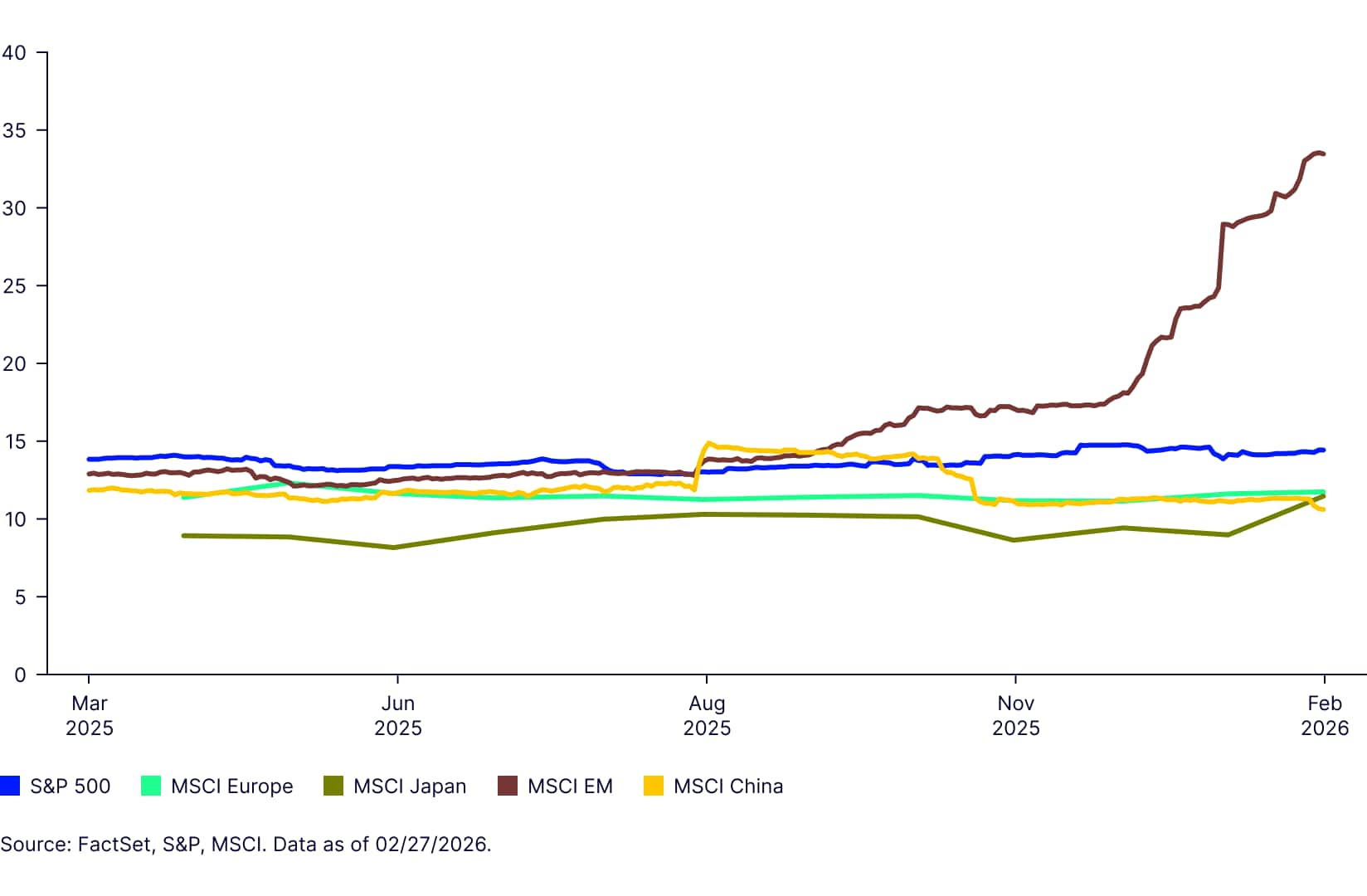

China’s market disconnect

China’s equity markets have fallen out of sync with broader emerging markets, reflecting policy uncertainty, property sector stress, and uneven earnings momentum despite long‑term growth potential.

China is the largest constituent within MSCI Emerging Markets, representing approximately 24% of the index. However, return correlations indicate that China’s performance has become meaningfully less aligned with that of other emerging market peers. We’ve long suggested that investors consider separating China from a broader EM allocation, as its unique economic drivers, policy framework and structural characteristics have led to differentiated outcomes.

Weekly highlights

Source: FactSet. Data as of 3/4/2026.

Source: FactSet. Data as of 3/4/2026

Source: FactSet. Data as of 3/4/2026. China’s YTD performance in LC terms.

Emerging markets: Earnings-led performance with a technology backbone

Emerging Markets (EM) outperformed developed markets in 2025, delivering a 32% return in local‑currency terms, and performance has been supported by earnings. Reported fourth‑quarter 2025 earnings growth currently stands at 19% YoY, with approximately 42% of companies having reported, and forward‑looking expectations continue to strengthen. Analysts are increasingly forecasting additional earnings upside into 2026, creating a constructive backdrop for continued total returns.

Earnings upgrades have been led primarily by Korea, Taiwan, and South Africa, with information technology emerging as the dominant contributor. Estimated CY 2026 earnings growth for MSCI EM Information Technology has surged from just 10% in September to more than 92% today, underscoring the scale of the earnings revision cycle now underway.

1-year EPS growth estimates

This strength reflects a broader structural shift within emerging markets. EM is no longer primarily a commodity- or financials-driven allocation. Instead, it has become increasingly tied to global technology and artificial intelligence investment cycles. Information technology is the largest sector in MSCI EM, accounting for 32% of the index, broadly in line with the S&P 500’s 32% exposure. Excluding China, the technology footprint is even more pronounced, with IT representing approximately 39% of the MSCI EM ex China Index.

Beyond technology itself, macro conditions have also proven supportive of EM. Despite tariffs and geopolitical uncertainty, growth across emerging markets has remained intact. At the same time, a softening US dollar and expectations for Federal Reserve easing have supported both EM equity and credit markets.

Valuations remain compelling. The MSCI Emerging Markets Index continues to trade at a discount to developed market peers, with a forward P/E of approximately 13x versus 21x for the S&P 500.

China versus the rest of EM: Why the recent gap in performance?

MSCI EM ex China has delivered a local‑currency return of roughly 10% year to date. In contrast, China has struggled, posting a total return of -5% year to date as of March 4th. While estimates still point to approximately 12% earnings growth for CY 2026, equity performance in China still hinges on domestic policy clarity, property market stabilization and household balance-sheet repair.

As featured in the Chart of the Week, China’s performance has diverged from EM, and this dynamic is also evident over the past year. The divergence over this time period can largely be traced back to market dynamics in late September and October. Chinese equities rallied sharply into late September following Beijing’s announcement of its largest stimulus package since the pandemic. These measures initially fueled a pronounced surge in MSCI China. By early October, however, much of the rally had already front‑loaded months of expected returns. As October progressed, economic data disappointed, policy expectations peaked and geopolitical risks reemerged. Chinese equities underperformed as a result, while the rest of EM continued to benefit from a more supportive macro and earnings environment.

The performance contribution breakdown indicates that the primary detractors from MSCI China’s performance since October have been communication services, consumer discretionary, and information technology. In China, we view the IT sector and AI investment as important pillars for sustaining equity market performance. However, questions persist around the durability of growth and the monetization of innovation. While China benefits from structural advantages in energy, it continues to lag in the development and manufacturing of leading‑edge semiconductors. Moreover, many of the fastest‑growing AI innovators remain either unlisted or underrepresented in major equity indices, limiting their impact on broader market performance.

Geopolitical shock: Iran and near‑term EM risks

More recently, the war with Iran has introduced a new source of volatility. Since the initial escalation, MSCI Emerging Markets has declined by approximately 7% in local-currency terms as of March 4. Korea, Egypt and Thailand have been among the most adversely affected, reflecting their sensitivity to higher crude prices and disruptions to trade flows through the Strait of Hormuz. That said, market conditions are evolving rapidly, and performance dynamics may have shifted by the time of reading.

A prolonged conflict with Iran could be negative for emerging markets in the near term, primarily through higher energy prices, weaker currencies and tighter financial conditions. However, as laid out in our Global Market Outlook back in January, our longer-term view on emerging markets is positive. EM continues to offer a compelling earnings‑driven opportunity set, led by technology‑oriented economies, and should benefit from a weaker dollar once more clarity on the duration and extent of the war materializes, as well as increased capital flows into the asset class.

Go beyond the headlines...

Skimmed the summary? Dive deeper with the full PDF—your go-to for weekly market insights and analysis.