How to determine your risk tolerance (and why it matters)

- Risk tolerance is easy to misconceive (and misapply) to portfolios.

- Knowing yours helps you set realistic expectations, avoid emotional decisions, and invest toward your goals.

- When your investments match your risk tolerance, volatility becomes more manageable.

Imagine stepping onto a casino floor.

The air hums—slot machines chime, dice clatter, voices rise and fall in every direction. Neon lights glow and pulse, illuminating every nook and cranny without a hint of daylight. It’s the textbook definition of sensory overload.

You scan the room. Past countless banks of whirring slot machines and boisterous craps tables, one game catches your eye: roulette.

After taking a seat between a bachelor party that lost track of time hours ago and a quiet regular who probably calls this his second home, you reach into your wallet.

But instead of pulling out the crisp Benjamin tucked between the fold, you slide a check across the table—a check that promises your entire life savings to the casino.

In exchange, the dealer hands you a towering stack of chips. You thank them. Then you place it all on black.

One spin could double your net worth.

One spin could erase all of your financial progress.

Just before spinning the fateful half-inch ball, the usually stoic dealer breaks and asks you a simple question: “How do you feel?”

Your answer to that question, in that moment, is your risk tolerance.

…

Most investing decisions aren’t nearly that dramatic. There’s no roulette wheel. No dealer. No single life-changing spin.

Still, the threat of loss is ever-present in markets, whether it’s a pullback in tech, an ominous headline about the economy, or a red number that feels a little too big to ignore. That’s where many investors realize something important: the risk they thought they could tolerate isn’t always the risk they can actually live with.

What is risk tolerance?

Risk tolerance is how comfortable you are with uncertainty and potential losses.

Said another way, it’s how much downside you can financially and emotionally handle without panicking, second-guessing your decisions, or abandoning your plan altogether.

Every investment has some level of risk. Assets like stocks and digital assets may deliver higher upside, but they also come with sharper swings and potential for greater downside over the short term. More conservative investments, such as bonds and CDs, usually fluctuate less, but that stability is often at the cost of lower returns over time.

You’ve probably heard that before, but it’s one thing to say you’re comfortable with ups and downs and another to watch your account balance—which may have taken years to build—reverse course, with no indication of stopping.

Your tolerance for risk comes from a combination of three important (and ever-changing) variables:

How you feel under stress

How you react to volatility

Your goals, timeline, and broader financial profile

This is different for everyone. One investor might not even blink at our casino experience, while another may feel queasy just reading through that hypothetical.

What risk tolerance is NOT

- It’s not how much risk you want to take. Most investors want higher returns. They like the idea of being aggressive—right up until the market drops. Wanting upside isn’t the same as being able to endure downside. Your appetite for risk and your tolerance for it are two very different things.

- It’s not how much you can afford to take. Some investors have higher risk “capacity” than others based on income, savings, time horizon, and other lifestyle obligations. That said, just because you can absorb more losses doesn’t mean you’ll sleep well doing it.

- It’s not tied to how much investment knowledge you have. Awareness is important and beneficial. But understanding markets doesn’t totally eliminate the stress. You can know exactly what’s driving the market down and still feel that pit in your stomach.

- It’s not a badge of honor. Being bold and daring in your personal or professional life doesn’t automatically translate to how you should approach investing.

- It’s not static. Life changes. So do markets. So does your relationship with money. Your comfort with risk in your 30s could look drastically different in your 40s.

None of this is to suggest risk is negative—in fact, risk is necessary to generate returns and build wealth. The challenge is understanding your relationship with risk so your portfolio supports your goals and your ability to stay invested during volatility.

Why understanding your tolerance for risk matters

Knowing your risk tolerance can help on several fronts:

If you expect steady, linear progress but your investments behave more like a rollercoaster, frustration is inevitable. Understanding your tolerance helps set realistic expectations about volatility, drawdowns, and recovery periods—so market swings don’t come as a surprise.

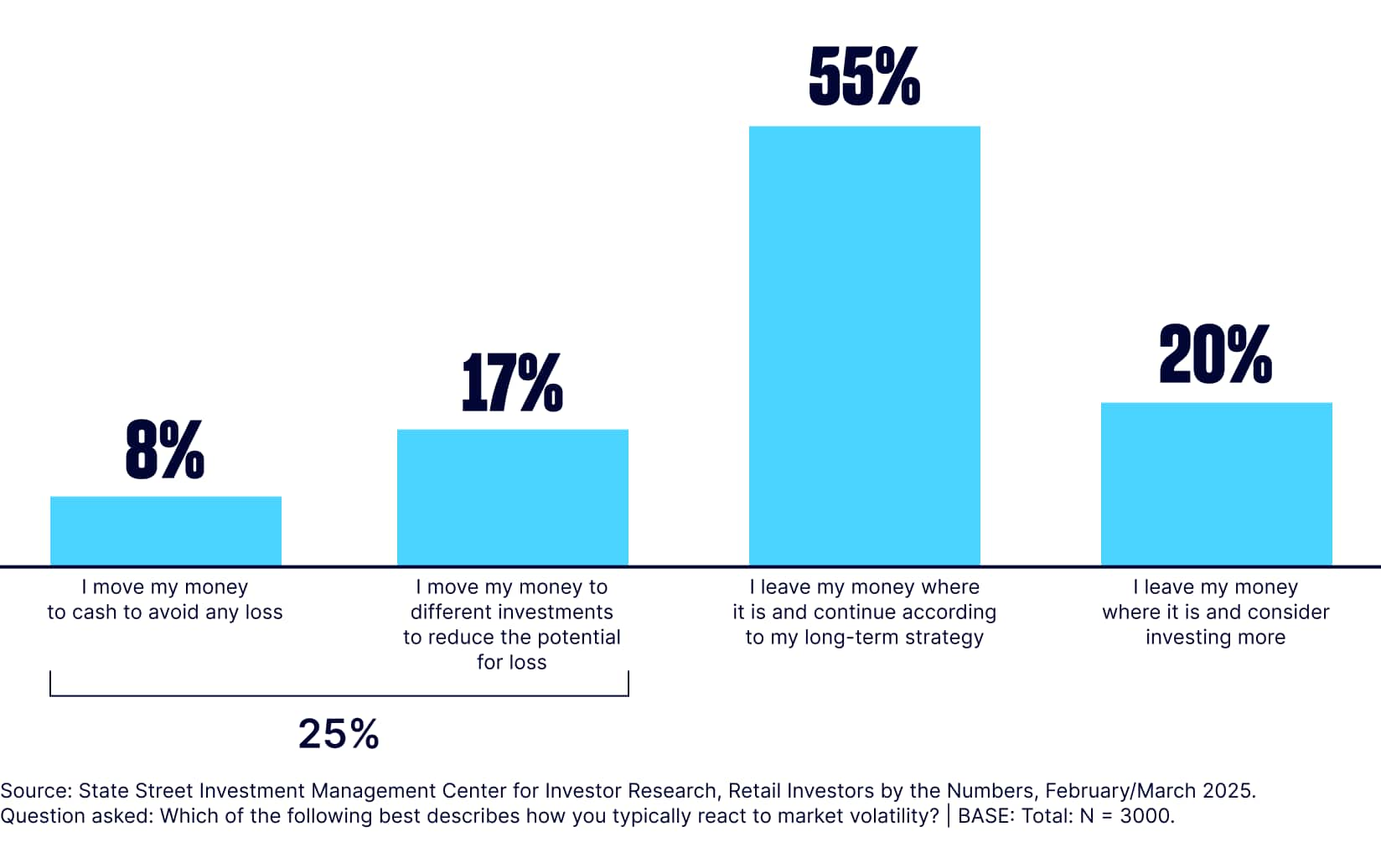

According to State Street Investment Management research, one in four (25%) investors say they panic-sell during market volatility, moving to safer investments or out of the market altogether.1

Figure 1: How retail investors typically react to market volatility

That can help alleviate anxiety and doubt in the moment, but it also pulls you out of the market, which could cause you to miss the recovery and future gains (not to mention the tax implications of realizing any profits).

Knowing your comfort level can act as a reference point if emotions are running high, even during bull markets when greed can be just as influential as fear. Awareness helps you pause, reassess, and avoid reactive decisions driven by short-term stress rather than long-term goals.

What factors influence your risk tolerance?

Your tolerance for risk is a lot like your tolerance for bad weather. A little rain might not bother you. A thunderstorm? Still manageable, with precautions. But the thought of being in the same state as a tornado, let alone sheltering through one, could be an outright dealbreaker for you.

Market volatility works in a similar way. Several factors influence how much uncertainty you can sit through before that inner voice pushes you to do something.

Time horizon

One of the biggest drivers of risk tolerance is how long until you need the money in your portfolio.

If you’re investing for a goal that’s decades away, you generally have more time to recover from downturns or pullbacks. Short-term volatility might sting, but it’s less damaging if you’re not planning to tap into funds anytime soon. On the flip side, if the goal (like a down payment) is in the next few years, even modest swings can feel much more consequential.

Ask yourself these questions:

- When will I realistically need this money?

- Would short-term losses delay my plans?

- How would I feel if my portfolio lost 20% one year?

Current goals and responsibilities

Risk tolerance doesn’t exist in a vacuum—it’s interwoven into everything else going on in your life.

Supporting a family, paying a mortgage, caring for aging parents, or running a business can all change how much uncertainty you’re comfortable absorbing. Even positive life events can shift your tolerance. A promotion, inheritance, or career pivot may change your relationship with risk.

Ask yourself these questions:

- What financial responsibilities depend on this money?

- Would a downturn force me to change my lifestyle or plans?

- Am I investing for growth, stability, income, or a mix of all three?

Emotional response to loss

No spreadsheet or risk tolerance questionnaire can truly calculate how you’d feel if your portfolio declined by half.

Some investors can watch their portfolio plummet without losing sleep. Others feel heartburn after a single down day. Neither reaction is “wrong,” but ignoring it can lead to decisions you might later regret.

Importantly, how you think you’ll react and how you actually react are often very different.

Questions to ask yourself:

- How did I feel during the last market downturn?

- Did I check my accounts more frequently or avoid them altogether?

- Have I ever sold investments to primarily feel relief?

Relationship with money

Your own history with money is an overlooked but major influence on your tolerance for risk. Investors who lived through major downturns early in their lives (whether they were investing yet or not) may be more cautious. Others who only know prolonged bull markets or brief bear markets may feel more comfortable taking risk.

Personal experiences outside investing are a factor too. Job insecurity, unexpected expenses, or financial stress can all impact how much uncertainty you’re willing to tolerate.

Questions to ask yourself:

- Have any events or financial experiences shaped how I view risk?

- Have I ever avoided investing because I feared mistiming the decision?

- Is there a past investing decision I still think about or regret?

How do you respond to risk when it counts?

Our exclusive report explores how 3,000 retail investors handle high-stakes decisions, market swings, and uncertainty—revealing what really drives their financial choices.

What are the different levels of risk tolerance?

Aggressive, moderate, and conservative—while everyone’s situation is unique, most investors generally fall into one of these three broad risk tolerance categories.

Aggressive

Investors with an aggressive risk tolerance are more comfortable accepting larger short-term losses in pursuit of higher long-term growth. They typically have longer time horizons, fewer near-term liquidity needs, and the emotional resilience to ride out sharp market declines without wavering. While this approach can unlock greater growth potential, it also requires strong conviction and the ability to stay disciplined when (not if) markets test patience.

Moderate

Investors with a moderate risk tolerance are willing to accept some short-term volatility and losses in exchange for higher long-term returns. This is the proverbial middle ground—balance between enough risk to grow wealth, but not so much that market swings disrupt confidence or discipline.

Conservative

Investors with a conservative risk tolerance are less willing to accept near-term losses, even if it means giving up some long-term growth potential. They tend to prioritize stability and capital preservation, preferring portfolios that aim to limit volatility and drawdowns. This approach may reduce stress during market downturns, but it often comes with the tradeoff of slower growth over time—especially after inflation.

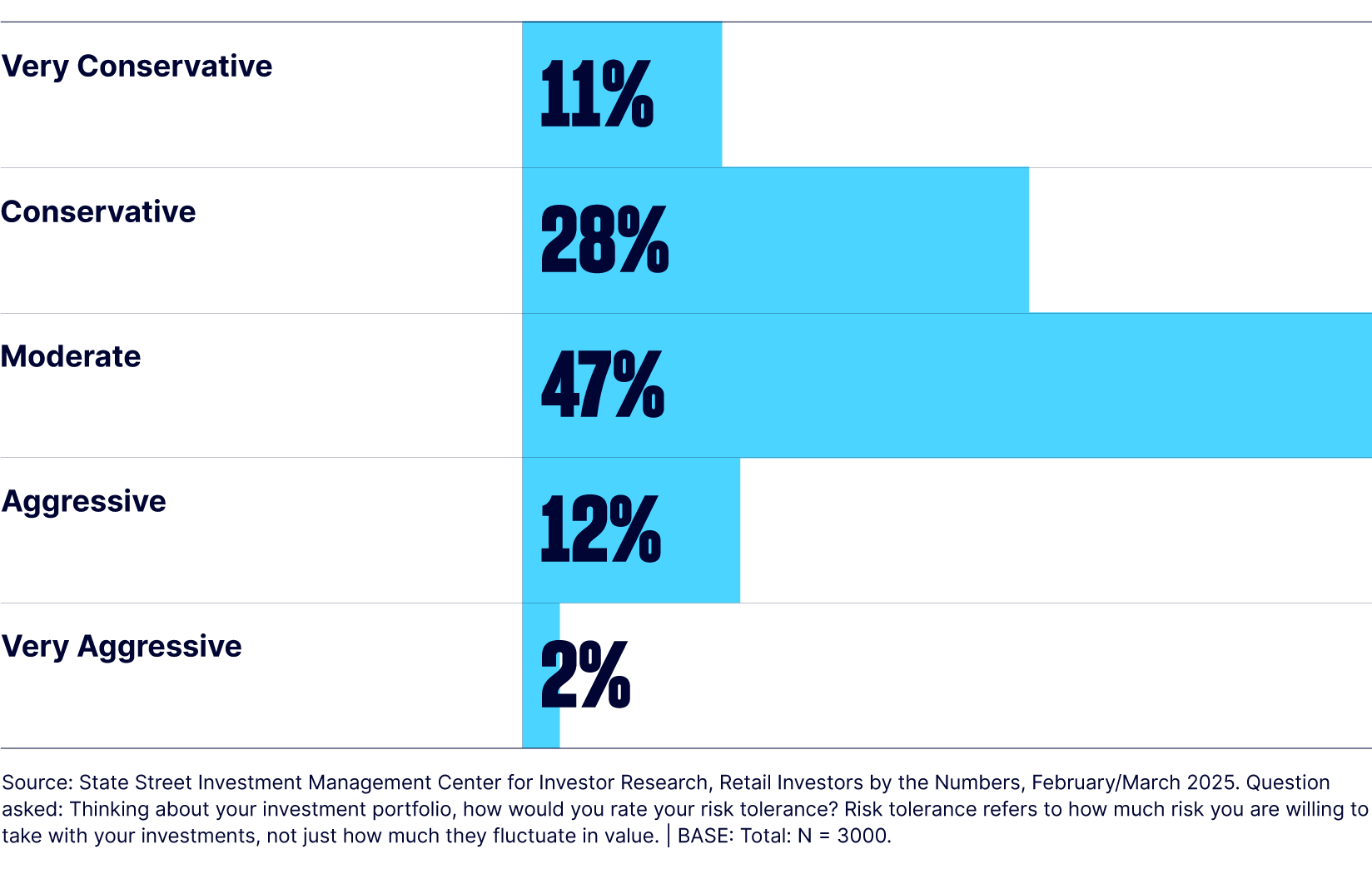

Figure 2: How today’s retail investors describe their investment portfolio’s risk tolerance

Broadly speaking, aggressive investors typically favor growth-oriented assets like stocks. Conservative investors typically prefer investments designed to dampen volatility and preserve capital, like investment grade bonds and CDs. And, as you’d expect, moderate investor portfolios have a balanced mix of both.

How can you determine your risk tolerance?

Nothing can simulate or match firsthand exposure to loss and how you’ll feel in that moment. Still, a little introspection goes a long way.

Quick quiz

1. The market drops 20%. Your portfolio has lost its gains from the past 12 months. Headlines are bleak. Everyone’s all but certain we’re entering a recession. Which reaction feels most like you?

a. You feel uneasy but stay invested.

b. You reduce some exposure to stocks to put your mind at ease.

c. You move most of your portfolio to cash or safer investments to stop the bleeding.

2. Looking back at past financial decisions, which feeling do you recognize more often?

a. Regret from being too cautious and missing opportunities.

b. Regret from decisions that, in hindsight, were too risky.

c. A mix of both—sometimes too cautious, sometimes too bold.

3. Your portfolio is up. Friends are bragging about an up-and-coming tech stock doing even better. This could accelerate your goal timeline if it pans out or delay it. What are you inclined to do?

a. You make no changes.

b. You make a modest allocation.

c. You make a substantial allocation.

Now what? Turn risk tolerance awareness into action

Once you have a better sense of your risk tolerance, then you can use it to make more informed and disciplined decisions.

How so? We’re glad you asked.

- Align risk in your portfolio with your time horizon. Short-term goals (money you’ll need in one to three years) generally call for more stability. Longer-term goals can tolerate more volatility—as long as you’re emotionally prepared to stay invested.

- Write it down—seriously. Document your risk tolerance. Note how you expect markets to behave, how much volatility you’re willing to tolerate, and what you won’t do during downturns. Consider this your personal investing “rulebook.”

- Use your plan as a guardrail. Volatility is inevitable. When it occurs, revisit your plan, particularly what you’re investing toward and how you may react to periods of market stress. This can help counter any urge to react emotionally.

- Reassess your tolerance as life changes. Career pivots, family dynamics, and evolving priorities can all affect how much risk feels appropriate. At least once a year, run a “self-diagnostic” and see if your risk tolerance has changed.

Ultimately, understanding your risk tolerance should help you develop an investment approach you can live with—through bull runs, volatile periods, and everything in between.

You can’t eliminate risk, but you can manage it

Most people like to believe they’re cool, calm, and collected investors…until the market drops and suddenly they’re refreshing their portfolio like they’re tracking a late (and directionally challenged) Uber.

It’s a natural and even expected reaction. Watching account balances dip is painful, especially considering there’s no way to confirm when the drop will end—it’s like being on a rollercoaster blindfolded, except your wealth is at stake versus your lunch.

That’s why it’s important to understand risk and, more importantly, your risk tolerance. Once you do, you’ll be better equipped to make grounded, disciplined decisions that allow you to invest confidently toward your goals.

Fewer refreshes. More confidence.

When you understand both your risk tolerance and the tools you can use to invest properly, decisions are far easier. Visit our ETF Education Hub to learn how ETFs can support different goals, timelines, and comfort levels.