Understanding the ETF Liquidity Ecosystem

Liquidity is one of the most important features attracting a diverse group of investors to exchange traded funds (ETFs). Here, we explain the mechanics of ETF trading and the roles played by key members of the liquidity ecosystem.

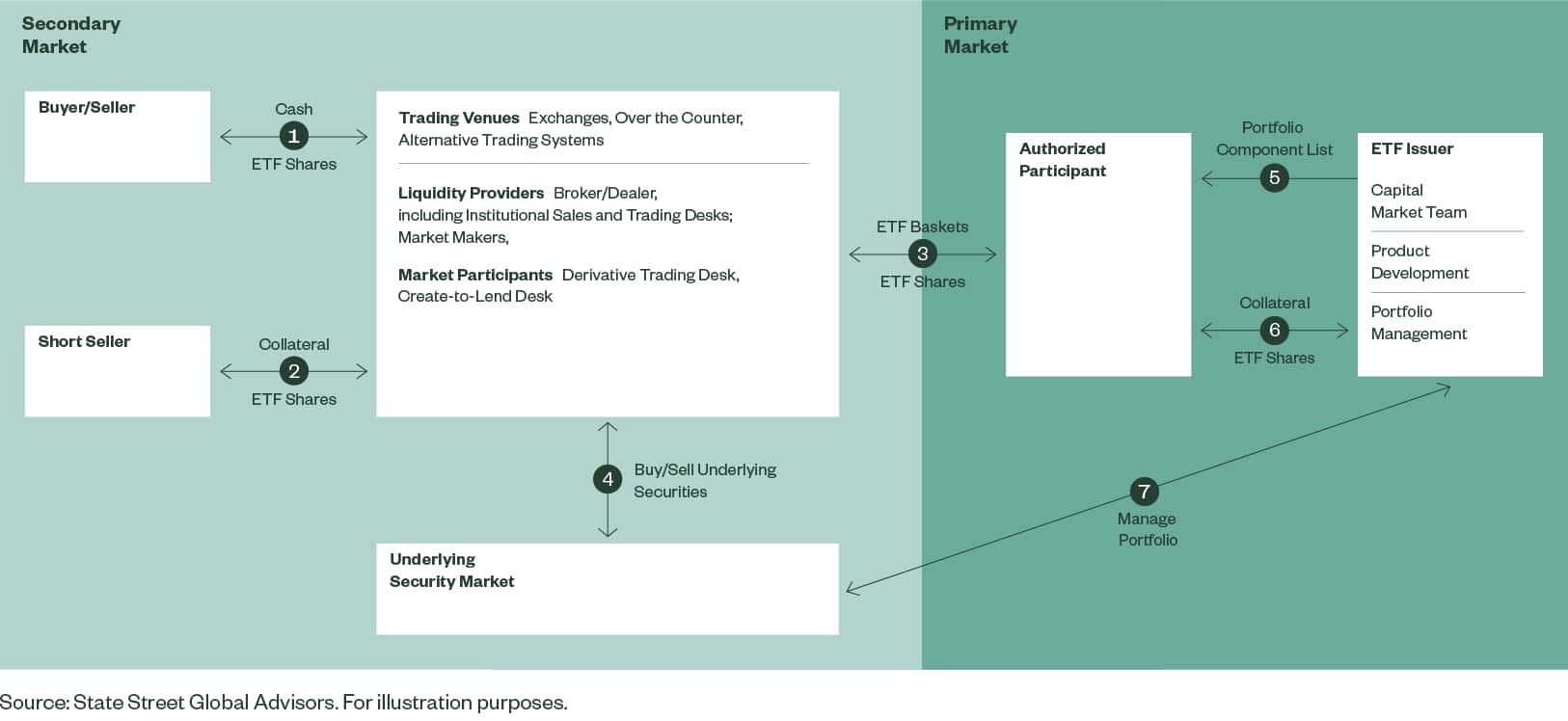

An ETF is an investment vehicle whose shares trade intraday on stock exchanges at market-determined prices. ETFs are unique in that they offer two markets for trading — the secondary market, where most investors trade, and a primary market that supports the ETF’s liquidity and allows it to trade close to Net Asset Value throughout the day.

Figure 1: The ETF Liquidity Ecosystem

The below explains the key ETF trading activities highlighted in Figure 1.

- Buyers and sellers of ETF shares place their orders through registered brokers and exchange cash for ETF shares when buying and vice versa for selling.

- Short sellers pay a fee to the lender to borrow ETF shares to sell in the market, buy them back later on at a lower price to lock in a profit, and then return them to the lender. In exchange for ETF shares, the short seller provides collateral, which is typically required to be of higher value than that of the borrowed shares.

- When the demand for ETF shares exceeds or falls short of the shares available for sale in the secondary market, there will be disparities between the ETF market price and its intrinsic value (NAV) based on underlying security prices. The primary market then provides additional liquidity, as market makers will engage Authorized Participants (APs) to create/redeem ETF shares to balance the supply and demand, keeping ETF share prices close to their intrinsic value. Market makers will deliver ETF baskets to the AP in exchange of ETF shares.

- Before creating ETF shares, market makers might need to source underlying securities in the ETF basket by tapping into their own inventory or purchasing from the underlying security market. In some instances, the ETF issuer might also accept cash-in-lieu as part of the ETF basket and purchase those securities directly from underlying security markets for the fund and charge related costs to the market maker. This process happens in reverse with redemption orders, if market makers need to liquidate the ETF basket delivered from the AP and return the proceeds to the seller of ETF shares. In the end, creation and redemption of ETF shares in the primary market may result in transactions in underlying security markets.

- At the end of each trading day, the ETF issuer publishes the Portfolio Component List, which includes the security names and corresponding quantities that comprise the ETF basket for the next trading day.

- The AP creates/redeems ETF shares by exchanging securities in the basket for shares of ETFs, or vice versa.

- ETF portfolio managers buy or sell underlying securities to manage corporate actions (e.g., dividend payments, mergers and acquisitions, spinoffs), index reconstitution and cash flows to realign portfolios with their benchmark and minimize tracking error. These transactions may impact the liquidity of underlying security markets.

Who Are the Major Liquidity Players in the ETF Market?

ETFs’ unique creation and redemption process and secondary market trading involve a number of capital markets participants who contribute to the ETF liquidity ecosystem, including:

- Exchange While ETFs are generally listed on one exchange, trading of ETF shares occurs across many trading venues. These include national securities exchanges; alternative trading systems; and over the counter.

- Broker/Dealer Brokers and dealers execute trades on behalf of clients by routing orders to trading venues or by matching buyers and sellers directly. Dealers buy and sell securities for their own account. They charge commissions for their services to execute and settle trades.

- Institutional Sales and Trading Desk Some brokers have a dedicated Institutional Trading Desk that specializes in facilitating execution of large trades at defined prices. They may quote a market for a given ETF at a given size (risk trade) or act as an AP to place a creation or redemption order on the client’s behalf with the ETF issuer (end-of-dayNAV trade).

- Authorized Participants (AP) APs are the only counterparties allowed to enter creation and redemption orders with the fund. They are typically entities that serve many functions, including acting as dealers in ETF shares in the secondary market and acting as an agent for market makers and other liquidity providers to create/redeem ETF shares.

- Market Makers Simultaneously making offers to buy (bid) and sell (ask) securities at specified prices, market makers provide two-sided liquidity to other market participants. They facilitate the exchange of securities between end investors by bridging the gap between the time when natural buyers and sellers enter the market. Market makers profit from the spreads of their bid-ask quotes as well as arbitrage opportunities between an ETF’s NAV andits market price. This also helps with price discovery and keeps the ETF prices in line with its NAV.

- Derivative Trading Desk Derivative trading desks actively transact in the underlying ETF to dynamically hedge their position(s), as they facilitate transactions on a variety of financial instruments for institutional clients. Additionally, ETFs seeking to track indices linked to other structures such as swaps and futures are often used in relative value arbitrage between vehicles.

- Short Sellers Short sellers provide liquidity, as they tend to be selling into demand when share prices appreciate, and conversely looking to buy back shares when prices decline. For example, if most investors are optimistic about the asset’s future performance, ETF share prices increase, leading to more demand of ETF shares. Short sellers who hold a contrarian view will borrow shares from brokers and sell them when there is more demand for purchases and buy them back later, when most investors are selling.

- Create-to-Lend Desk Create-to-Lend Desks create ETF shares (through an AP) for the purpose of lending them to clients seeking to borrow the shares. They usually hedge their positions to minimize price risks.

Each of these capital markets players contributes to ETFs trading more efficiently throughout the day, which benefits both buyers and sellers. There are also economic benefits for the capital markets participants.

Who Are the ETF Issuer’s Liquidity Players?

The ETF issuer develops ETF products, determines fund investment objectives, manages the ETF portfolio according to the fund’s objectives and oversees day-to-day operations. Within the organization, these three functions deal with market liquidity:

- Portfolio Manager and Trading Desk Portfolio managers manage the ETF portfolio, seeking to achieve the investment objective. They determine the composition of ETF baskets. Portfolio managers’ trading desks execute trades as directed by portfolio managers. They work with liquidity providers of underlying securities to source liquidity, minimize trading costs and seek best execution.

- Capital Markets Team Building relationships with APs, exchanges, market makers, trading desks/platforms and other liquidity providers, the capital markets team plays an active role in promoting competitive markets to improve the ETF liquidity ecosystem. Given their relationship with market participants and insight into primary and secondary market activity, they are a critical resource for investors looking to execute large ETF trades efficiently.

- Product Development ETFs rely on arbitrage activities to keep the fund’s market price in line with its NAV. Therefore, when designing an index for an ETF to track, the product development team ensures the ETF basket is liquid enough to efficiently manage the fund from a liquidity perspective. This, in turn, allows market participants to effectively create/ redeem ETF shares and keep prices in line with NAV.

- Liquidity Risk Management The liquidity risk management team monitor fund underlying asset liquidity and funding liquidity using a variety of risk metrics and quantitative models in normal and stress scenarios to ensure the ETF’s ability to meet client redemption in a fair and orderly manner. They engage with portfolio managers, traders, product managers and other stakeholders to address any liquidity issues identified.