The case for emerging markets small-cap equity

For investors considering an emerging markets allocation, we believe it is essential to take a close look at emerging market small caps (EMSC) and the differentiated benefits they offer. In this paper, we outline why EMSC represents a powerful way to access the EM growth story—and why we believe a systematic active approach is the most effective way to capture it.

2025 was another outstanding year for equities broadly, but what may surprise some investors is that—despite concerns around US tariffs—EM equities finished the year among the top performing regions. The EM growth story has returned to the forefront for investors, supported by one of the defining themes of the year: the rapid evolution of AI. And as we recently highlighted, emerging markets are actively participating in—and benefiting from—this trend. Importantly, smaller EM firms are also part of the AI value chain, helping to address the global infrastructure gap. Whether it is electronics manufacturing services, basic hardware suppliers, or capital goods companies, many of these businesses are increasingly plugged into the broader AI support system.

As we move into the next phase of AI adoption—shifting from the development of chips and models toward more practical, real world applications—we expect the associated tailwinds to extend to companies across the market cap spectrum. Rather than focusing solely on large cap technology leaders, we believe the ecosystem effects of AI, together with EM-specific structural drivers and an increasingly supportive policy backdrop, strengthen the case for broadening exposure. And within this opportunity set, one area we believe deserves renewed focus is emerging market small caps. Here’s why.

A purer play on the emerging market growth story

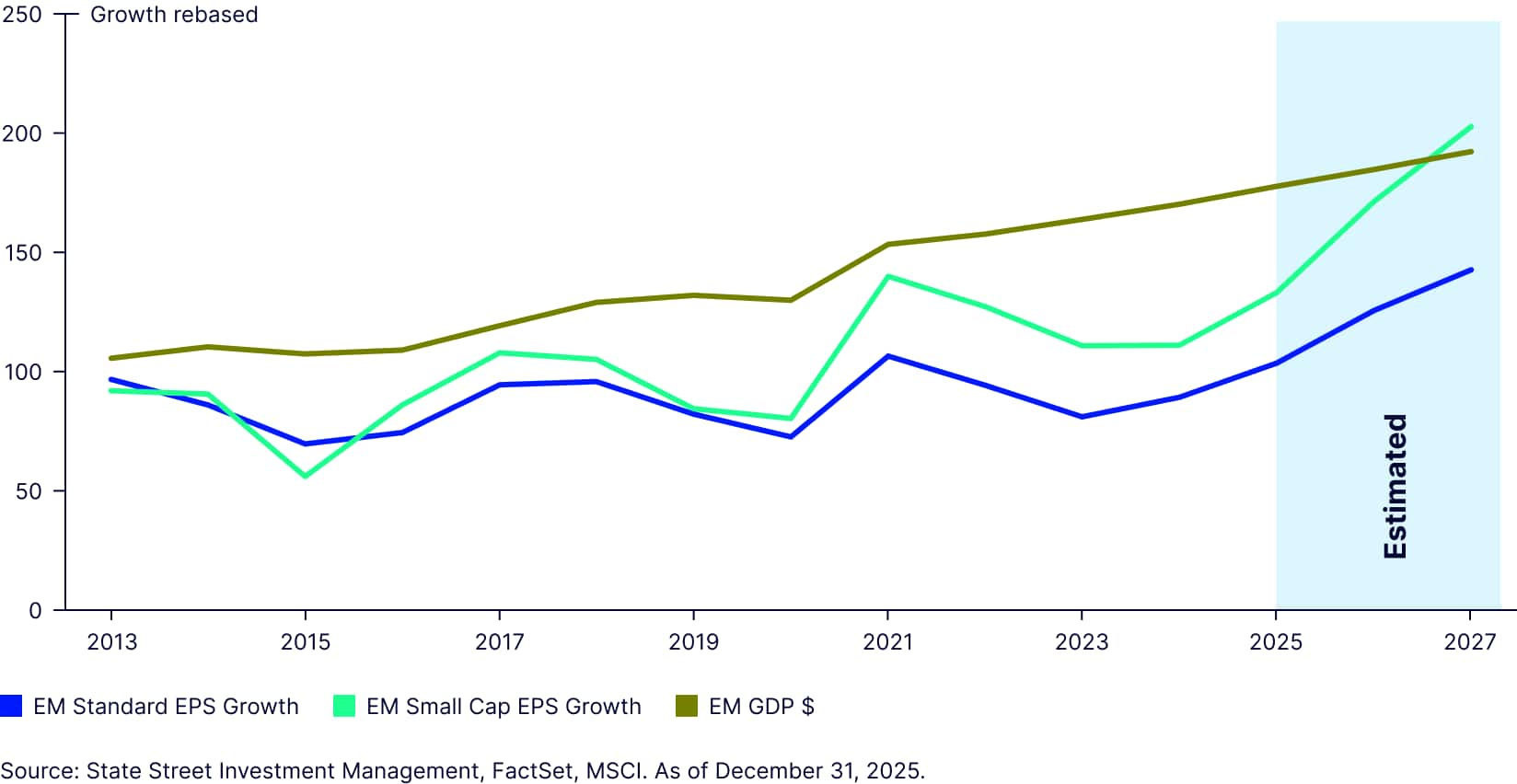

Emerging market small cap stocks provide a unique advantage, offering a purer and more direct exposure to the emerging market growth story. Unlike their large cap peers, which are often influenced by global supply chains, small cap companies are more closely tied to local economic activity. As a result, their EPS growth rates exhibit a stronger relationship with trends in emerging market GDP growth rates than their large cap counterparts (Figure 1). For investors seeking direct participation in the structural growth of emerging economies, gaining exposure to EM small cap equities can be particularly effective. In our view, if capturing the momentum of the EM growth story is a key objective, an allocation to EM small caps should be part of that discussion.

Figure 1: EM small caps offer EPS growth more in line with GDP trend

A distinct opportunity set for portfolio construction

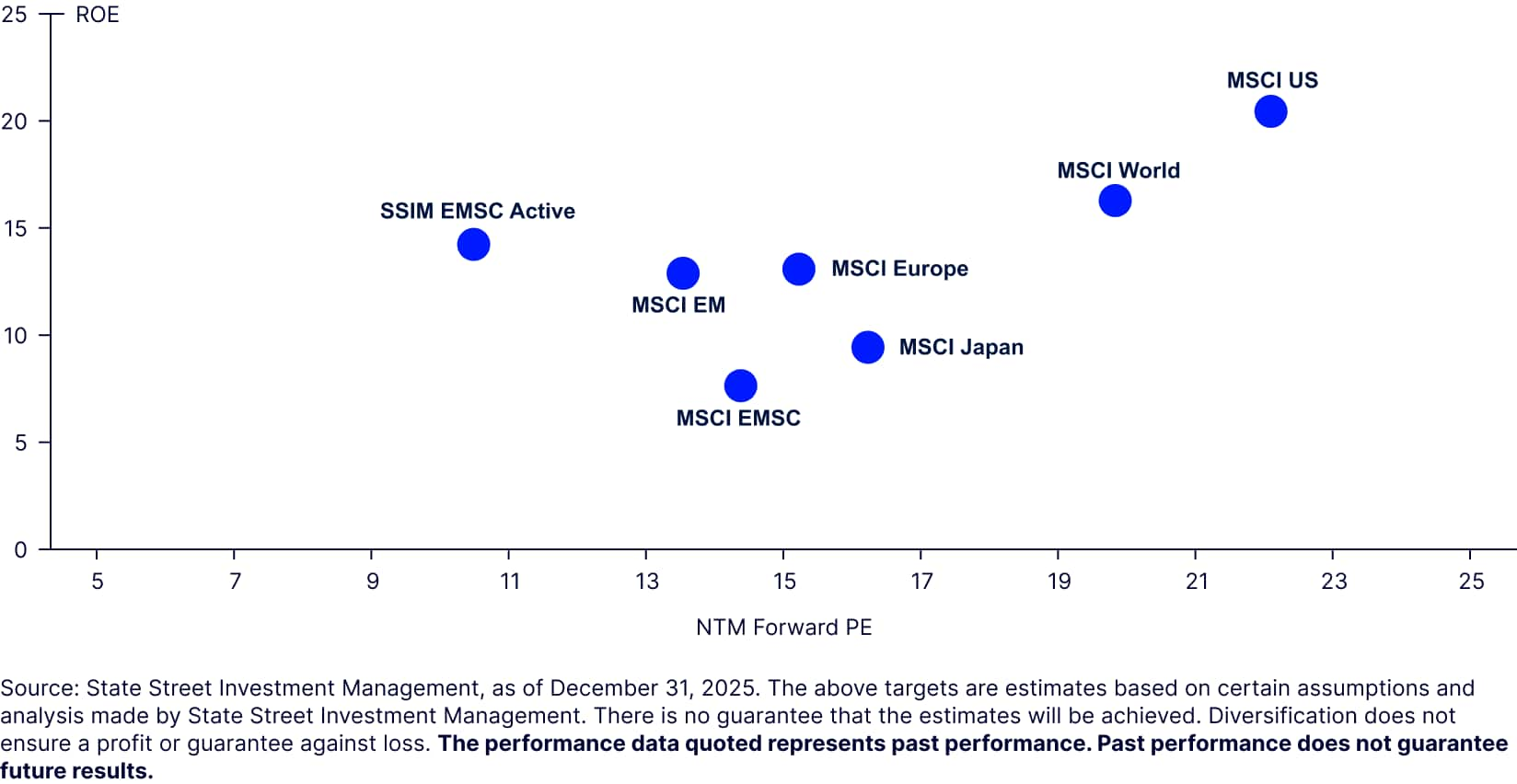

In many global markets, valuations remain elevated, and while high multiples in certain segments may be supported by strong returns on equity (ROE), we view EM small caps as a particularly compelling area for active management. To illustrate, our Systematic Equity Active team can construct portfolios with an ROE of roughly 17% while maintaining a price to earnings (P/E) ratio below 10 (Figure 2)—delivering profitability levels comparable to MSCI World at nearly half the valuation.

Figure 2: Active Strategy valuation to profits

Less dollar dynamics

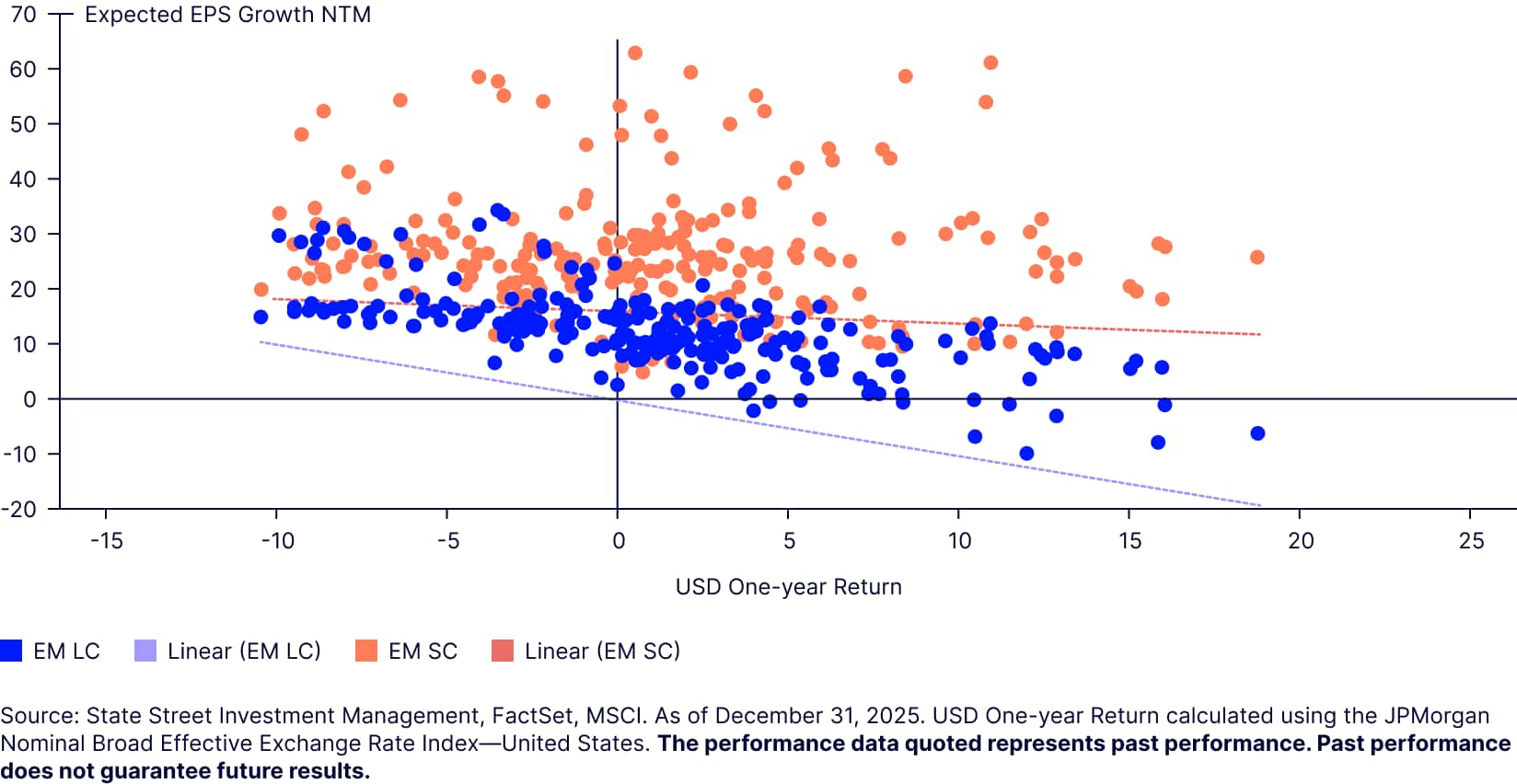

Another appealing characteristic of EM small caps is their significantly lower sensitivity to U.S. dollar movements. This aligns naturally with their role as a purer expression of EM economic growth: revenues for EMSC companies are driven primarily by domestic demand, rather than the global trade flows that shape the more internationally exposed Emerging Markets Large Caps (EMLC).

A simple way to demonstrate this dynamic is by examining the correlation between the twelve month change in the US dollar and forward one year estimated EPS growth. Over the trailing ten year period, the correlation for EMSC is only slightly negative at –0.1, compared with a much stronger negative correlation of –0.7 for EMLC. While opinions differ on the dollar’s path from here, we believe EMSC earnings growth is structurally more insulated from adverse currency moves—providing a more resilient way to participate in EM fundamentals regardless of future dollar trends.

Figure 3: EMSCs have lower correlation with USD dynamics

Risks

Of course, these opportunities come with risks—for example, uncertainty around US policy and tariffs, hesitancy toward adopting Chinese AI tools outside China, and broader geopolitical tensions. However, a systematic investment process that builds diversified portfolios can help mitigate many of these risks. When evaluating an EM allocation, we believe EM small caps represent a highly attractive opportunity set—one where skill, discipline, and a strong focus on risk are essential to extracting value, and where a systematic approach is best suited to deliver it.

Why consider an Active Systematic Approach?

Given the structural inefficiencies in this asset class, we are strong advocates of an active approach—and specifically, a systematic one. Emerging market small caps receive limited attention from the sell side: just over half of the universe has any analyst coverage at all, compared with near complete coverage in the standard MSCI EM Index. This lack of investment by the brokerage community has persisted for nearly fifteen years, since the launch of our Emerging Markets Small Cap Active Strategy. We view this persistent information gap as a clear competitive advantage for systematic managers. Fundamental investors often depend heavily on sell side research, forecasts, and corporate access, which tend to favor larger, more visible companies. As a result, much of the small cap universe remains under analyzed and under owned, creating fertile ground for active managers—particularly those able to process information efficiently across the entire investable universe without the inherent size bias of traditional fundamental approaches.

A systematic approach is uniquely equipped to exploit these conditions. Our state of the art data infrastructure aggregates the latest information across a broad suite of factors and sources on more than 3,000 emerging market securities each day. Our models continuously evaluate the opportunity set, allowing us to identify and react to new information quickly, minimizing inertia or slippage and enabling more efficient capture of alpha. Because sell side attention is disproportionately concentrated in the largest names, many of our most compelling ideas emerge in less covered segments of the market. Our model identifies firms with attractive valuations, strong quality profiles, and improving fundamentals and, critically, it can uncover these opportunities before they appear on the radar of other investors.

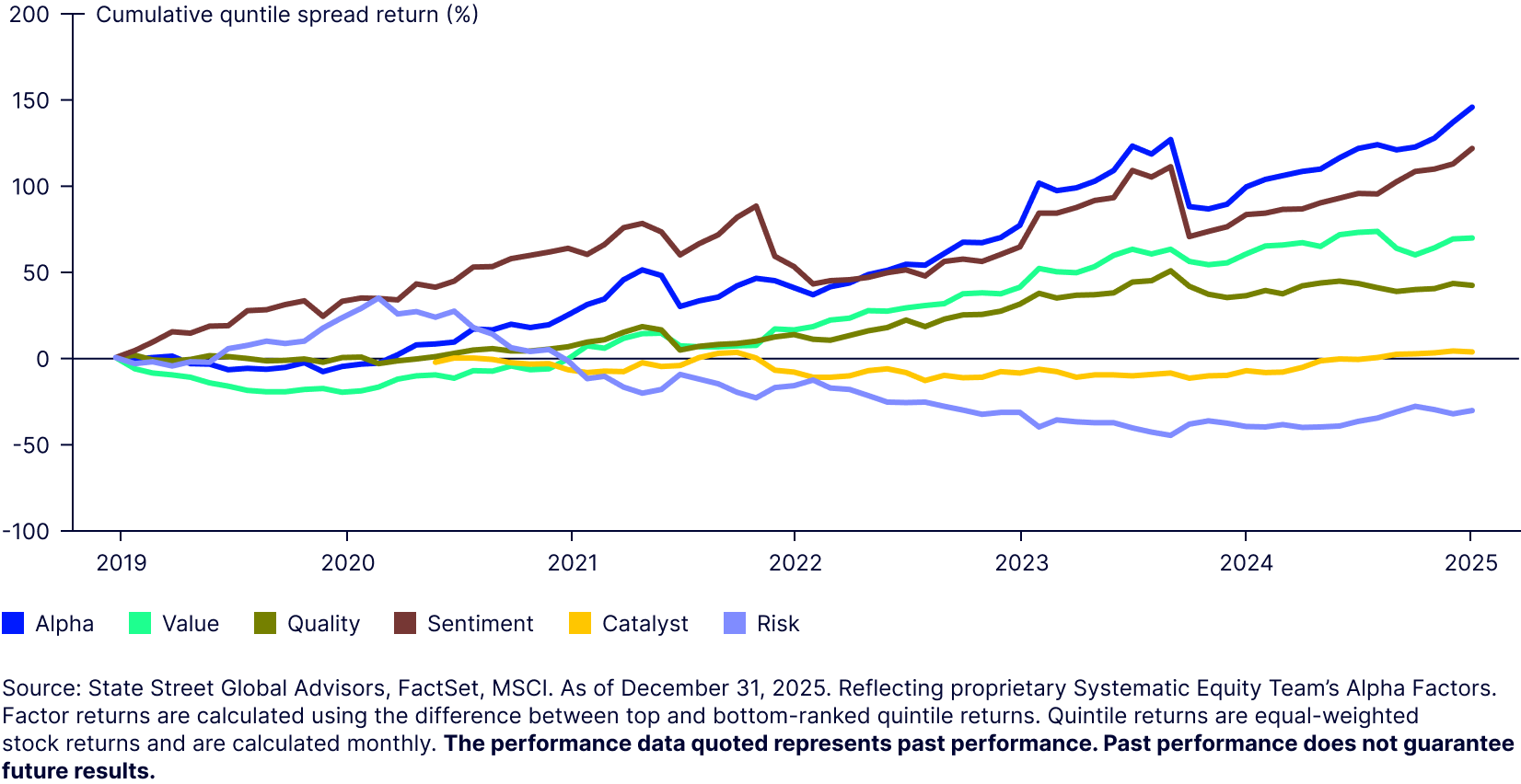

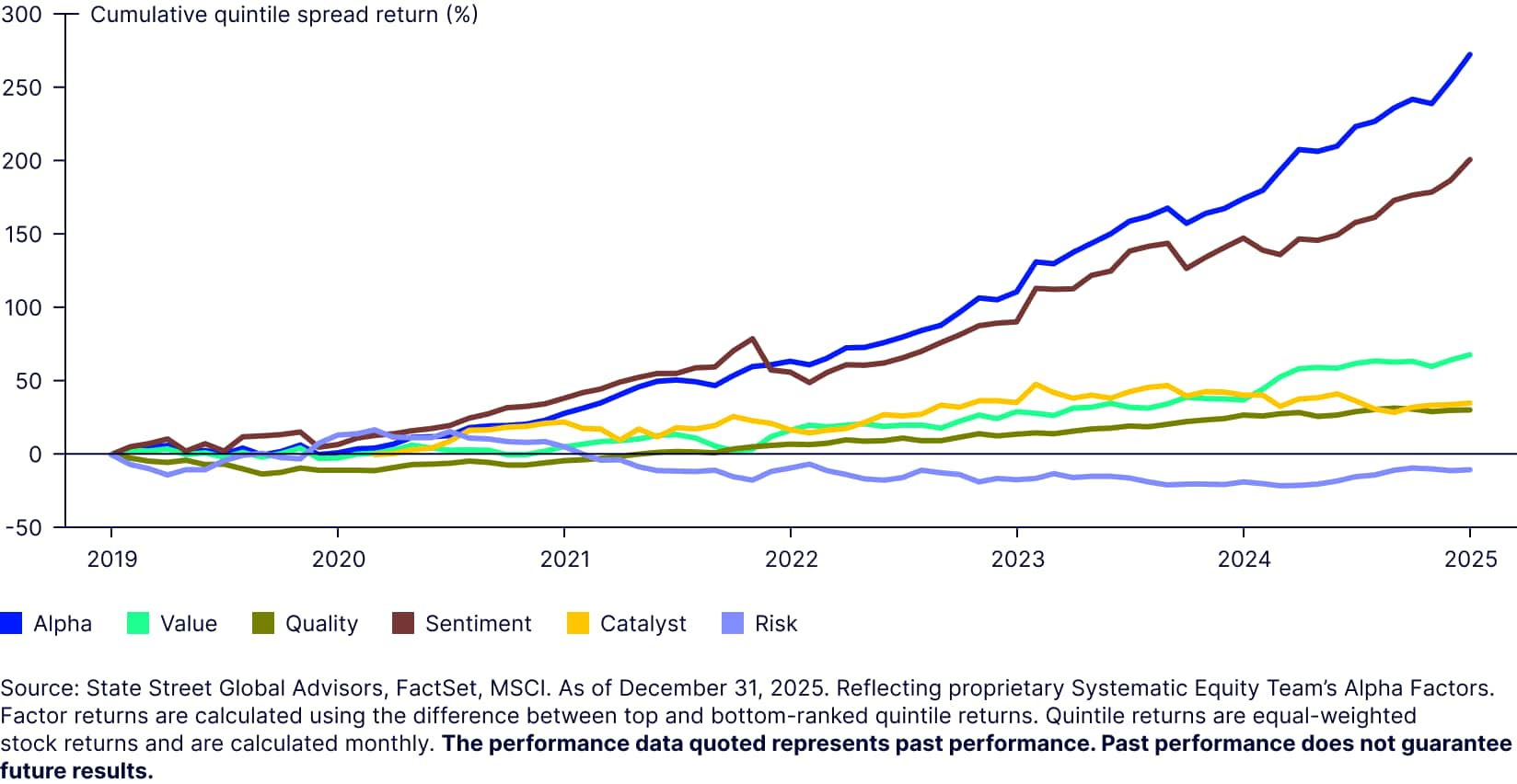

The charts below illustrate this dynamic by showing the return spread between the best and worst stocks as ranked by our factor models. While not a direct representation of portfolio holdings, they provide a clear and unbiased demonstration of our alpha signals’ effectiveness. At the total alpha level—the dark blue line—our model has delivered strong performance even through periods of significant global stress, including COVID related volatility and geopolitical disruptions.

Emerging Markets Large Cap

Emerging Markets Small Cap

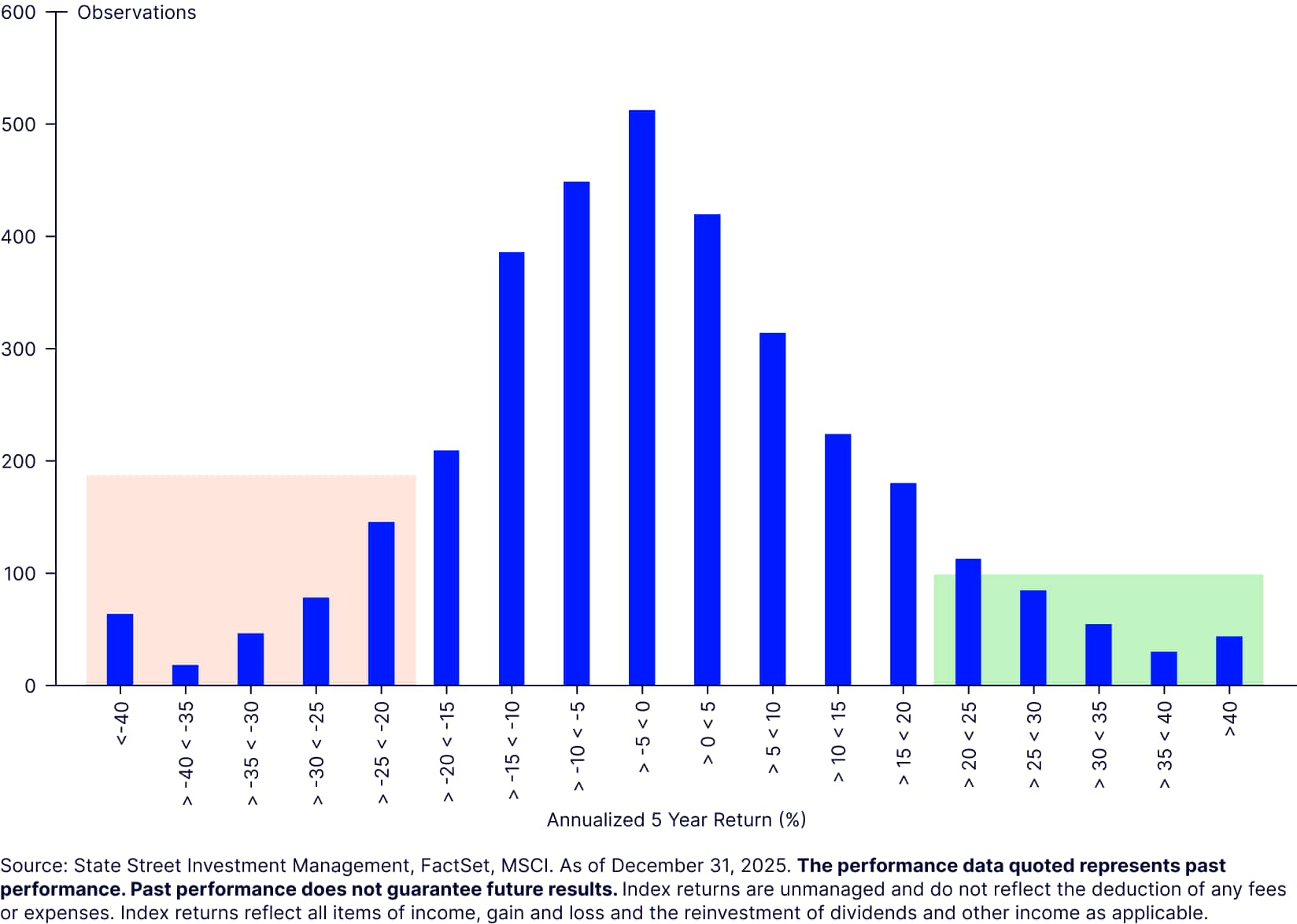

Most investors recognize that financial asset returns are often skewed, with non normal distributions (fat tails) and the ever present possibility of rare, extreme “black swan” events. While this dynamic exists across markets, it is especially pronounced in emerging market small cap equities. As shown in Figure 5, return distributions in this universe display far more observations in the tails than a normal distribution would suggest— particularly on the downside, where the negative tail has meaningfully more observations than the positive one. For skilled managers able to identify a handful of strong performers, this environment can create powerful alpha opportunities. But for concentrated portfolios, getting even a single position wrong can lead to long, painful recoveries. That is why our philosophy emphasizes broad diversification and disciplined position sizing— an approach well suited to a return profile where mitigating large losses is just as important as capturing big winners.

Figure 5: MSCI Emerging Markets Small Cap skew

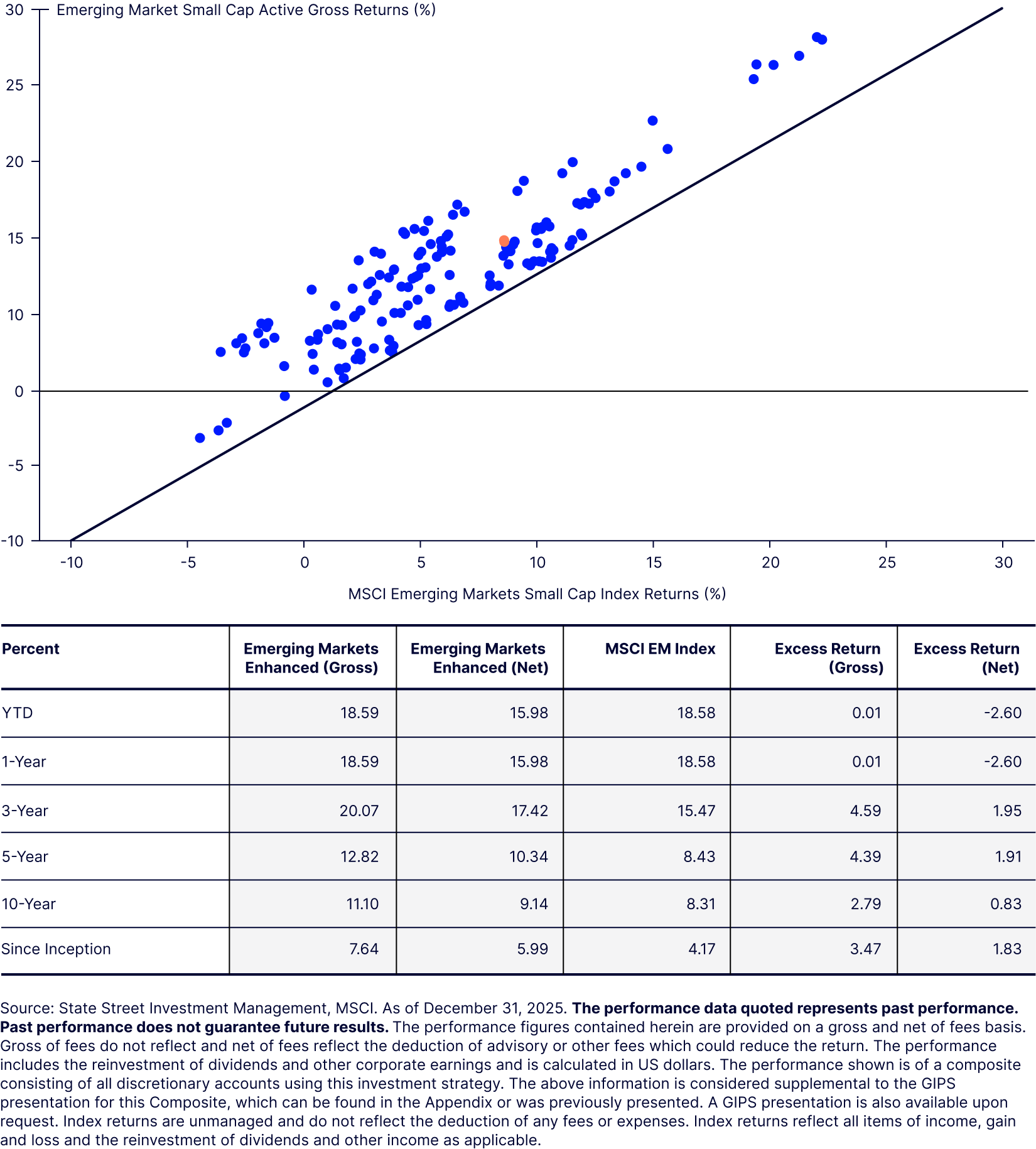

Our recommendation is simple: be diversified. Our team believes that incorporating security level risk and return factors as comprehensively as possible within the portfolio optimization process is one of the most effective ways to mitigate idiosyncratic tail risk. Our approach in the EMSC universe has been tested across multiple market cycles, and we can confidently point to a long, consistent track record of attractive risk adjusted returns. This is illustrated in Figure 6, which plots rolling five year excess returns for our Emerging Markets Small Cap Active Strategy back to its inception on October 1, 2007. On a gross basis, the strategy has delivered a 100% batting average, outperforming the benchmark in every rolling five year period since inception (86% on a net basis)—a result that underscores the power of disciplined diversification and position sizing in a market defined by fat tails and elevated idiosyncratic risk.

Figure 6: Our EM Small Cap Active Strategy has outperformed consistently

A compelling case for EM small caps

Emerging market small cap equities represent a distinct and opportunity rich universe—one best accessed by the right investor using the right approach. Their greater breadth, lower concentration, limited analyst coverage, and inherently non normal return patterns create an environment where a quantitative process with robust informational breadth is, in our view, the optimal way to capitalize on these opportunities.