US Snapshot

This report highlights four United States-specific insights into how workers are thinking about retirement; what planning tools they consider most important; and how plan sponsors can be most supportive in helping them realize their long-term financial goals. The collective voice of workers expressed in the results can provide employers, financial advisors and policymakers with a wealth of information about how to best help plan participants succeed.

Attitudes about retirement change every year — and sometimes evolve in unexpected ways. That’s been shown time and again in the findings from our Global Retirement Reality Report (GR3), conducted annually since 2018. The report provides a window into how individuals and organizations are preparing for retirement and what resources they need to succeed.

In 2023, the turmoil caused by COVID-19 and continued economic uncertainty eased somewhat, allowing workers to focus more of their attention on their retirement prospects and the steps they can take to reach their retirement goals. Now, they’re looking for support to bolster their confidence that retirement is within reach and desire the ability to generate a steady stream of income after they step away from the workplace.

Key finding 1: Retirement planning is again a priority.

For many American workers, the past three years have been a blur of crises affecting their daily lives. The COVID-19 pandemic forced changes in the way people work and interact with friends. Product shortages made it hard to find basic items. Gas prices soared when Russia invaded Ukraine. Rising inflation caused spikes in everyday goods such as groceries.

But in 2023, as the pandemic receded and inflation slowed, Americans began to refocus on long-term goals such as retirement. More than half of American respondents (54%) said they expect to fully retire at some point in their lives and another 28% said they expect to partially retire. The number of respondents saying they are on track for retirement remained largely unchanged between 2022 and 2023, suggesting that individuals are moving beyond the worries and uncertainties driven by the pandemic and fear of an economic recession.

In this year’s survey, American respondents were the most confident about their ability to retire on time (30% versus a global survey average of 21%). Confidence among U.S. respondents in their ability to retire in their lifetime also continued increasing, reaching 31% from 24% in 2020. Even so, seven in 10 American workers still are not fully confident that they will be able to retire—or to retire on their chosen timeline.

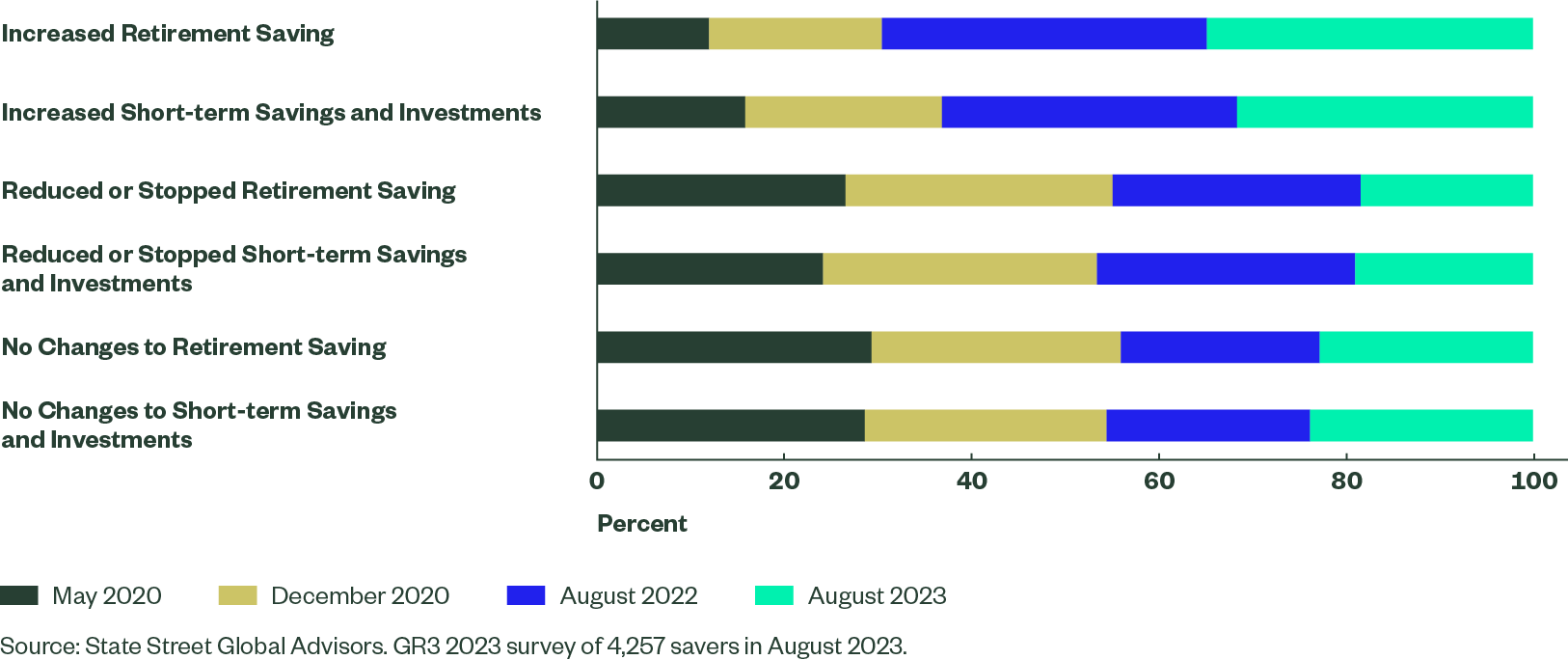

However, efforts to prepare for retirement have been moving in the right direction: Just 9% of Americans have reduced or stopped their retirement savings, compared to 14% who did so in 2022. And nearly a third of U.S. respondents (32%) have increased their savings rates in that same timeframe.

Figure 1: Changes to Savings Behavior in Past Six Months

Respondents continue to have significant worries about their preparedness for retirement, expressing both short-term concerns such as price increases and political uncertainty as well as longer-term worries such as the cost of health care as they age. Inflation and the related cost of living crisis was by far the biggest barrier to retirement identified by respondents (74%), but other significant worries were seen in the results. Concern about the threat of unplanned expenses, such as medical expenses (47%), grew faster in the United States than in most other countries, and the political environment (40%) also weighed heavily

Plan sponsors can help mitigate workers’ short- and long-term concerns through educational outreach and plan design. Workers would value information about how they can manage health care costs today so that they can save more money for retirement. Similarly, sponsors can address worries about inflation by putting recent price increases into a historical context and evaluating inflation-hedging options for their DC plan — whether they are within a target date fund’s glidepath, imbedded within another solution such as a balanced fund, or offered as a standalone option such as real assets including commodities, precious metals or real estate. If already offered within the DC plan, sponsors should make sure plan participants know these solutions exist and educate them on how they are designed to combat inflation.

Key finding 2: American women are struggling more with retirement than men.

All workers have to balance the need to meet today’s financial obligations with setting money aside for the future. Women, though, typically face greater hurdles in preparing for retirement: generally lower earnings, greater life expectancy, and a higher likelihood of having their careers and retirement savings potential disrupted by family care.

As a result, it’s not surprising that women were less optimistic than men about their ability to retire. Fewer than a quarter of women (23%) were extremely or very optimistic about being financially prepared for retirement compared to nearly four in 10 men (39%). Women were even more concerned about inflation than men, with three in four (75%) concerned that price increases will erode their spending power over time.

Figure 2: How optimistic are you that you will be financially prepared for retirement by the time you stop working?

Employers can play an important role in helping women prepare for retirement. Consider that 27% of women reported increasing their savings in 2023 compared to 33% of men. Targeted engagement programs for women about the financial benefits of increasing savings can make a difference. Through outreach, education and in-person forums, employers can help women to build confidence in their ability to save for retirement. Women-led and women-only educational sessions, in particular, may provide safe and supportive environments that can help some individuals feel more comfortable asking questions, discussing finances, and therefore gaining valuable insights.

“While there are systemic issues at play that the defined contribution industry alone can’t solve, we can help,” says Danielle Gladstone, Head of Participant Engagement at State Street Global Advisors. “Education can and should center around asset allocation. Historically, women are more conservative investors, but options like target date funds have leveled the playing field.”

Helping women workers goes beyond retirement education and plan design. In particular, workplace accommodations such as flexible work schedules can help women avoid career interruptions caused by childbirth and caregiving, thus allowing for better opportunity to save for retirement continually throughout their working years.

Key finding 3: Americans take responsibility for their retirement, but are looking for support.

Workers in the United States aren’t expecting other people to take care of their retirement for them. U.S. respondents were the most likely of any country surveyed to say they are personally responsible for retirement (73%), compared to Canada (61%), Australia (64%), UK (66%) and Ireland (71%). American workers also are acting on that belief: They were more likely to be checking their retirement-savings balances regularly (39%) than in the past, an increase of 4 percentage points compared to 2022.

While U.S. respondents were among the most confident of any country surveyed in their ability to figure out how best to sustainably withdraw their savings independently (37%), nearly two thirds of American workers (63%) want help from trusted sources with retirement planning.

Figure 3: How helpful would each of these resources be in helping you manage your finances in retirement?

Nearly eight in 10 respondents (78%) agreed that education and advice are helpful retirement resources. Employers can support workers by offering personalized planning tools and access to advice. Workers say that financial consulting and web-based modeling tools would be beneficial resources as they prepare for retirement. Three quarters of respondents (76%) said one-on-one financial advice would be helpful. More than seven in 10 (72%) said online income calculators that help them spend down their retirement savings over the course of a lifetime would be helpful.

Two thirds of respondents (66%) said they want an employer service that helps with their total financial planning for reaching goals such as housing, paying for education and retirement. Employers and financial service providers can support retirement preparedness by understanding that plan participants’ finances are interconnected. Providing a service such as tuition reimbursement means that an employee does not have to choose between paying for their education or setting money aside for retirement.

Figure 4: To what extent would you want to be offered more information about the following services from your employer?

Key finding 4: Americans prioritize dependable lifetime income in retirement.

For most of their adult lives, workers earn a regular paycheck to help them pay the bills each month. So, it’s no surprise that respondents were most likely (47%) to define retirement income as a consistent income stream, like a paycheck, that begins the day they retire. Six in 10 Americans (60%) preferred receiving income in retirement as a steady stream of income rather than all at once.

The importance of regular income is even stronger for the latter years of retirement. In the U.S. and across the globe, people said they want flexibility with their money early in retirement and stability later. Americans were most likely to say they want flexibility at beginning and steady income later in life (42%), compared to set amount for life (31%), or flexible access even if they run out (27%).

Americans’ desire for certainty around their retirement income picture is growing. The resource mentioned most frequently as being helpful is an employer-offered product that provides guaranteed income. Nearly eight in 10 respondents (79%) agreed that an employer-sponsored annuity solution would be a helpful resource. Four in 10 (40%) agreed that annuities are an essential part of providing an income in retirement.

Figure 5: To what extent would you agree or disagree with the following statements about annuities?

When a plan sponsor offers an annuity-based solution, participants should be given not only robust education on how the annuity works, but also the ability to quantify the benefits of the annuity. There are plenty of “retirement-income calculators” online, but the results may not be grounded in the participant’s real financial picture. Instead, an intuitive digital experience that leverages the participant’s actual account balance and real-time annuity pricing could provide more meaningful information, allowing the participant to make an informed decision about whether to purchase that annuity.

Closing Thoughts

- Workers are refocusing on retirement preparedness. While Americans’ confidence in retirement increased modestly, a strong majority of workers still are not sure they will be able to retire when and how they would like to. With pandemic-related concerns receding and an uptick in savings-related goals, now is the time to help workers think carefully about how to build their nest eggs.

- Women need additional resources to accomplish their retirement goals. American women reported far lower confidence that they will be able to retire than male respondents, with less than a quarter of women being strongly assured of it. Targeted education programs and workplace accommodations can help support women’s concerns that inflation, disruptions in career earnings and other challenges will keep them from achieving their long-term financial goals.

- Workers are anxious for support around retirement. More than three quarters of Americans said they would value advice and education such as web-based tools, income calculators and programs that help them look holistically at their financial obligations so they can make appropriate choices about retirement and put more money away. To truly address retirement planning, these tools should be personalized to the individual participant, not built off a persona.

- Having a regular source of income in retirement is a primary goal for most Americans. Most people want to have a steady stream of funds coming in as soon as they retire. Workers would benefit from education, tools and plan-design features to help them prepare now to have regular income in the years ahead.