6 Behavioral biases every self-directed investor should know

- Behavioral biases affect everyone—yes, even experienced investors.

- Recognizing common patterns (like herding, overconfidence, and loss aversion) can help you navigate markets with more confidence.

- Pairing that awareness with a clear investment strategy? That’s where things start to click.

Many self-directed investors have a major commonality with tried-and-true, travel influencers you see on social media: they like to take the road less traveled.

Think about it. They both do their own research. They both trust their instincts and value their independence. And yes, they’re both a bit suspicious to follow the crowds when “everyone else is doing it.”

But investing, like travel, rarely unfolds on an empty road.

There’s noise, detours, unexpected traffic (usually when you’re already running late). And every so often, you hit a stretch where you stop and think: “Am I still going the right way?”

That feeling? Totally normal.

Markets have a way of testing even the most well-thought-out plans. Not because you’re doing anything wrong, but because our brains aren’t exactly wired for long-term investing horizons. They’re wired for right now.

The good news: awareness can help.

Sure, it doesn’t ultimately eliminate uncertainty. But it can help you recognize common routes, anticipate congestion, and make more intentional choices about where to go next.

Below are six common behavioral patterns self-directed investors may face. Recognizing them could help you stay on course toward your long-term goals.

Pattern 1: Following the crowd (or herding)

You’ve seen this before.

A stock starts gaining traction. Headlines turn positive. Conversations (on Reddit or your preferred investment news source) pick up. Suddenly, it feels like everyone has an opinion—and most of them are pointing in the same direction.

That’s herding: the tendency to follow the actions of others, especially when things feel uncertain (or exciting…or both).

How it impacts investors

According to our research, about three in 10 investors admit to investing in trends primarily because they were popular at the time (Figure 1).1 The challenge is that popularity doesn’t always equal long-term potential.

While investing in what’s popular can feel reassuring in the moment, it often leads to buying after prices have already moved and second-guessing when momentum fades.

How awareness helps

Market enthusiasm is cyclical. There will always be a “next big thing.” That part doesn’t change.

What can change is how you respond to it.

A simple question can help create space between the noise and your decision-making: “Would I still make this investment if no one else were talking about it?”

If the answer is yes, great. If not, it may be worth revisiting your rationale.

Staying anchored to a defined strategy—clear allocation targets, regular rebalancing, and a focus on the fundamentals—can help you follow your plan, not just the crowd.

Pattern 2: Trying to time the market

Everyone wants to get timing right. Buy at the bottom. Sell at the top. Move at the exact “right” moment.

The problem is, those moments are only obvious in hindsight.

In real time, markets don’t offer clear signals—they offer uncertainty. And that uncertainty can make it tempting to wait for better conditions before making a move.

How it impacts investors

Nearly half of investors (46%) say performance is their top concern when managing their investments (Figure 2).2

Figure 2: The investment management concerns that worry self-directed investors

Ranked in order of importance

| Self-directed investor concerns with managing investments | Total % of surveyed investors |

|---|---|

| Performance | 46% |

| Market volatility | 42% |

| Fees | 43% |

| Achieving your goals | 36% |

| Lack knowledge or expertise | 31% |

| Mistiming the market (i.e., buying or selling at the wrong time) | 21% |

| Making decisions based on incomplete or unclear information | 20% |

| Not diversifying enough | 21% |

| Allowing emotion or fear to influence my decisions | 19% |

Source: State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: Which, if any, of the following are you concerned about with respect to managing your investments? | BASE: Self-directed Only: N = 1773

So it’s understandable why timing feels like something worth trying to get right.

But in practice, it often leads to hesitation on the way in, reactive decisions on the way out, or re-entering after markets have already recovered. In other words, a lot of movement without much progress.

Here’s the part that’s easy to overlook: some of the market’s strongest days tend to happen during periods of volatility—when investors are most likely to step away. Missing even a small number of strong market days can significantly affect long-term outcomes.

Let’s say you missed the 20 best trading days between 1995 and 2025. Your returns would be cut by roughly half in comparison with the investor who stayed in the market. Of course, that may seem easy to point out in retrospect. But those “best days” tend to happen during bear markets and extreme volatility—like during the 2008 financial crisis or the COVID-19 pandemic (Figure 3). In other words, when people are most likely to panic.

How awareness helps

Perfect timing isn’t a requirement for long-term success. Consistency tends to matter more.

Automating contributions—whether weekly, monthly, or quarterly—can help you stay invested across different market environments without having to make constant judgment calls.

It’s less about finding the perfect moment, and more about staying in motion.

Invest like you’re going places. Because you are.

Wherever you’re headed, State Street Investment Management can help you get there.

Pattern 3: Prioritizing comfort over progress

We’re hardwired to prefer comfort. Especially in the short term.

In investing, that can show up as holding more cash than needed, delaying investment decisions, or pulling out of the market when things feel uncertain.

This tendency is often referred to as present bias, favoring what feels safe or reassuring today over what may benefit us in the future.

How it impacts investors

On average, self-directed investors allocate more of their surplus income to saving (60%) than investing (40%) (Figure 4).3 That can be intentional: building a buffer, preparing for near-term needs, or simply staying cautious.

None of those things are inherently wrong. But over time, keeping too much on the sidelines can limit the role compounding plays in growing wealth. Because in investing, time isn’t just helpful—it’s foundational (Figure 5).

How awareness helps

This isn’t about choosing between comfort and progress. It’s about finding the right balance between the two.

Maintaining an appropriate level of cash for short-term needs (often three to six months of living expenses) can provide stability. At the same time, keeping the rest of your portfolio invested can help ensure your long-term goals continue moving forward. Said another way: prepared for today, positioned for tomorrow.

Pattern 4: Letting recent events drive decisions

When something is fresh in your mind, it tends to carry more weight:

- A recent market drop can make risk feel elevated

- A strong rally can make gains feel more certain than they are

- A headline or conversation can start to feel like a signal

That’s availability bias (or recency bias), our tendency to rely on information that’s most recent or easiest to recall.

How it impacts investors

More than six in 10 investors say they tend to rely on readily available information when making decisions (Figure 6).4

While recent information isn’t irrelevant, it’s often incomplete. When short-term events start to outweigh long-term thinking, decisions can drift away from the original plan—sometimes without it being obvious in the moment.

How awareness helps

Markets will always generate headlines. Some more urgent-sounding than others. The key is having a framework that helps you step back and assess what actually matters.

A clearly defined investment strategy can act as that anchor, providing context for what you’re seeing and help you base decision-making on long-term direction rather than short-term noise.

Pattern 5: Overestimating (or underestimating) your own abilities

Confidence plays an important role in investing. It helps you take action, stay committed, and trust your decisions.

But like most things, it works best in balance.

Too much confidence can lead to overestimating your ability to outperform the market. Too little can lead to hesitation or missed opportunities.

How it impacts investors

About 35% of self-directed investors believe their portfolio management skills can help them outperform the market (Figure 7).5 Yet at the same time, only 51% of self-directed investors report feeling confident making investment decisions.6

Both ends of the spectrum can create challenges.

Overconfidence can lead to frequent trading or overconcentrated positions. But a lack of confidence can result in staying on the sidelines or second-guessing decisions.

How awareness helps

The goal isn’t to eliminate confidence it’s to keep it grounded. That’s where structure can help:

- Diversifying across asset classes

- Setting clear allocation limits

- Avoiding overexposure to a single investment

Some investors also find it useful to document their decisions—noting why they made them and what they expected. Looking back can provide helpful perspective (especially when memory starts rewriting the story).

TL;DR: Confidence should support your strategy, not override it.

Pattern 6: Reacting strongly to losses (loss aversion)

Losses tend to feel twice as painful as equivalent gains feel rewarding.7 That’s not just perception—it’s a well-documented behavioral tendency.

And in investing, it can lead to decisions that prioritize short-term relief over long-term outcomes.

How it impacts investors

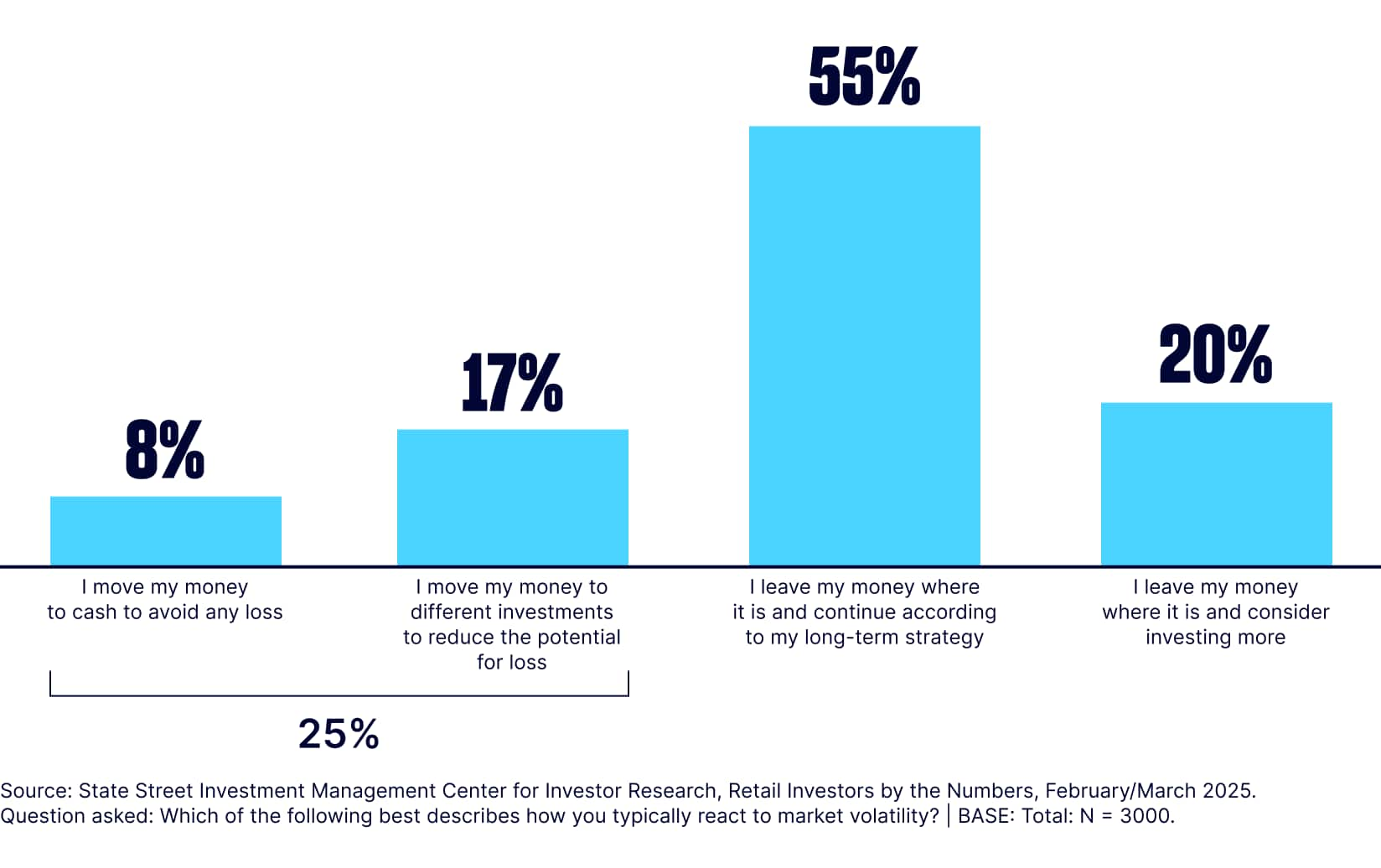

Market volatility is one of the most cited concerns among self-directed investors.8 In response, about 25% report selling investments elsewhere to minimize losses (Figure 8).9

Figure 8: 25% of self-directed investors move their money when volatility strikes

In the moment, it can feel like regaining control.

But stepping out during downturns often means missing the recovery that follows—and interrupting long-term growth in the process.

How awareness helps

Volatility is a natural part of investing. Not a signal that something has gone wrong.

When markets decline, it can help to shift focus: From short-term account balances to long-term time horizons and the role those investments are meant to play in your portfolio.

Diversification can also reduce the impact of any single investment, making it easier to stay invested through periods of uncertainty.

Because while volatility can be uncomfortable, reacting to it isn’t always productive.

Awareness is the first step toward better investing

No, investing toward your goals is never going to be smooth sailing. There will be moments of uncertainty. Points where the path feels less clear. Times when staying the course requires a bit more intention.

That’s not a sign of failure, it’s part of the process. Our instincts weren’t built for long-term investing. They were built for quick decisions and immediate outcomes.

Awareness helps bridge that gap.

It doesn’t remove uncertainty, but it can help you recognize when a reaction is being driven by instinct rather than strategy—and give you the space to respond more thoughtfully.

Over time, those small moments of awareness can add up: helping you stay aligned with your goals, more confident in your decisions, and better equipped to navigate whatever the market puts in front of you.

DEEPEN YOUR AWARENESS

Get more insights from investors like you

This exclusive report explores the money habits of 3,000 retail investors—and can help you uncover new perspectives on your own financial mindset.