Global Equities: A Shift in Performance Drivers

As a soft landing became the base case scenario in the United States and a deep recession is likely to be avoided in other regions, global equities rallied — with the S&P 500® Index, the STOXX Europe 600 Index, and the Nikkei 225 all setting new record highs.

The environment has become increasingly supportive for equities as economies, particularly the US, surprise to the upside, demonstrating resilience to monetary tightening. We also expect disinflation to continue, while acknowledging that inflation entrenchment and geopolitical challenges remain key risks. 2023 was a year of US exceptionalism and this extraordinary strength is likely to remain intact. Expect even more pronounced US-centricity in 2024 with elections, inflation prints, economic growth, and earnings for US companies determining the prospects for equity markets around the world.

Earnings Prospects More Important Than Yields

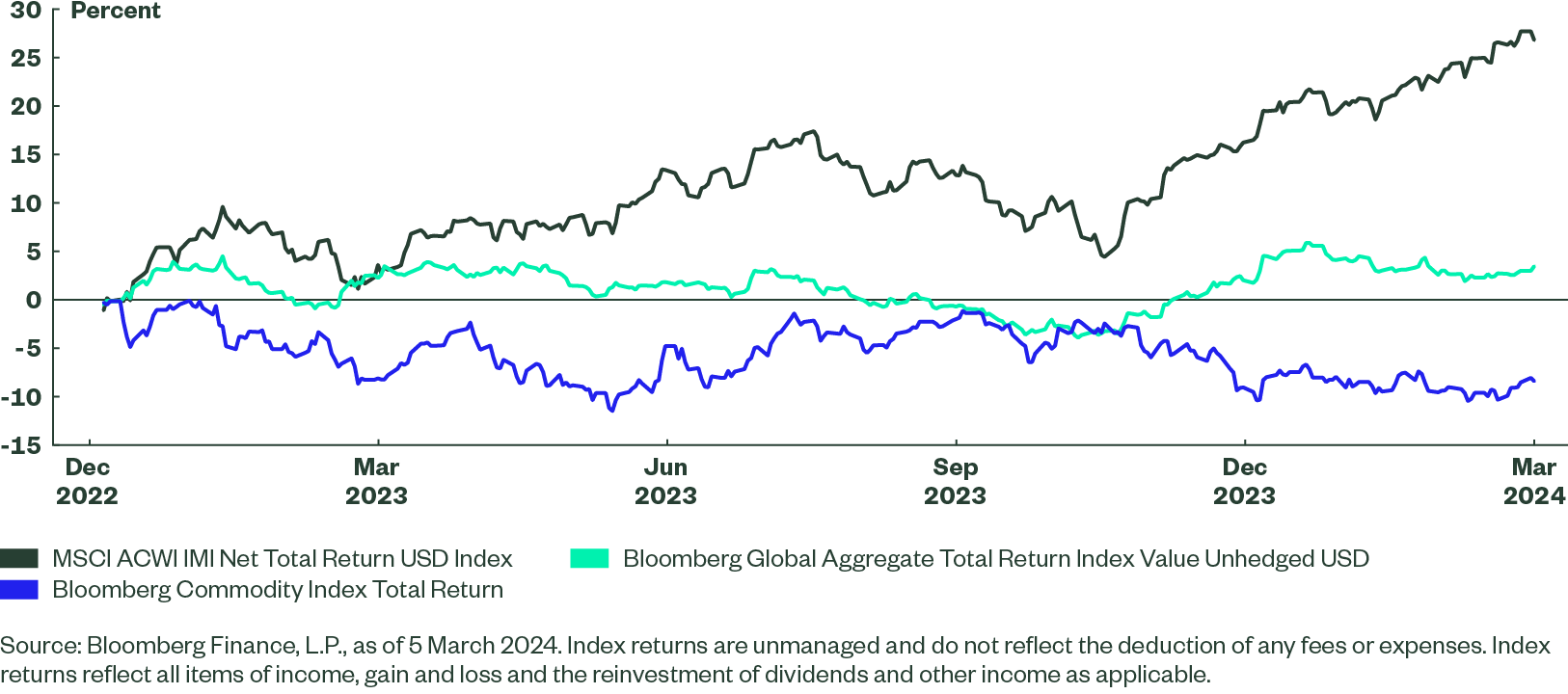

Over the course of 2023, equity return volatility was driven by both AI developments and interest rate prospects, with not only higher inflation but also a stronger-than-expected labour market leading to temporary drawdowns. Meanwhile, inflation undershot in November, leading to a broad-based market rally at year-end. However, since January we’ve observed a shift in investor perceptions as traders have reset their expectations around the rate path, with the number of expected cuts in 2024 falling from nearly 6.5 at year-end to 3.5 as of March.1 Nevertheless, equity returns once again outpaced other asset classes as businesses — through Q4 earnings — demonstrated their ability to grow their bottom line despite higher rates. This resiliency may be the key element to broadening market performance globally, beyond a handful of tech-related stocks. With rate cuts on the horizon, the market environment for global equities is becoming increasingly benign.

Figure 1: Performance Since the Beginning of 2023

Global Economy Is Likely to Avoid a Major Crisis

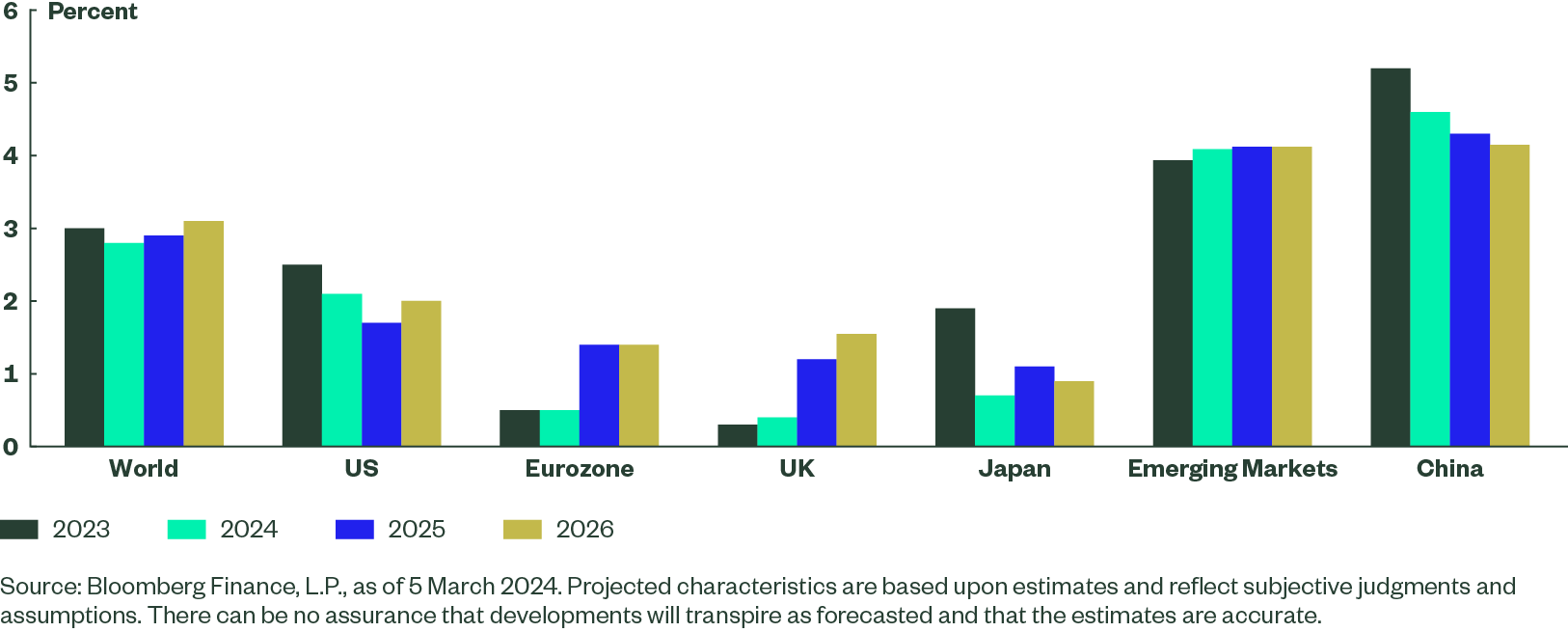

Although the dispersion of the economic expansion remains wide across key developed economies, the common theme is that the growth has been better than was feared. US GDP increased at a 3.3% annualized rate in Q4, with growth for the full year at 2.5%, against consensus of economists pointing to just 0.3% at the start of the year. Clearly, the US consumer’s willingness to spend was underappreciated, as was the impact of fiscal programs. Europe is balancing on the edge of a recession but flat growth means that a severe crisis, which would be disruptive for equities, seems likely to be avoided. Japan, which has thus far been supported by a weak Yen, entered a technical recession. But it is expected to benefit from Shunto-driven wage growth, which may boost more domestic portions of stocks. China remains a key concern. While the country accounts for only 2.4% of the MSCI ACWI IMI Index and is not included in the developed-only MSCI World Index,2 China remains a vital part of the global economy and geopolitical landscape.

Figure 2: Expected Real GDP Growth

PMIs May Have Bottomed Out

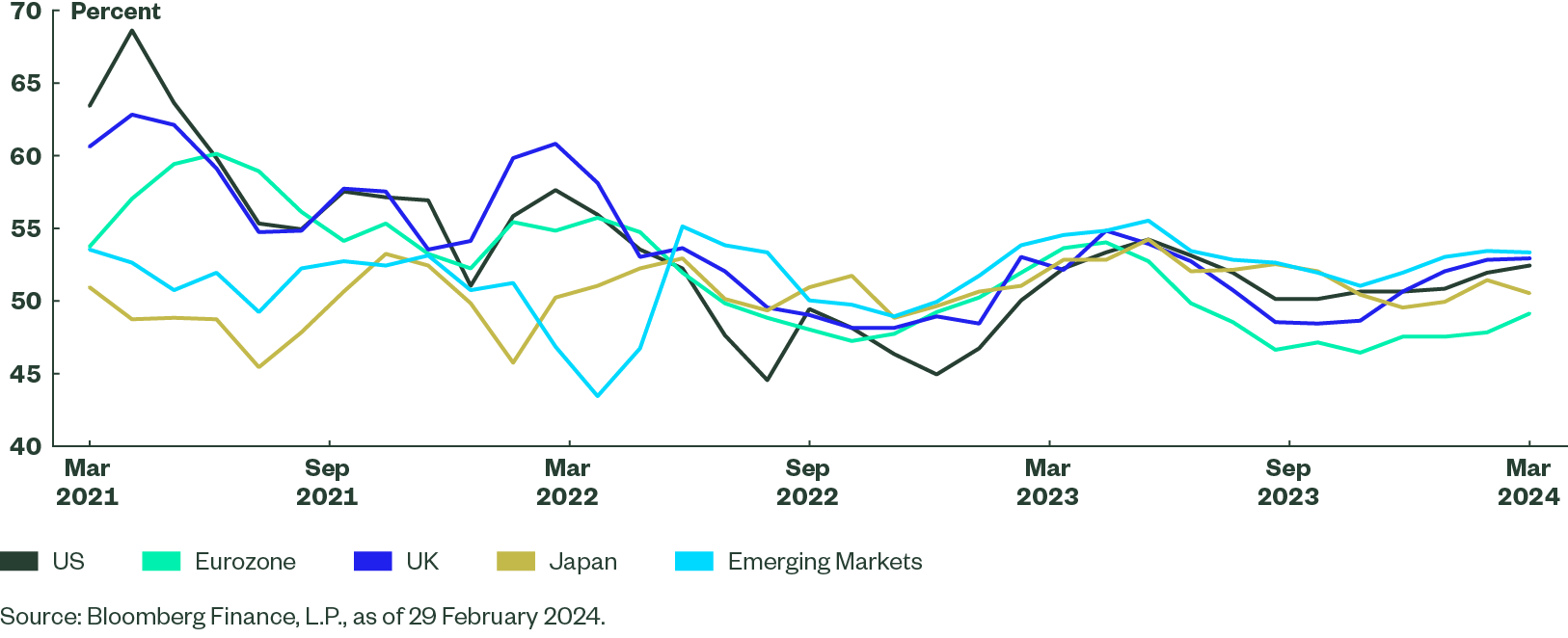

Economic activity has been improving in both the services and manufacturing segments, though the latter is still in contraction in most of the key regions. However, it is another area of US exceptionalism; the Markit manufacturing PMI rose from 47.9 to 50.7 in January. The ISM PMI figure remained below 50 but showed signs of recovery.

Another important highlight is the UK. Data show it is struggling with a technical recession, but had a very strong composite PMI print of 53.3 in February. Meanwhile, the Eurozone remains in a contraction — though the February composite reading rose 1 point to 48.9 ahead of expectations and at an eight-month high. A relatively weak economic outlook in Europe provides a cleaner path for the European Central Bank and the Bank of England to cut interest rates.

Figure 3: Composite Markit PMIs

Will Disinflation Prevail?

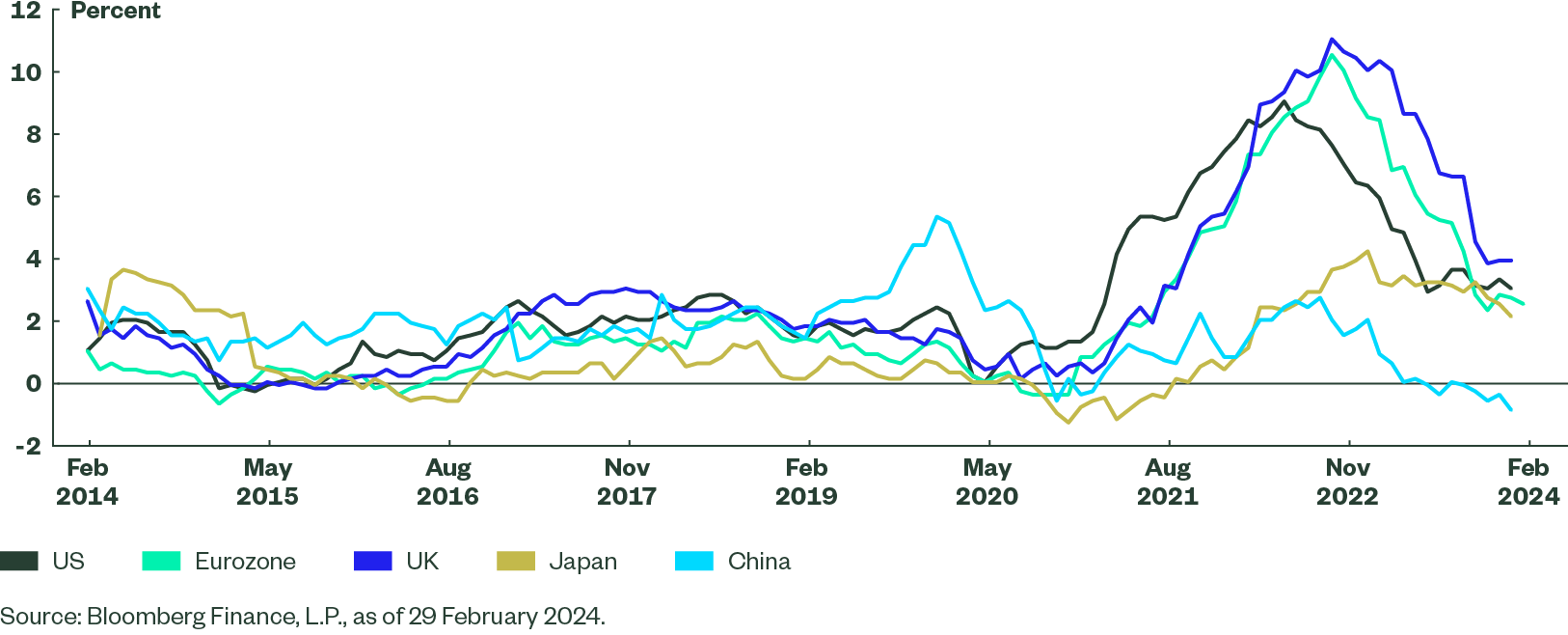

While the global economy is in better-than-expected shape, continued disinflation is being called into question, particularly in the US, as the January CPI print came in at 3.9%, above the expected 3.7%. While we acknowledge the risk of a demand-driven rebound in prices (especially after such a print), we still expect disinflation to continue, given restrictive rates are working through the US economy. Europe is likely to see a smoother path towards inflation targets given weakness in demand, although bottlenecks in the Red Sea are adding to supply-side price pressures. China remains on the edge of deflation, struggling to revive domestic demand. Japan, on the other hand, may see a degree of policy normalization. January consumer prices (excluding fresh food) rose 2.0%. That’s above the 1.8% forecast but still in line with the Bank of Japan’s target. The probability of rate hikes will increase if Shunto negotiations deliver robust wage growth.

Figure 4: CPI Inflation

Strength of Labour Markets Remains Intact

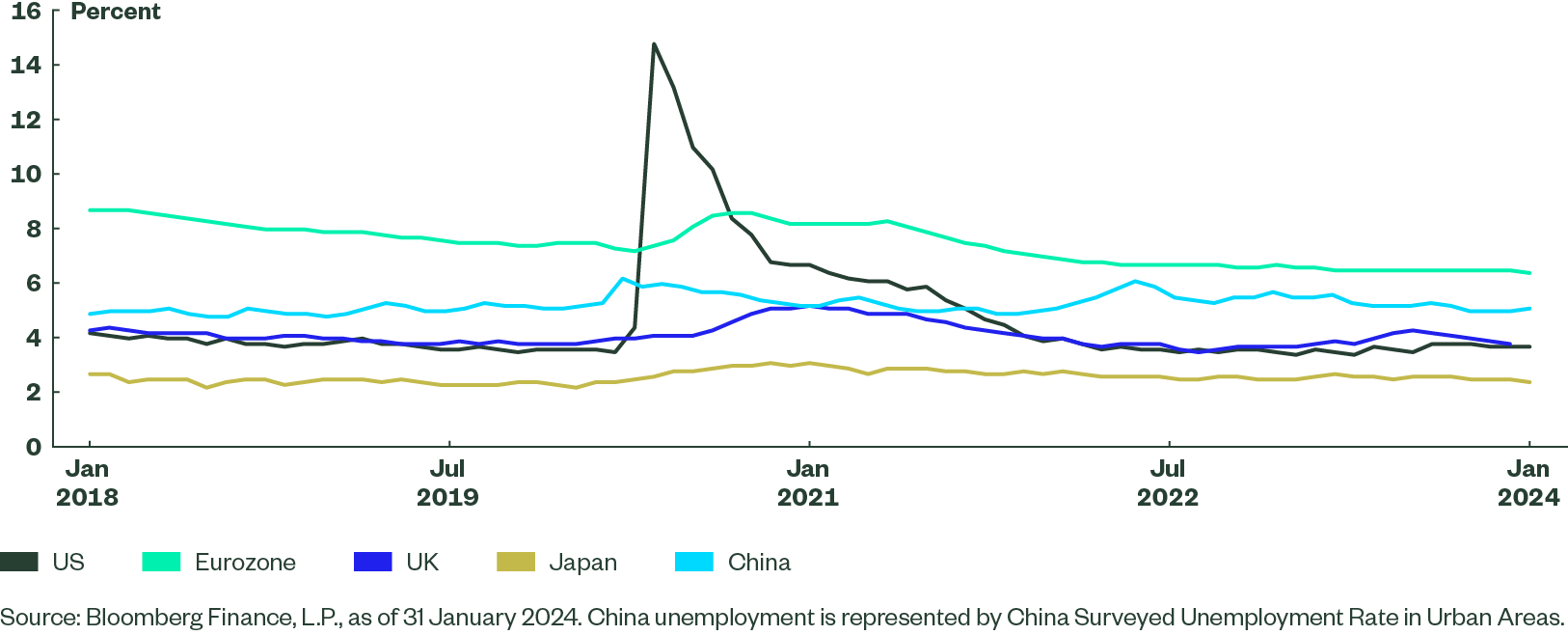

The battle against inflation is being won and dovish pivots from central banks are on the horizon. But what is most remarkable is that, at the same time, labour markets remain robust across major economies. US unemployment sits at 3.9%, one of the lowest levels since 1969. Japan and China are also experiencing tight labour markets with unemployment at 2.4% and 5.1%, respectively. Eurozone and UK numbers at 6.4% and 3.8%, respectively, are also lower than one might have expected after the hawkish turn of central banks. Tight labour markets drive consumer resiliency, which allows the global economy to go through a period of higher rates without widespread crises.

Figure 5: Unemployment Rates

Valuations Re-rated — but Rate Cuts on the Horizon

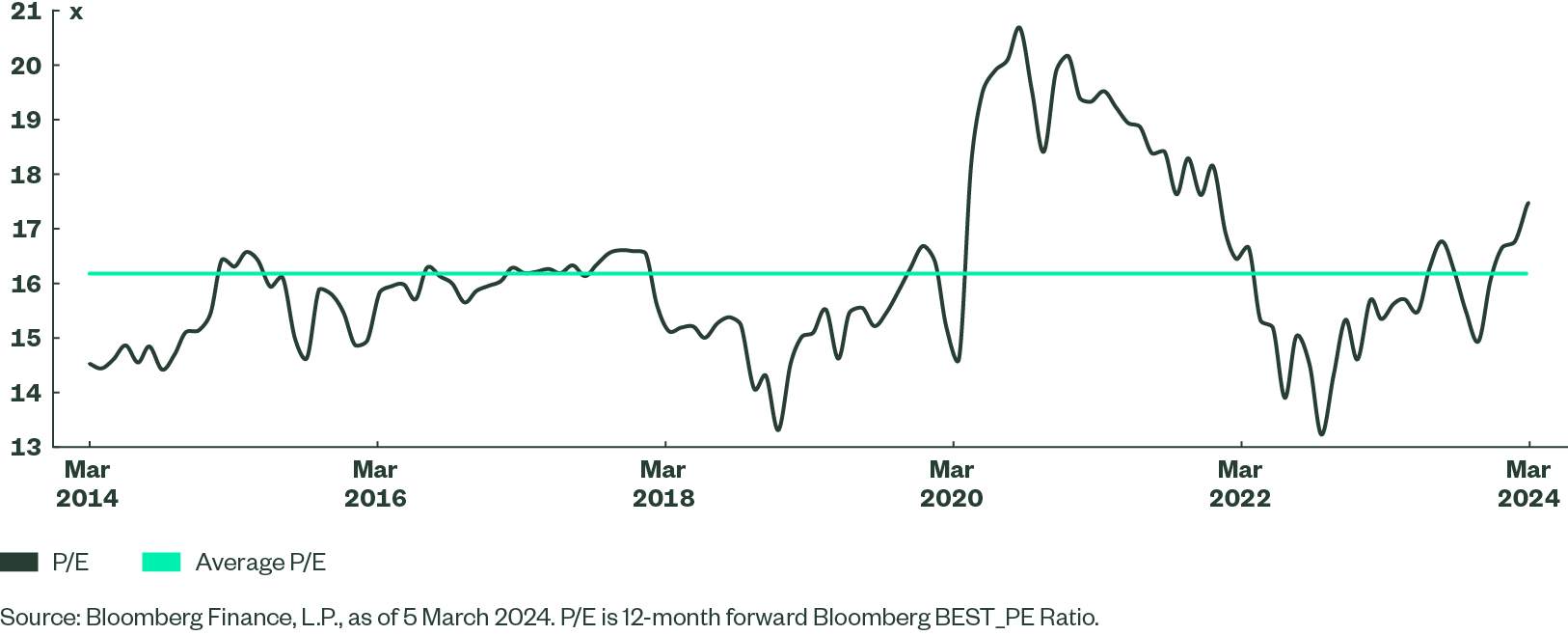

Equity markets have been on a four-month rally since the end of October. That has led to re-rating equities to a 17.5x price-to-earnings (P/E) ratio, which may be justified as long as the soft landing scenario continues to unfold. Current P/E translates to a 5.7% earnings yield which, at first glance, may not seem appealing to asset allocators, given a 3.7% yield on a seemingly safer global aggregate bond index exposure.3 However, in the current environment, bonds offer protection against a hard landing scenario. Over the past year, both growth and inflation surprised to the upside, making the “no landing” outcome perhaps a more probable one. Under such a scenario, bonds will likely offer little protection against higher inflation; equities may benefit from economic growth and to some extent from inflation, at least in nominal terms.

Figure 6: MSCI ACWI IMI Index 12-month Forward Price to Earnings

Earnings Are Taking Centre Stage

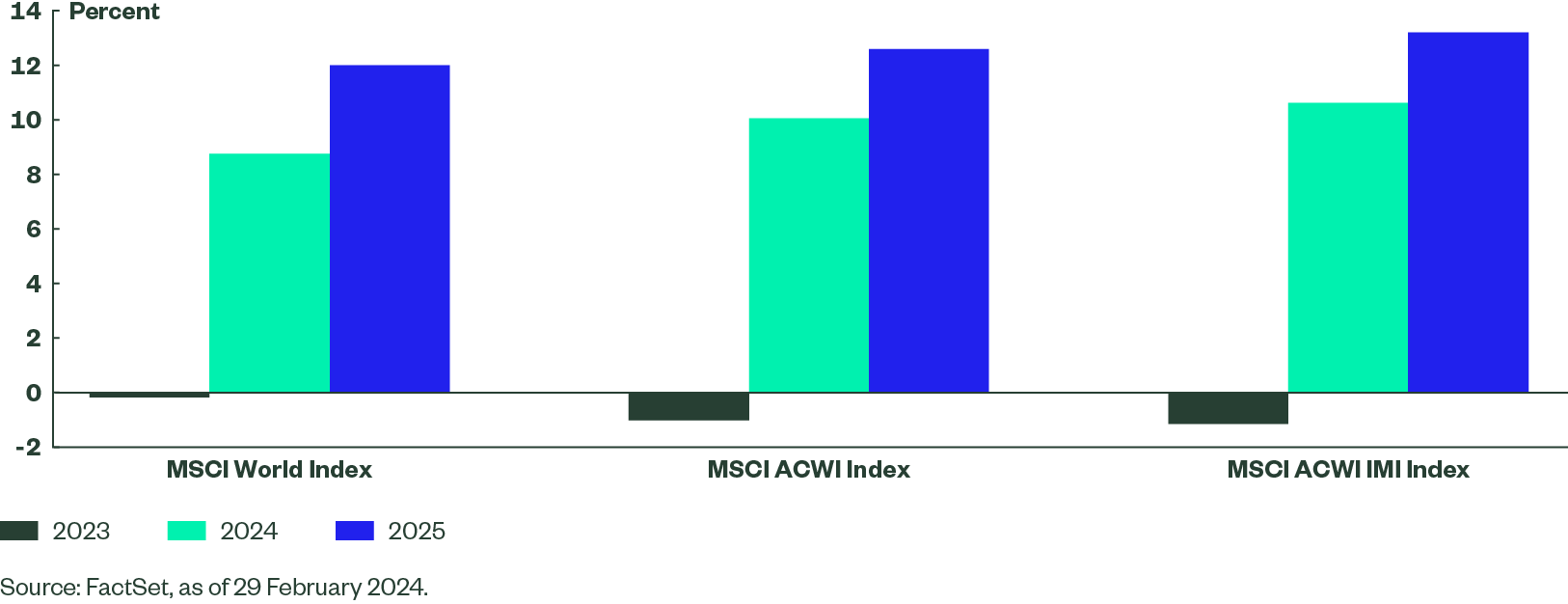

In the beginning of 2024, investors shifted their focus from yields to earnings as better-than-expected Q4 results demonstrated the ability of businesses to cope with higher rates, at least for the time being. US and Japanese Q4 earnings came in 7% and 12% above expectations, respectively, while European earnings in aggregate were 3% ahead of estimates.4 The currently priced-in earnings growth in 2024 may be not just achieved but exceeded, especially if economic growth projections continue to be revised upwards while central banks begin cutting rates.

Figure 7: Earnings Growth Estimates

Going Global to Capture Equity Potential

With the battle against inflation largely won, rate cuts on the horizon, and both GDP growth and earnings surprising to the upside, it appears that the equity rally has further room to run. Key risks remain, including an inflation rebound and further deterioration in the geopolitical landscape.

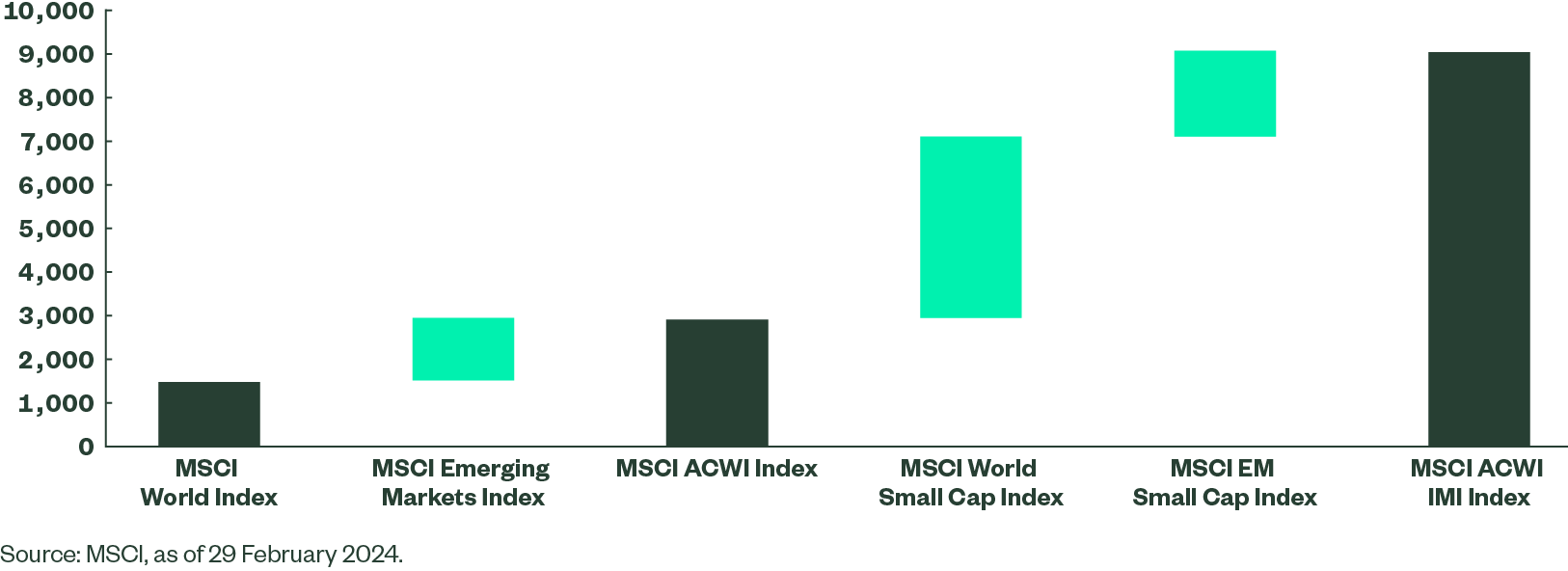

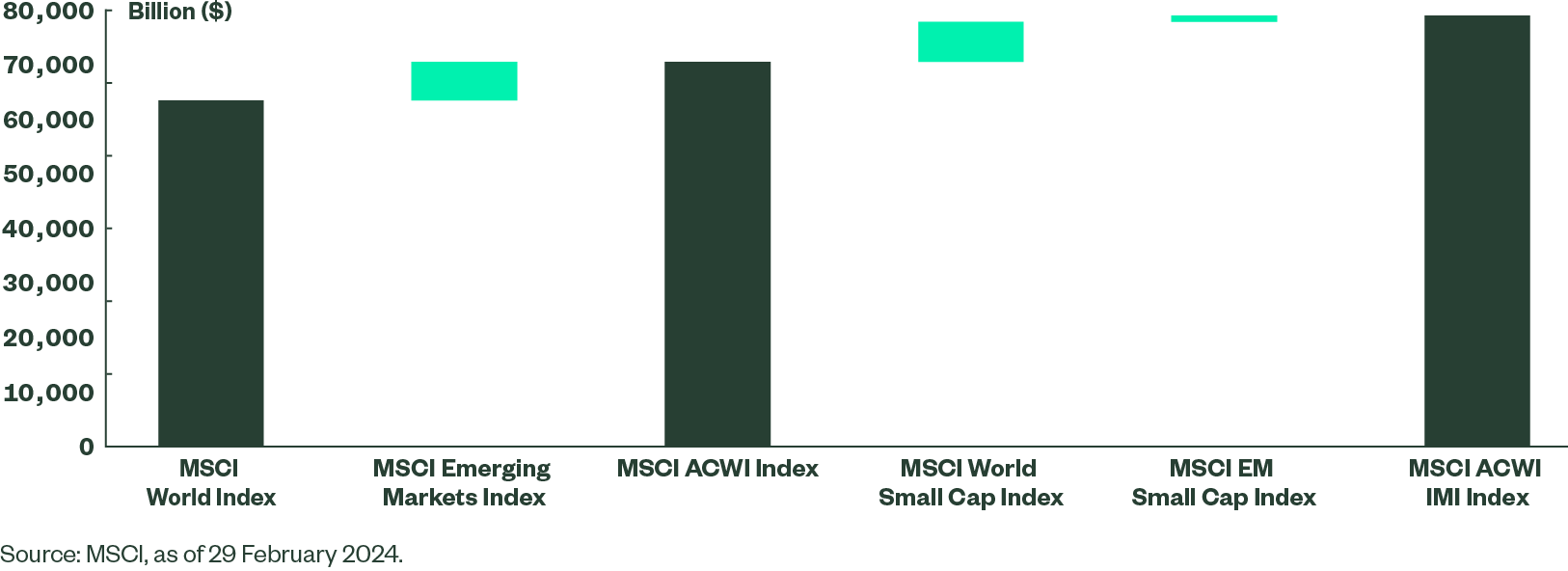

Investors may choose their preferred regions or decide to allocate to a diversified exposure such as the MSCI World Index, the MSCI ACWI Index or the most comprehensive MSCI ACWI IMI Index. Euro- and GBP-based investors may also consider hedging their exposures against the risk of the US dollar depreciating relative to their own currencies, which could be triggered by a potential dovish turn from the Federal Reserve later in 2024.

Figure 8: Global Equity Indices by Market Cap

Figure 9: Global Equity Indices by Number of Constituents