The economics of AI-driven productivity

As AI lifts productivity, its effects on jobs and profits are less linear than headlines suggest. This edition explores how efficiency gains can cushion margins, influence labor dynamics, and shape market outcomes across sectors.

US productivity growth over the past 30 years has been far from uniform. The late 1990s and early 2000s stand out as a period of above-average gains, coinciding with the widespread adoption of the internet and information technologies. By contrast, productivity growth during much of the mid-2010s was surprisingly subdued despite rapid digitalization. While recent data show a welcome reacceleration, gains are only roughly in line with long-run averages—suggesting the current AI cycle may still be in its early innings.

Weekly highlights

Source: S&P, FactSet. Data as of April 13, 2026.

Source: S&P, FactSet. Data as of April 13, 2026.

Source: S&P, FactSet. Data as of April 13, 2026.

Productivity, unemployment, and profits: The AI transmission mechanism

Moving beyond the daily geopolitical headlines, investors are grappling with a broader set of questions around what comes next for growth, inflation, and markets. Near the top of that list sits artificial intelligence—not as a single, settled narrative, but as an open-ended force with the potential to reshape productivity, labor markets, and corporate profitability.

The debate often begins with a simple question: If AI raises productivity by changing how work gets done, what happens to employment, demand, and the durability of the profit cycle? The honest answer is that the range of outcomes remains wide. The macro and the micro intersect here in important ways, and history offers a useful lens for how firms tend to behave as labor markets soften.

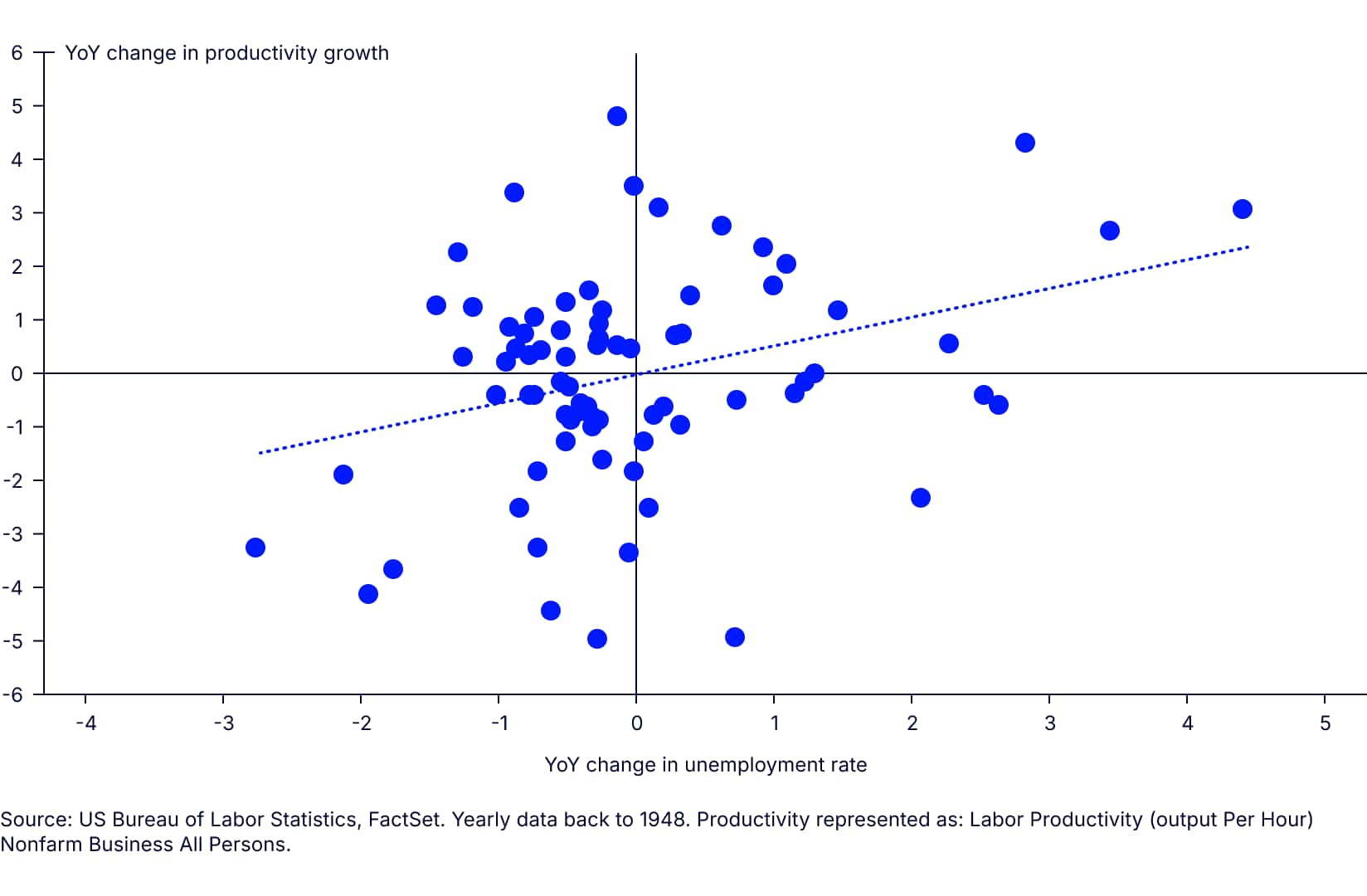

Productivity and unemployment: Why the relationship can be two-way

Productivity increases with unemployment

One of the more underappreciated dynamics in the data is that productivity growth often strengthens as the unemployment rate rises (chart above). The intuition is straightforward: When labor markets soften or demand uncertainty rises—companies face a sharper imperative to “do more with less.” Hiring slows, low-return projects get cut, and attention shifts toward efficiency and throughput. In that sense, higher unemployment can cause a productivity impulse as firms streamline.

The causality can also run the other direction. When productivity accelerates meaningfully—through technology, process change, or capital deepening—firms may be able to produce the same output with fewer workers. That can mechanically push unemployment higher, at least during transition periods. In other words, unemployment can rise because productivity improves. Practically, the economy often experiences some mix of both forces at different points in the cycle.

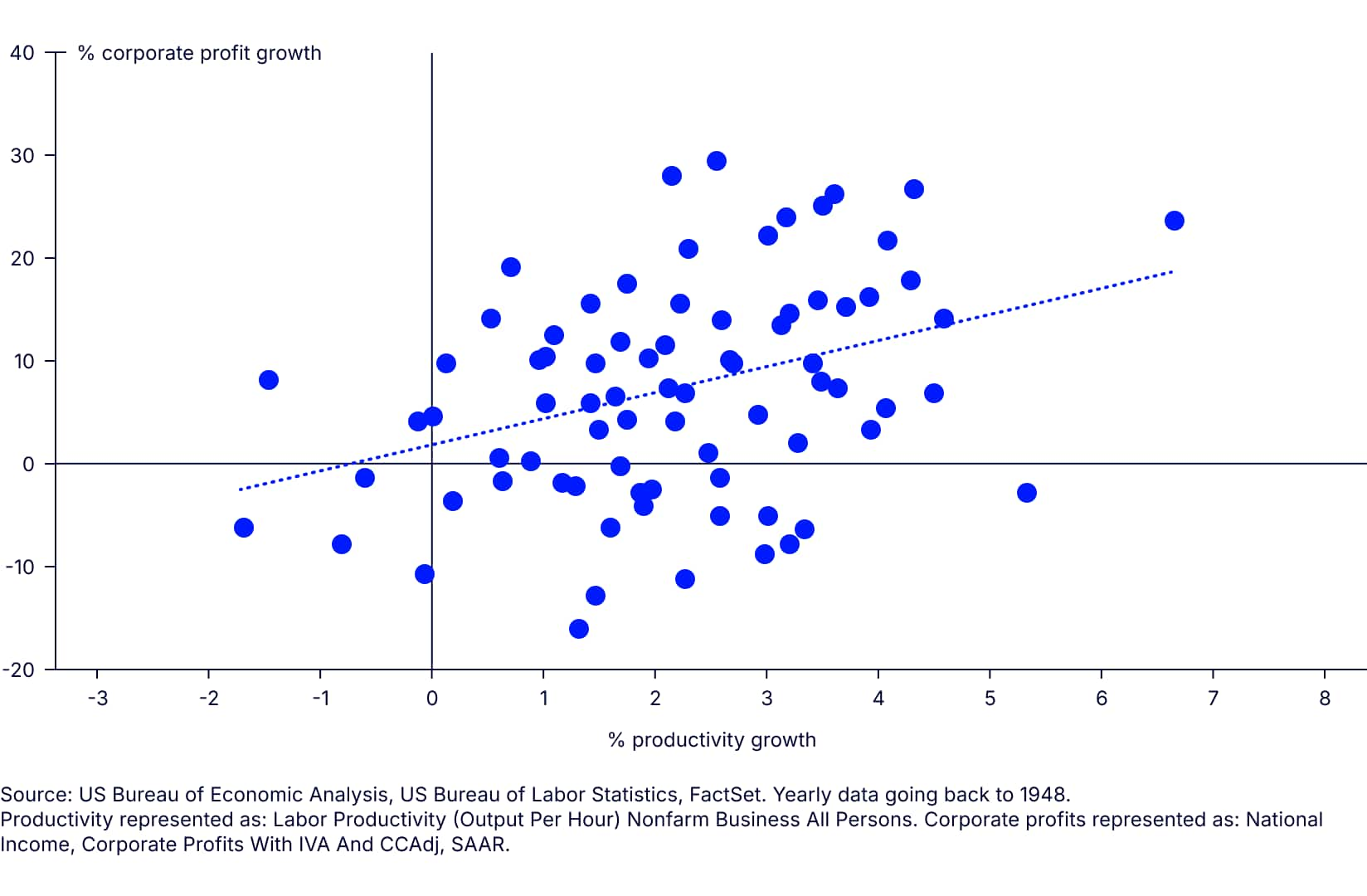

From productivity to profits: The corporate cushion

Productivity leads to profits

This chart illustrates an expected relationship: Stronger productivity growth tends to coincide with higher profits. Putting the two charts together frames the heart of the issue. Even in periods when the labor market deteriorates, productivity can improve—and that improvement can provide a partial cushion to corporate profits. This is not because unemployment is “good,” but because corporate management teams react to changing conditions. They protect margins by reducing discretionary costs, reconfiguring operations, and leaning into efficiency. When successful, earnings can hold up better than macro anxiety would suggest, at least for a time. This is one reason the market’s relationship with unemployment is not linear.

Crucially, however, higher margins rarely persist in isolation. Even if AI improves profitability in a vacuum, corporate behavior rarely stops at “we’ve protected margins; let’s be content.” Competitive forces tend to recycle productivity gains into reinvestment—more aggressive pricing, capacity expansion, faster product cycles, deeper distribution, or entry into adjacent markets that were previously uneconomic. Productivity, in other words, often seeds the next phase of competition rather than locking in a static margin outcome.

This dynamic also limits the notion of a stable end state in which firms cut costs, shrink headcount, and simply accept a permanently lower growth world. The impulse to outgrow competitors remains incredibly powerful. And growth, importantly, still tends to require humans. Even in an AI-enabled environment, higher productivity can raise the returns to hiring in certain functions, as each employee can now drive larger outcomes per unit of effort. Put differently, firms may not need as many people to do yesterday’s work, but they may hire to pursue tomorrow’s opportunities.

AI as a catalyst—And the labor market anxiety it creates

AI is best understood as a potentially significant new contributor to productivity, particularly in knowledge-intensive work such as drafting, coding assistance, customer service triage, data extraction, and compliance review. While AI will displace certain tasks and some job categories as currently defined, widespread adoption still requires human judgment, accountability, client trust, and strategic oversight. For many firms, AI is not a full substitute for labor; it is a force multiplier that changes the composition of labor demand.

This is where the public narrative can get distorted. It is often easier to identify the jobs that may “roll off” than to envision the jobs that will “roll back on.” Historically, technology waves tend to retire tasks faster than they reveal new job titles. New employment often appears embedded within existing roles, new services, or newly scalable forms of demand. The key swing factor is pace. Gradual adoption allows labor markets to adapt through normal churn; abrupt, concentrated adoption raises the risk that displacement temporarily outpaces absorption.

Investment takeaway

AI-driven productivity gains can coexist with rising unemployment—particularly during transition periods—and corporate profits may prove more resilient than headlines imply if efficiency gains partially offset demand weakness. The risk is labor market deterioration that’s severe enough to overwhelm the margin cushion.

For investors, the conclusion is nuanced. Rising unemployment alongside rising productivity does not automatically imply poor returns, nor does it guarantee strong ones. Outcomes will vary by sector, business model, and time horizon. Markets are likely to reward firms that translate AI adoption into measurable productivity—higher revenue per employee, faster cycles, or lower unit costs—rather than those that merely articulate AI ambition. In practice, that favors companies with proprietary data, repeatable workflows, and distribution advantages. Regionally, the early leadership signal may come from the US (scale platforms, deep capital markets) alongside pockets of AI-heavy supply chains in parts of Asia; over time, diffusion matters more than invention, and markets with faster corporate adoption and fewer legacy frictions should see the bigger margin and growth effects.

Go beyond the headlines...

Skimmed the summary? Dive deeper with the full PDF—your go-to for weekly market insights and analysis.