Prioritize income and resilience with active short duration and multi-sector credit

In a more uncertain macro environment where inflation and growth risks are stoking rate volatility and credit spreads remain tight, fixed income returns are likely to rely more on income and carry. With less support from price appreciation, generating return depends increasingly on selectivity and active positioning.

Fixed income markets have entered a more complex phase, as tighter spreads and shifting policy expectations limit the scope for price-driven gains. Yet, elevated yields help provide a stronger starting point for income. With income and carry now set to play a more central role in bond portfolio returns, increased volatility and divergence across rates and credit markets reinforce the need for flexibility and selectivity.

In this environment, investors may benefit from focusing on:

- Short-duration active to capture elevated front-end yields across a broader opportunity set, while reducing sensitivity to interest rate volatility

- High-quality core-plus active strategies to provide more resilient income and differentiated return drivers by blending investment-grade asset-backed and mortgage-related sectors

- Active credit allocations with floating-rate exposure to enhance income while maintaining flexibility across evolving market conditions by allocating to a range of below investment-grade high yield and bank loans, as well as collateralized loan obligations (CLOs)

Curve dynamics and elevated yields reinforce the case for short duration

Following a steepening period through much of 2025, yield curves have recently bear flattened,1 reflecting the repricing of policy rates impacting the short end of the curve as near-term inflation expectations constrain policy flexibility.

While global yields have repriced higher, not all policy paths across major central banks are starting from the same place. The Federal Reserve (Fed) continues to navigate persistent inflation with moderating, but still resilient, growth (2026 GDP growth is expected to be 2.2%).2 Meanwhile, the European Central Bank is balancing noticeably slower growth (+0.9%) with still-elevated inflation.3 The Bank of England faces weaker growth (+0.8%) and higher inflation dynamics than the eurozone.4 Lastly, the Bank of Japan is gradually normalizing policy from historically accommodative settings, with growth expected to exceed 1% for the first time since 2022.5

Despite not all starting from the same place, the current repricing indicates a shift from a neutral stance to one that may be more restrictive, as inflation pressures now supersede growth concerns. Even with that seemingly coordinated reaction to rising consumer prices, US bonds continue to offer a meaningful income advantage. Front-end yields are approximately 120 basis points (bps) higher than in the eurozone and nearly 250 bps higher than in Japan.6

While Japanese bonds can appear more attractive once hedged into dollars, that excess yield is primarily a function of FX carry—not underlying bond income—and can erode quickly as rate differentials or currency dynamics shift. In that context, US Treasurys may offer a more durable and predictable source of income.7 Across the US curve, yields also remain elevated relative to both recent and longer-term averages (Figure 1), providing a stronger starting point for income generation.

Although the curve has normalized from deeply inverted levels, it remains below historical steepness, suggesting room for further mean reversion-based steepening that may weigh on the long end. Current macro factors also could have an impact. Changes in Fed leadership, inflation upside bias, a potential stronger focus on balance sheet reduction that could constrain liquidity, and a deteriorating fiscal backdrop with rising deficits have, and may continue to, place upward pressure on term premia as well as longer-dated yields and their volatility.

In contrast, the front end of the curve continues to offer elevated yields with lower sensitivity to interest rate volatility. While the US 2-year yield offers 100 bps less in yield than the US 30-year, it has exhibited significantly lower volatility (roughly 800 bps) over the past year.8 With a higher front-end starting point, investors are also able to capture higher carry through roll down, where bonds benefit from price appreciation as they move toward maturity.

Together, these dynamics reinforce the case for active short-duration strategies, allowing investors to generate attractive income without stretching into longer-duration exposures.

Tight spreads and rising volatility highlight the need for selectivity

Credit markets have remained resilient despite rising volatility across rate markets, with spreads continuing to tighten even as the MOVE Index moves higher (Figure 2). Investment-grade and high yield corporate bond spreads are now in the tightest 3% and 4% of observations over the past 20 years,9 respectively, highlighting a growing disconnect between macro uncertainty and credit trends.

Credit markets have been supported by durable corporate growth trends, as earnings have come in strong for broad equities—the sixth consecutive quarter of double-digit growth for S&P 500 firms.10 At the same time, high yield issuers are exhibiting positive, upward-trending trailing 12-month EBITDA growth and solid interest coverage ratios.11

But at current spread levels, the potential for further compression appears limited, leaving downside risks more asymmetric. Historically, when spreads are in the tightest quintile, forward returns have been more constrained, with subsequent one-year returns averaging 0.7% for IG and 2.7% for high yield.12 Notably, underlying price returns over these periods averaged -4.1% and -4.5%, respectively, highlighting the critical role of income in offsetting price declines when spreads are tight.13

This dynamic has important implications for portfolio construction.

In an environment where volatility is rising but spreads remain tight, outcomes may increasingly depend on strategies focusing on high quality income generation, security selection, and active positioning across sectors where risk-adjusted opportunities remain more attractive.

Diversifying income sources and risk exposures to boost resilience

Many portfolios remain concentrated in traditional sources of credit income, particularly fixed rate high yield and investment-grade corporate bonds. These exposures are driven largely by spread dynamics and corporate fundamentals, making income streams more sensitive to changes in growth expectations and broader credit conditions. With spreads near historically tight levels, this concentration can lead to more cyclical and asymmetric outcomes.

A more diversified approach can improve resilience by incorporating income sources with different underlying drivers. In addition to corporate credit, floating-rate instruments such as bank loans and CLOs offer income with lower sensitivity to interest rate movements. And with policy rates now expected to decline only modestly in 2026, the floating rate currently out on offer may have a more stable floor.

Securitized credit assets, including investment-grade asset-backed securities (ABS), mortgage-backed securities (MBS), and commercial mortgage-backed securities (CMBS), provide differentiated sources of income. Many of these securities benefit from amortization and prepayment, which can accelerate principal repayment and shorten effective duration, allowing investors to capture income without extending interest rate risk.

Many of these segments remain underrepresented in traditional benchmarks. For example, securitized assets, particularly ABS and CMBS, typically comprise a modest share of core bond indices, with only 0.4% and 1.4% exposure, respectively, in the Bloomberg US Aggregate Bond Index.14

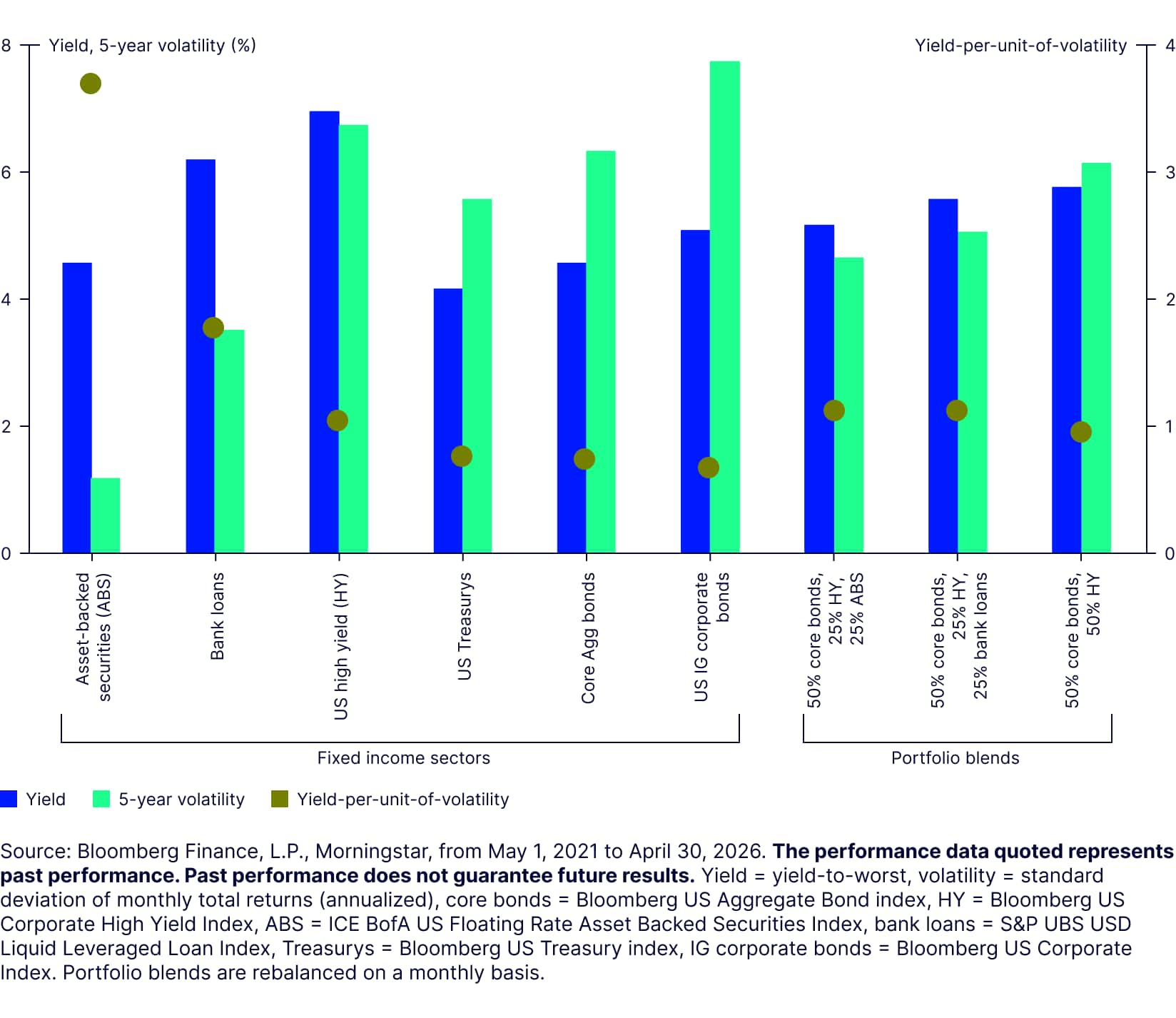

Incorporating floating-rate and securitized credit exposures into a credit-heavy allocation can help maintain attractive yield levels while reducing overall volatility (Figure 3). These examples highlight how combining multiple income sources, rather than relying solely on traditional corporate credit, may improve efficiency and better balance rate and spread risk.

Figure 3: Reducing volatility while preserving returns through income diversification

Positioning for income in an uncertain market

With yield curve dynamics evolving, credit spreads near historically tight levels, and macro uncertainty elevated, fixed income returns are likely to depend more on income, diversification, and active positioning.

A bias toward the shorter end of the curve may help limit volatility while seeking income. And while the curve continues to offer opportunities to capture carry through roll-down, active management can help navigate shifting rate and spread dynamics.

At the same time, a broader active approach to credit—combining corporate credit with less equity- and growth-sensitive exposures along with more diversified income sources across floating-rate and securitized assets—may help support resilience and more consistent outcomes.

In this environment, generating resilient income will depend on where—and how—income is sourced.

Implementation ideas

To reposition your bond portfolio to help target income and resilience, consider:

Active short-duration strategies.

Active core-plus allocation.

Active high income exposure.