple levers to help intentionally set cash-flow timing (maturities/structures), interest-rate sensitivity (duration and curve positioning), spread and default exposure (sector and credit quality), and liquidity (public versus less liquid credit).

The objective is not to maximize yield, but to design a cash-flow profile that fits real-world needs—such as funding a distribution policy, matching known liabilities, or supporting model portfolios.

Total bond returns reflect both coupon income and changes in bond prices, which are influenced by interest rates, economic conditions, and credit quality. As a result, yields and total returns do not move in lockstep over shorter horizons. But over longer periods, higher starting yields have historically translated into higher realized returns. A fact reinforced by the correlation between the starting yield on core bonds and their subsequent returns growing closer to one as the time period extends (Figure 4).

Big picture, bond income potential is at its highest when the price paid is nearing lows, but only for the patient long-term investor and provided that the low price is not signaling defaults.

The time varying income effect is also evident in research that found longer-duration bonds have tended to offer more stable income streams but greater short-term price fluctuations, making them more suitable for that same patient investor prioritizing predictable cash flow over portfolio value stability.

Equities: Income as a complement to growth—not a substitute

Equities have traditionally been used primarily for capital appreciation, but income-oriented equity strategies now play a more deliberate role within modern income portfolios. Rather than serving as a primary source of portfolio cash flow, equities are increasingly used to complement income objectives by balancing yield, volatility, and long-term growth potential.

Dividend income varies meaningfully by strategy, region, and sector. Dividend-focused approaches, such as high dividend or dividend growth strategies, provide systematic ways to increase income within an equity allocation.

Equity-like assets such as REITs, infrastructure equities, and preferred securities have historically offered higher yields than broad equity markets, supported by underlying cash flows tied to real assets or contractual revenues (Figure 5).

Within equities, the income–growth tradeoff is especially pronounced. Strategies designed to deliver higher levels of income often tilt away from growth-oriented segments of the market, which can limit long-term return potential relative to broad capitalization-weighted benchmarks. For example, the MSCI ACWI High Yield Dividend Index has underperformed the MSCI ACWI Index by 1.8% per annum over the past 20 years.9

Yet some higher-yielding equity segments have also exhibited lower volatility than the broader equity market—offering partial downside mitigation during periods of stress—these characteristics reflect portfolio tilts rather than free income risk reduction. For example, the MSCI ACWI High Yield Dividend Index has had a lower standard deviation of returns than the MSCI ACWI Index over the past 20 years (15.1% versus 15.8%).10 But more stable dividend growth-oriented dividend benchmarks may offer even lower volatility. For example, a dividend grower’s version of the S&P 500 Index had 120 percentage points lower volatility than the S&P 500 Index.11

Geography and sector composition further shape equity income outcomes. US equities tend to offer lower dividend yields than non-US markets, largely due to the US market’s concentration in growth-oriented sectors such as Technology, where firms prioritize reinvestment and share buybacks over cash distributions. By contrast, sectors such as Utilities, Consumer Staples, Health Care, and Energy have historically offered higher yields supported by more stable cash flow.

Taken together, equities contribute to income portfolios not by maximizing yield, but by supplementing cash flow while preserving exposure to long-term growth. Their effectiveness depends on how they are combined with other income sources, and on a clear understanding of the growth tradeoffs embedded in income-oriented equity strategies.

Tradeoffs of pursuing greater cash flow with alternatives and hybrids

As income needs increase, portfolios often move beyond traditional income sources, bringing tradeoffs that can become more consequential. That is, higher income is rarely achieved without accepting some combination of greater risk, reduced upside participation, increased complexity, or deviation from traditional benchmarks by transforming a risk factor to derive a different income stream from that traditional market. For example:

- Real estate: Private real estate investments (dedicated or part of private equity funds) tend to perform well in inflationary environments, as lease structures often include inflation-linked escalators, which diversify equity/bond allocations. However, investors must consider liquidity constraints, especially in private real estate, and the impact of interest rate fluctuations on property valuations and financing costs.

- Infrastructure: Transportation networks, utilities, and renewable energy projects are increasingly recognized for their defensive qualities and predictable cash flows. Underpinned by long-term contracts or regulated revenue models, they can provide stability even during economic downturns. Moreover, infrastructure often benefits from secular trends like urbanization and the energy transition. Key considerations include political and regulatory risks, as well as long investment horizons.

- Preferred securities: Preferreds occupy a unique space between equities and bonds, offering higher yields than traditional investment-grade debt while maintaining priority over common equity in the capital structure. Particularly attractive in a low-growth, low-rate environment, many are issued by financial institutions with strong balance sheets. But preferreds can be sensitive to interest rate movements and credit spreads, and their hybrid nature means they may be callable or have limited upside in rising rate environments.

- Convertible bonds: With income provided through regular coupon payments, the option to convert into equity creates potential upside if the issuer’s stock performs well. Their yield is typically lower than that of a comparable non-convertible bond but often higher than the dividend yield on the issuer’s common stock, positioning convertibles between bonds and equities. Higher equity sensitivity can limit downside protection relative to straight bonds. And in rising interest-rate environments, convertibles may face price pressure from their bond component.

New tools for income design

As income investing has evolved from a yield-focused exercise to an outcome-oriented discipline, a new set of tools has moved into the mainstream. These approaches are not replacements for traditional income sources, but complements, designed to address specific portfolio needs such as income enhancement, interest-rate sensitivity, and diversification.

While they can meaningfully increase portfolio cash flow, they also introduce distinct tradeoffs related to upside participation, liquidity, and complexity. Understanding how these tools work—and where they fit—is increasingly important for designing sustainable income outcomes.

- Derivative income: These strategies typically combine underlying equity exposures, like the S&P 500 Index, with derivatives to pursue enhanced income. This segment has grown rapidly, with more than 200 US-listed ETFs included in Morningstar’s US Fund Derivative Income category.

The trade-off for enhanced income potential is lower total return relative to the underlying market, as derivatives may limit upside price appreciation. - Private credit: Like traditional bonds, private credit investments generate income through regular, contractual interest payments from the borrowers. Historically, yields are often higher than in public markets to compensate investors for different levels of liquidity as well as the specialization premium inherent in how the customized deal is packaged. Note that many private credit loans are floating-rate, meaning the interest rate adjusts with a benchmark rate. This can help provide a hedge against rising interest rates.

Because the private credit liquidity profile differs from that of public bonds, with some vehicles offering longer lockups and fewer exit options, and returns depend heavily on borrower fundamentals and deal structures, it’s best viewed as a complement to public income sources rather than the sole source of income, particularly for investors with longer-time horizons and lower immediate liquidity needs.

Figure 6: Income enhancement tools and associated tradeoffs

| Income tool / strategy | How income is enhanced | Primary tradeoff |

| Traditional fixed income (IG bonds) | Coupon payments from interest income | Lower long‑term return potential; income compressed when yields are low |

| High yield bonds | Higher coupons relative to investment‑grade bonds | Greater exposure to credit risk and economic downturns |

| Dividend‑paying equities | Higher cash distributions from companies with established payout policies | Increased exposure to value‑oriented sectors and reduced exposure to high‑growth stocks |

| High dividend / dividend growth strategies | Systematic tilt toward higher‑yielding or consistently paying companies | Distinct value bias and the potential for underperformance in strong growth‑led equity markets |

| REITs (public real estate) | Rental and property income distributed through equity structures | Sensitivity to interest rates and property market cycles |

| Infrastructure equities | Regulated or contracted cash flows from capital‑intensive assets | Concentration in specific sectors and exposure to regulatory risk |

| Preferred securities | Higher income through hybrid equity/debt instruments | Interest‑rate sensitivity and limited upside participation |

| Convertible bonds | Interest income plus potential equity conversion | Lower yield than non‑convertible bonds and fixed corporate bonds; equity exposure introduces volatility |

| Derivative income | Derivative securities used to generate potential premium income | Capped upside participation; higher income can reduce total returns while still exposing investor to equity risk (albeit less than broad equities) |

| Private credit | Contractual interest payments, often at higher yields than public bonds | Limited liquidity; greater reliance on borrower credit quality and longer investment horizons |

Source: State Street Investment Management, as of May 2026.

While asset classes and strategies shape how income is generated, they do not, on their own, determine whether income needs are actually met. For many investors, the next step is moving beyond income generation toward structuring portfolios that convert total return into dependable, repeatable cash flow.

From generating income to delivering income outcomes

Beyond individual asset classes, a growing set of tailored income solutions focuses not on generating yield from a portfolio’s holdings, but on converting total return into predictable cash flows.

In these approaches, income is delivered through the planned drawdown of principal and capital appreciation over time, often on a predefined schedule. The distinction is important: rather than asking which assets produce the highest income, these solutions begin with the question of how much income is needed, when, and for how long.

- Annuities represent one of the earliest and most established examples of this outcome-oriented approach. Structured as contracts rather than investments, annuities provide a guaranteed stream of income in exchange for an upfront premium or a series of contributions.

The underlying mechanism involves pooling assets and longevity risk, with insurance providers investing those assets—typically across bonds, and in some cases equities or other return-seeking instruments—to transform market returns and capital gains into steady, reliable payments. In effect, annuities separate income delivery from market volatility, trading liquidity and flexibility for certainty.

- Bond ladder strategies offer a different method of structuring income, without explicit guarantees. A bond ladder is constructed by holding bonds with staggered maturity dates, so that principal is returned at regular intervals. Maturing bonds can be used to fund spending needs or reinvested, helping to manage interest-rate risk while creating a more predictable pattern of cash flows.

Unlike yield-maximizing bond allocations, laddered approaches emphasize timing and cash-flow alignment, making them particularly useful for investors seeking to match portfolio income to known future liabilities.

Taken together, these retirement-focused solutions highlight a broader shift in income investing—from identifying higher-yielding assets to engineering portfolios around desired cash-flow outcomes. Rather than relying solely on yield, they draw on total return, diversification, and time-based structuring to meet retirement spending needs more precisely.

The future of income investing: Designed, diversified, and deliberate

Income investing has entered a new era.

Structural changes in markets, evolving stock–bond relationships, and a broader opportunity set have fundamentally altered how portfolios generate and sustain cash flow. In today’s complex and uncertain environment, income is no longer something portfolios simply produce—it is something investors must intentionally design for.

Income can no longer be anchored to a single asset class or evaluated through yield alone. Reliable income outcomes depend on how income is generated, where it comes from, and how it behaves over time. Different asset classes deliver cash flow in different ways, balancing income against volatility, liquidity, and long-term return potential. As a result, traditional, one-dimensional income frameworks are often insufficient to meet modern portfolio needs.

Today, effective income strategies require deliberate portfolio design—combining contractual income, total return, and structural tools in ways that reflect individual objectives, risk tolerance, liquidity constraints, and time horizons. In practice, this often means blending multiple income sources rather than relying on any one lever in isolation.

This outcome-oriented approach is less about maximizing yield and more about making informed choices: which risks to take, where to take them, and how to combine them in pursuit of sustainable cash flow. Fixed income remains the critical toolkit in this process, helping investors shape, sequence, and manage income outcomes over time.

Ultimately, the future of income investing won’t be defined by any single solution, asset class, or metric. It will be defined by portfolios that are designed, diversified, and deliberate—and aligned with the role income plays in the broader portfolio.