The Defensive Qualities of High Yield

High real yields and short durations make high yield bonds an interesting asset class. Credit spreads may have tightened, but historically high outright yields provide some protection in the event that slower growth pushes spreads wider.

The decline in US Consumer Price Index (CPI) seen over the past 12 months is rightly viewed as a key driver of Federal Reserve policy. But it also has material implications for investor returns. For instance, in June 2023, US CPI topped 9% on a year-on-year basis, which meant negative returns on an inflation-adjusted basis — even for strategies like high yield.1 While yields have declined from the highs seen in Q3 2023, they have fallen at a more moderate pace than inflation, resulting in real yields of 450 basis points (bps) given the current CPI level. European yields and CPI are also lower, and the result is that the real yield is a little higher than for the US. These real rates of return are high from a historical perspective, and have supported interest in high yield bonds.

Structural changes in the market have added to the resilience of high yield as a strategy. The key change is the shortening of average durations. This has been driven by a combination of two things: a lack of new issuance (it is expensive to issue debt with yields where they are), and sharp price declines seen in high yield bonds in 2022 resulted in a lowering of bond durations. In the case of the Bloomberg US High Yield Index, the option-adjusted duration has dropped from highs of over 4.25 years in 2022 to close to 3.1, while the Liquidity Screened Euro High Yield Index has fallen to 2.65 years, its lowest since the index was incepted in 2004.2

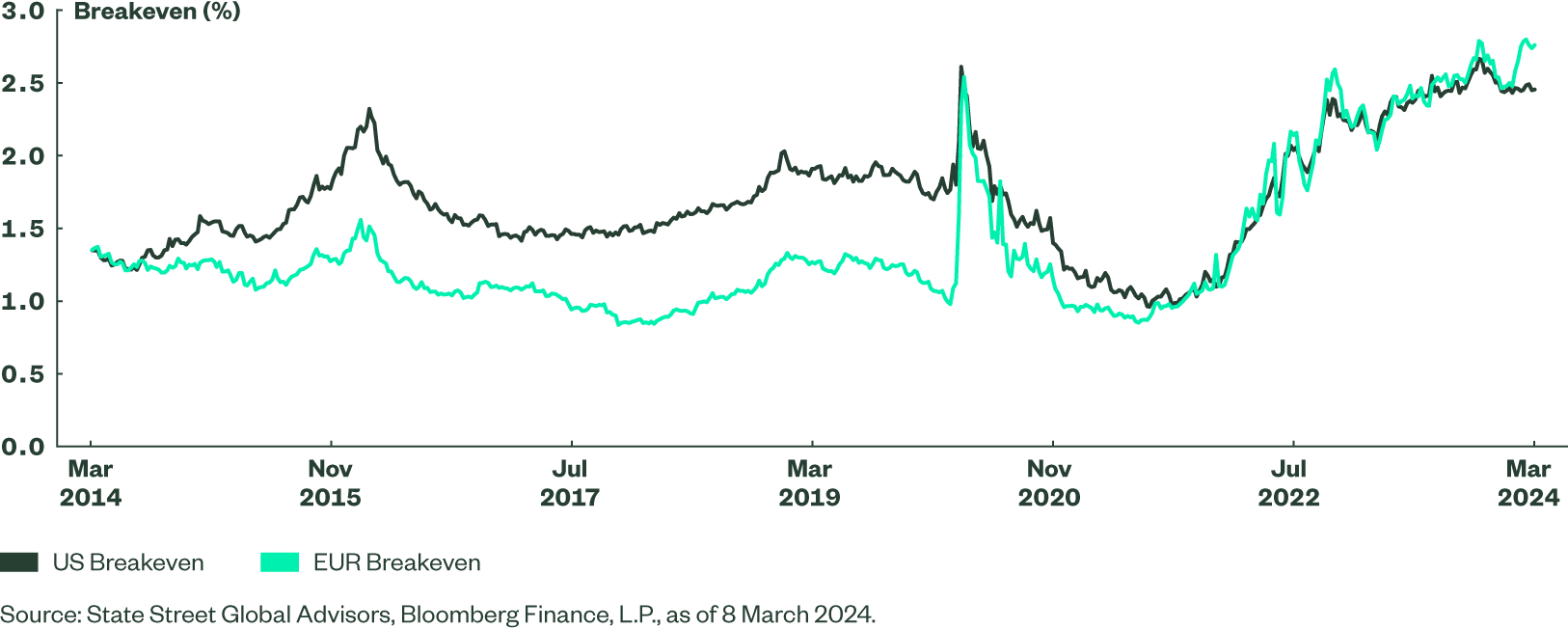

Lower price sensitivity to moves in market yields is a key variable in determining the probability that an investment will break even. A proxy for this can be derived by dividing the index yield by its duration. This gives an indication of the degree to which the yield on the index needs to rise before the price losses of the strategy offset the annual yields received from holding it. In the case of the Bloomberg US High Yield Index, the breakeven is 245 bps, and 276 bps for Euro. Both are at historically high levels (Figure 1).

Figure 1: Breakeven Yields for US and Euro High Yield Indices

Tight Spreads and Other Risks

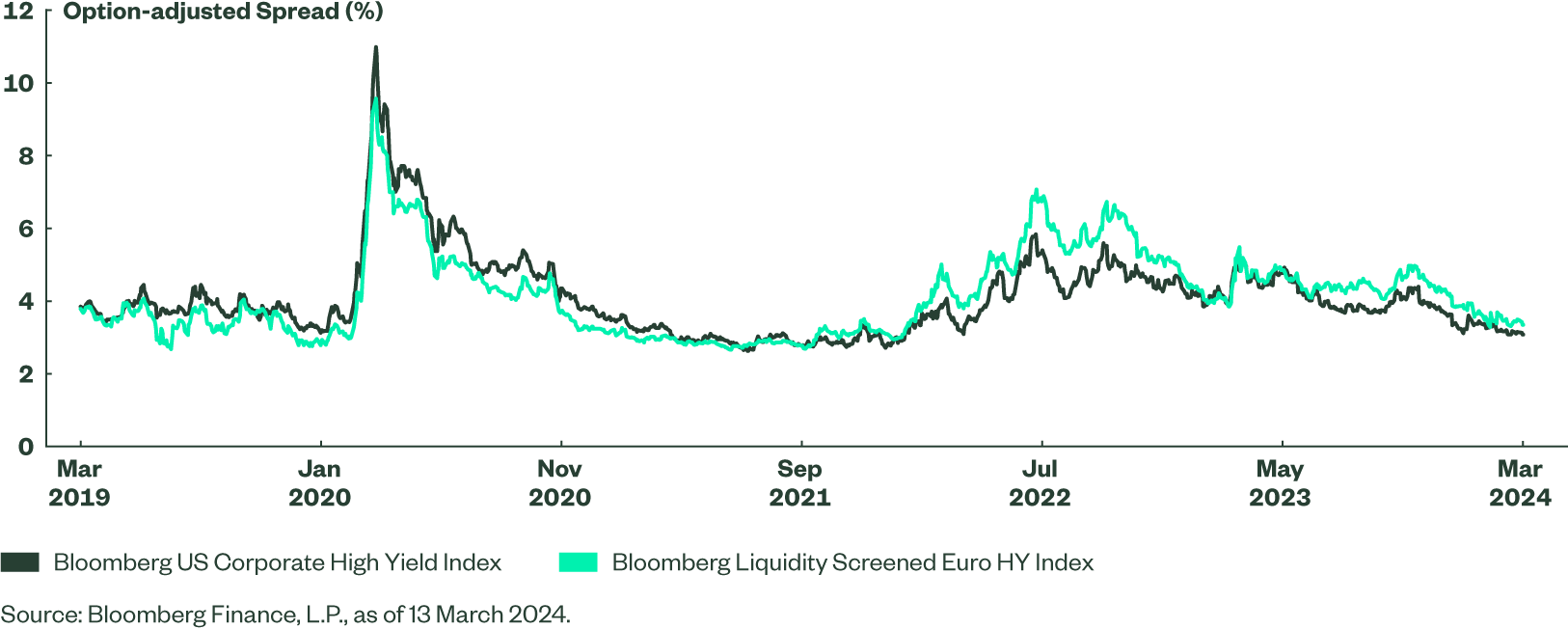

While outright yields and high breakevens may provide a draw for investors, there is no doubt that credit spreads are tight. Option-adjusted spreads are as tight as they have been since early 2022, implying that there is already plenty of ‘good news’ in the price. A soft landing seems to be the consensus view of markets, meaning spreads would be liable to widen in the event of a more material slowdown. This is a risk, but as elaborated above, yields would have to rise by around 250 bps before investors suffer negative returns. This is not impossible, but the recent trend has been more about upside data surprises. Even in Europe, where growth has been far slower, the recent trend has been for some upside surprises with the Citi Economic Surprise Index over 50.3

Figure 2: High Yield Spreads Have Tightened

The upgrades-to-downgrades ratios for both Europe and the US have fallen below 1, indicating that momentum has shifted towards a deterioration of corporate balance sheets. High interest rates are partially to blame, but a more material slowdown would at least force central banks to ease policy. So credit spreads may widen but all-in funding costs could potentially still ease.

The alternative scenario is that activity data remains strong and CPI sticky. This is what the market has been faced with year to date and, while not constructive for rates markets generally, has resulted in high yield delivering a stronger performance than most other parts of the fixed income market.