Ireland Snapshot

As Ireland prepares for the introduction of auto-enrolment in 2024, the implementation of the reforms seems perfectly timed. Irish savers’ optimism and confidence about retirement has been dealt a blow by the rising cost of living, which has raised concerns about how people can afford to stop working in later life.

Despite this short-term headwind, it is still important to proceed with the structural reform that will improve retirement saving in the longer term. By phasing in contributions over time, the increased level of saving will be easier for people to adjust to.

Discussions about mandatory retirement ages and phased or delayed retirement are ongoing, but rising living costs and other factors are making it more likely that some people will choose to – or have to – keep working beyond the existing state pension age.

Key Findings

Our global survey involved more than 4,200 respondents, over 600 of whom were from Ireland. We asked respondents about their retirement plans and expectations, their income needs, their sustainability attitudes and their views on services related to pension savings.

While the cost-of-living crisis dominated the results, the survey also provided important insights into how people view their income needs in retirement and what support they would like from employers and pension providers. As Ireland moves to implement auto-enrolment, these other issues should move to the foreground for consideration by all stakeholders.

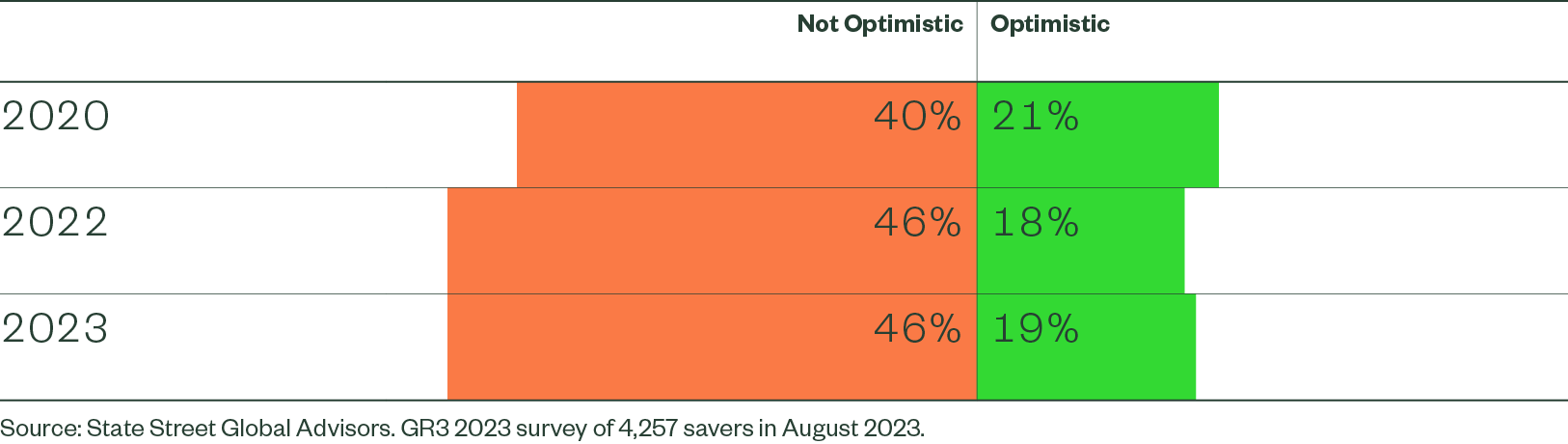

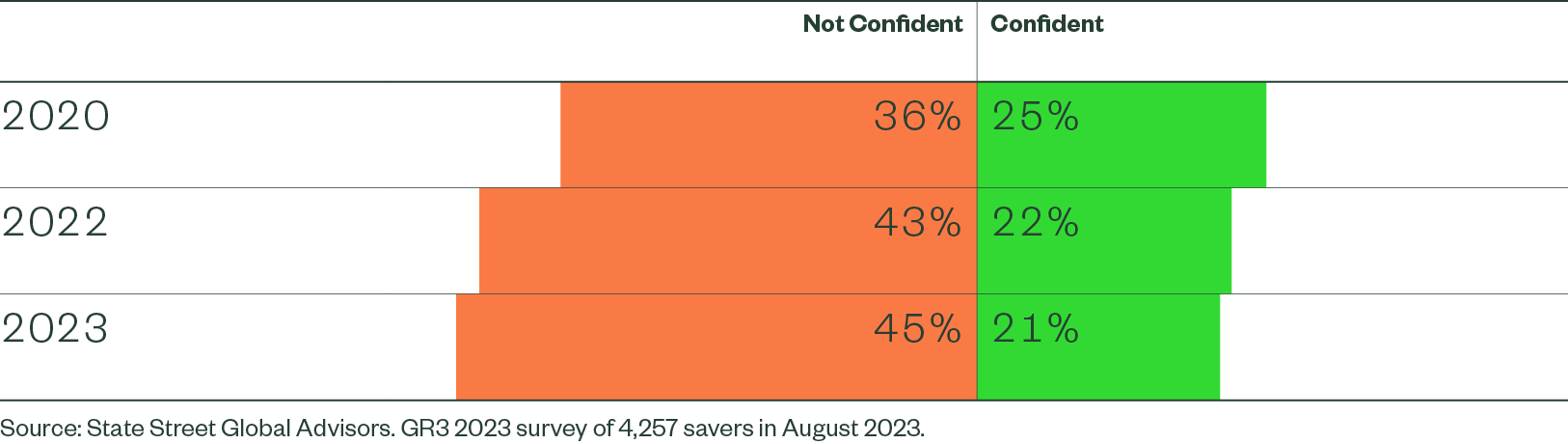

Key finding 1: Cost of living impacts retirement optimism…

Almost half (46%) of Irish pension savers said they were “not at all” or only “slightly” optimistic about whether they will be financially prepared for retirement by the time they expect to stop working. A similar proportion (45%) are “not at all” or only “slightly” confident of being able to retire when they plan to.

Figure 1: How optimistic are you that you will be financially prepared for retirement by the time you plan to stop working?

Figure 2: How confident are you that you will be able to retire when you plan to?

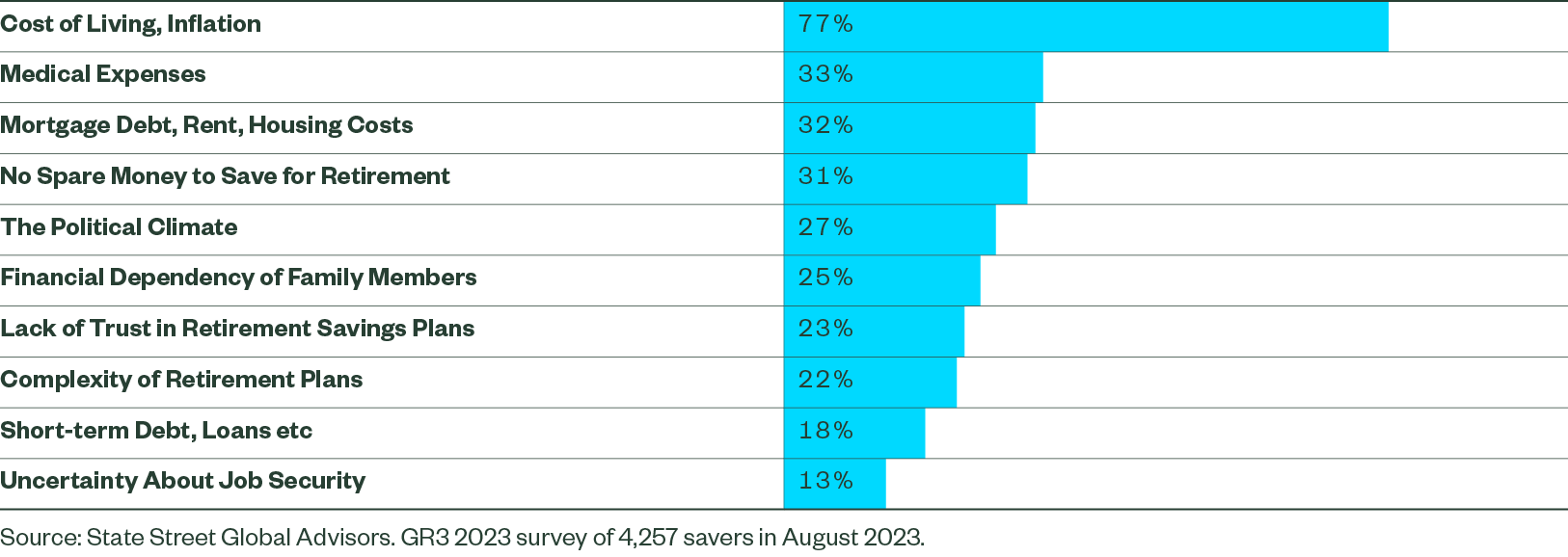

The biggest barrier to retirement by far is the current high level of inflation, which has fuelled a cost-of-living crisis in every country covered by our research. More than three-quarters (77%) of respondents cited this as their biggest concern. However, inflation has been falling in recent months in Ireland and is now significantly lower than it was in late 2022. If this trend continues and inflation remains at a more manageable level, confidence and optimism around retirement may increase.

However, policymakers cannot rely on this, as savers have other concerns. A third (33%) cite medical expenses as a barrier to retirement, while a similar proportion (32%) are concerned about meeting housing costs such as rent or mortgage payments.

Three in 10 (31%) say they have no spare money to save for retirement. As auto-enrolment is implemented and contribution rates rise over the next decade towards 12% (split equally between employer and employee), we would expect optimism around retirement to improve.

Figure 3: What factors most negatively affect your confidence that you will be ready to retire when you plan to? Please pick top three.

It is also worth noting that more than two in five Irish respondents cited the complexity of retirement plans (22%) and a lack of trust in them (23%). This emphasises the importance of ensuring the auto-enrolment regime is understandable and robust.

“Cost of living and housing market has become increasingly a concern. I have been saving as part of a retirement plan since I was in my 20s and yet I don’t know at this point if I will be able to afford rent, bills, food when I retire.”

“I am more determined and focused about retirement planning. I am learning more about options. I am determined I can retire at 65. Prior to this, I did not think very much about retirement.”

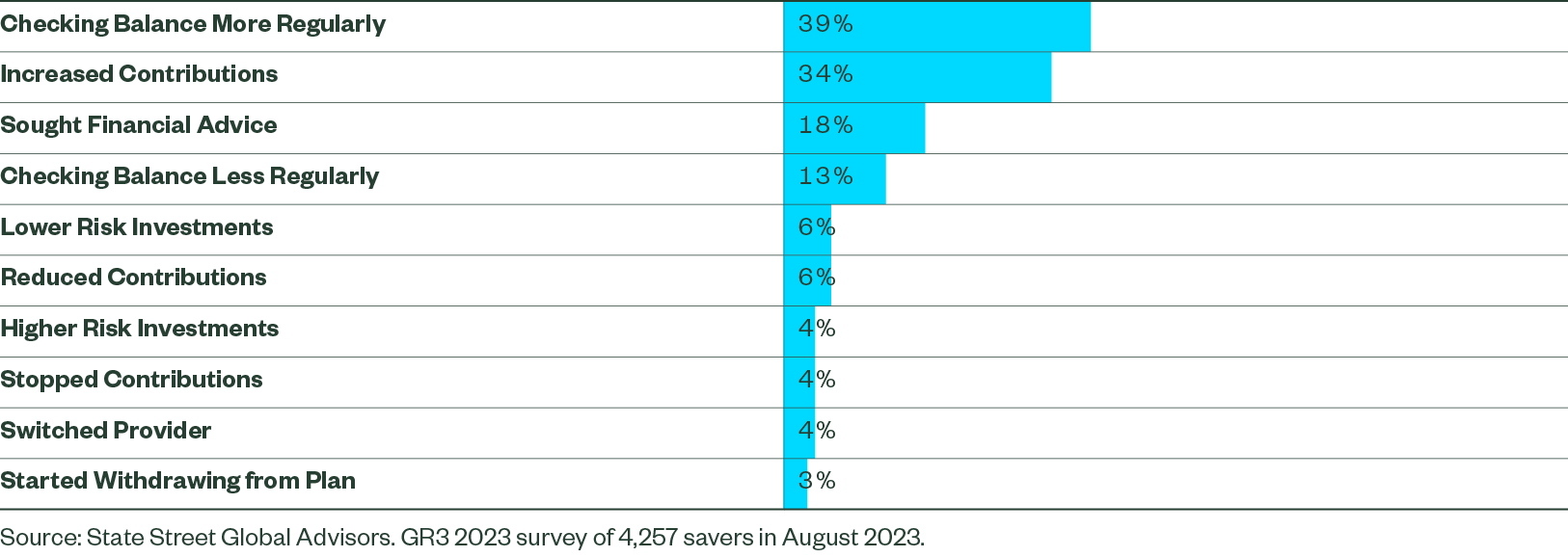

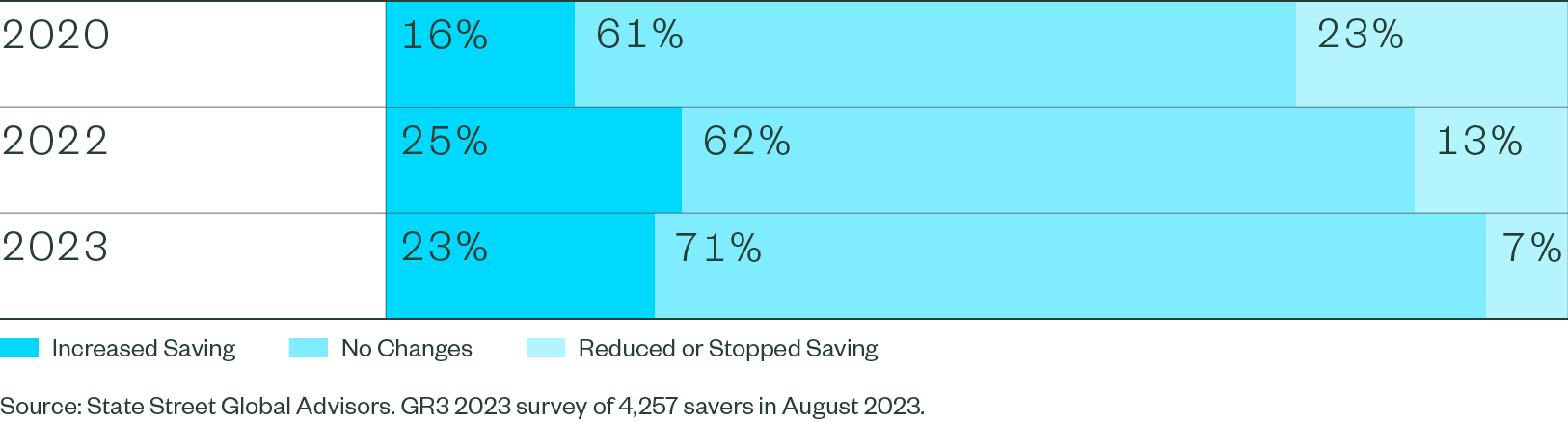

Key finding 2: … but savers are increasing contributions

This lack of optimism and confidence has not stopped Irish savers from contributing more to their retirement pots. More than a third (34%) said they had increased their contributions in the past year.

Figure 4: Have you made any of the following changes to your retirement savings plan? Please select all that apply.

Most people have not made changes to short term savings or retirement savings, but the 10% who have reduced or stopped saving for a pension is cause for concern. There is evidence that automatic enrolment may reduce this: in the UK, the rate at which people actively opted out of their pension was just 0.8% in the 2022-23 financial year.1

Figure 5: During the last six months, have you made any changes to how much you are saving in your retirement savings plan?

Key finding 3: Income in retirement remains a concern

Increasing contributions may reflect an ongoing concern among Irish savers that they will not have enough income in retirement. Most (52%) say they will need €30,000-€50,000 as an annual pension in order to retire, while 29% believe they will need more than €50,000. However, as discussed above, many are sceptical about whether they will achieve this.

Income therefore is an important factor for pension savers, and should inform future discussions of Ireland’s retirement system as auto-enrolment beds in.

Figure 6: How helpful would a source of regular, guaranteed income offered through your employer be?

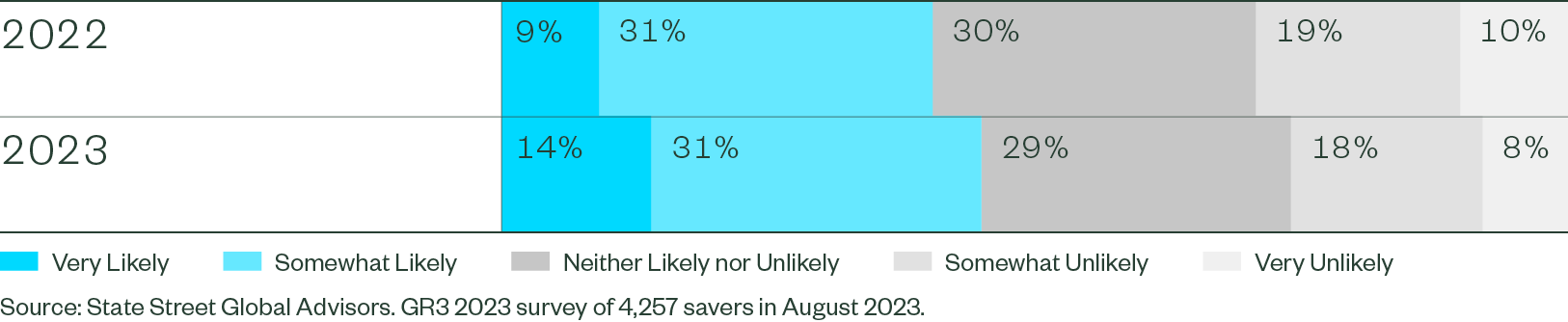

Figure 7: How likely would you be to keep money invested (rather than withdrawing it or transferring it elsewhere) after retirement if it provided an income in retirement?

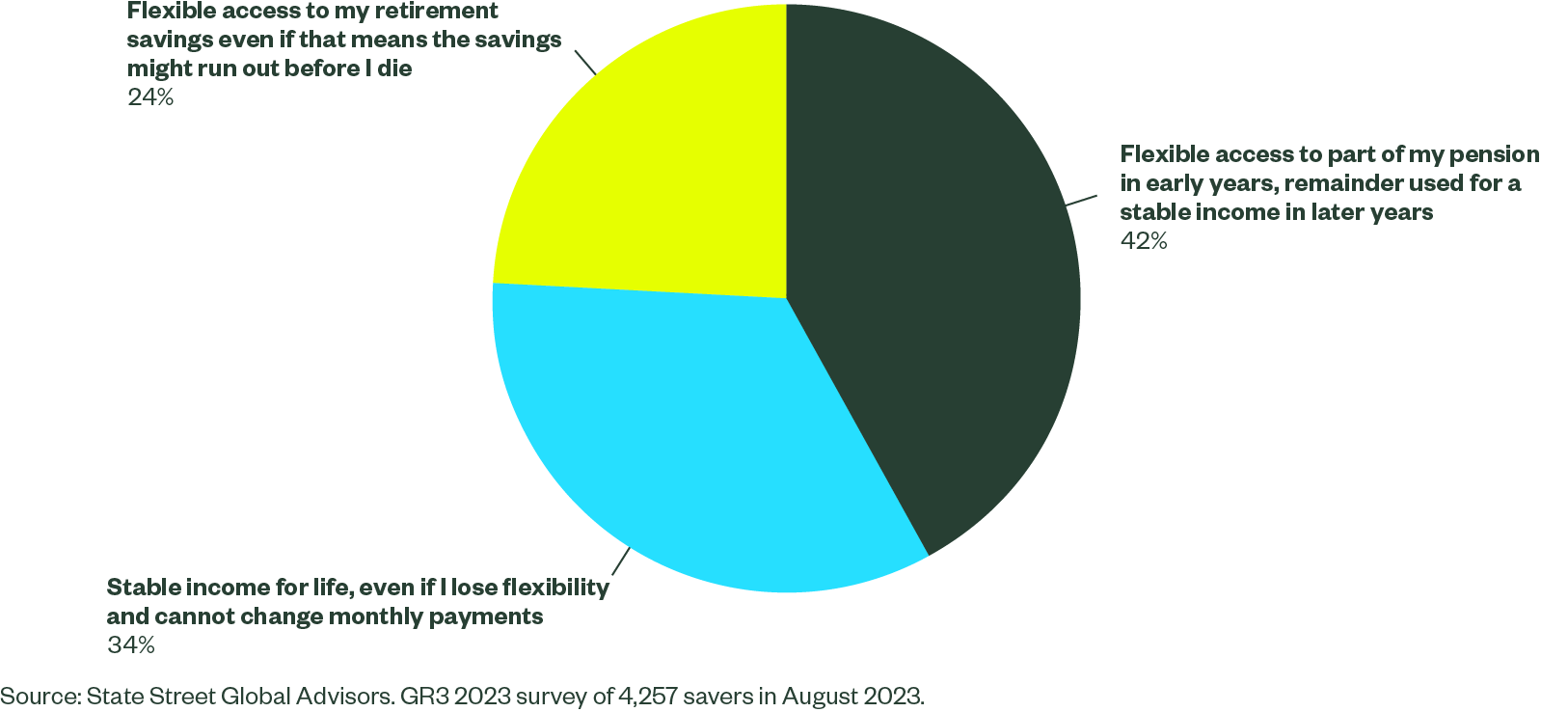

Retirees have several options, including different types of annuities or drawdown via an Approved Retirement Fund. The latter allows for flexible drawdown of income while remaining invested and may be an attractive option for many. A blend of multiple options may also be appropriate.

Figure 8: From the following options below around how you could access your retirement savings, which would you choose?

The success of Ireland’s auto-enrolment regime is likely to be assessed by coverage and opt-out rates, but for individuals it will come down to their experience as savers and in retirement. This means that ensuring they understand their options and are empowered to make appropriate decisions is vital.

Key finding 4: Empowering retirees

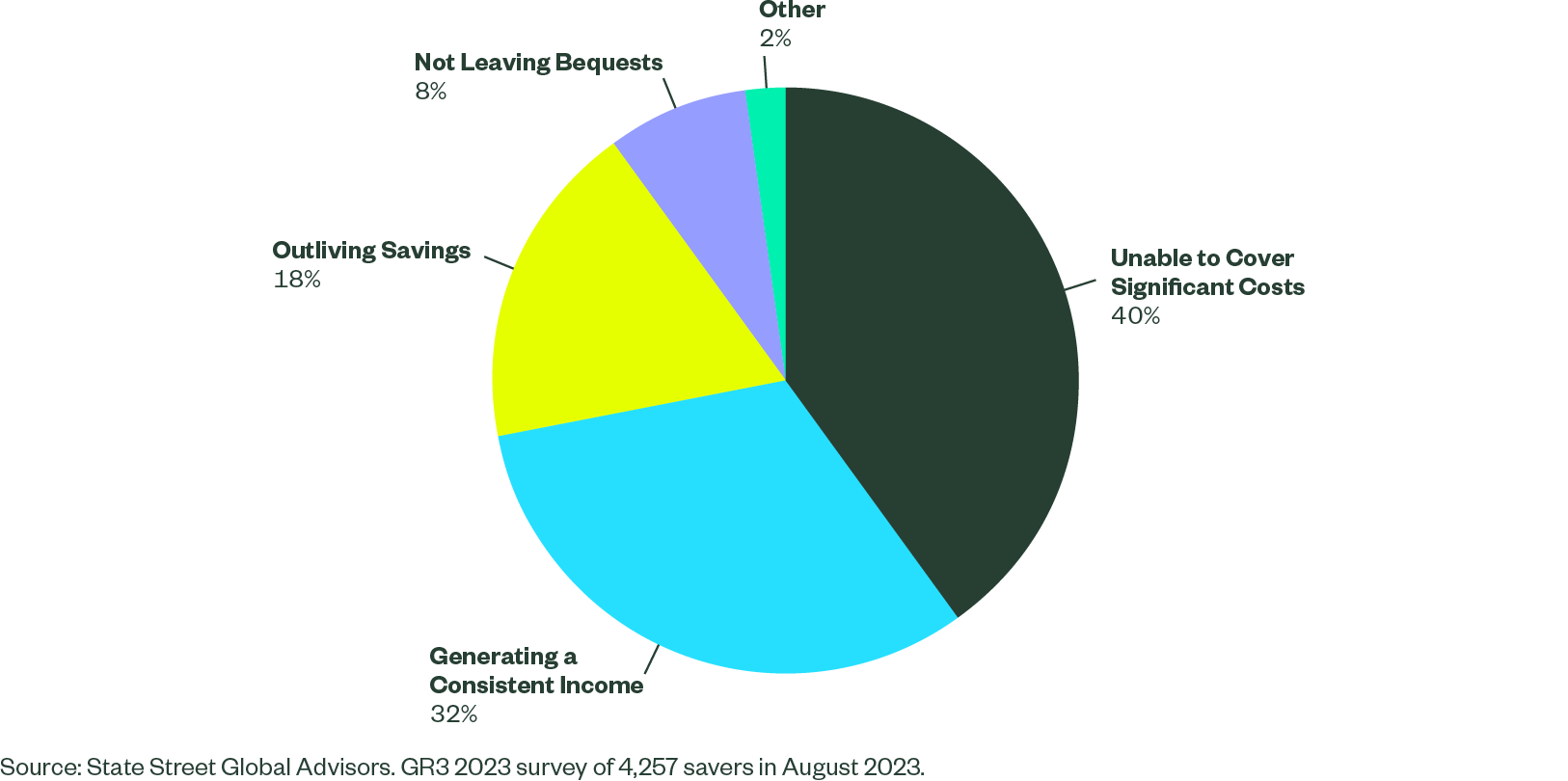

While automatic enrolment is designed to provide a significant boost to retirement savings in the accumulation phase, what happens in retirement remains an issue. Employees want an income in retirement that they can rely on, but achieving this can be difficult for those who are not financially savvy.

Figure 9: What is your biggest financial planning concern specific to retirement?

Choosing what to do with a retirement savings pot is the biggest financial decision many people will make. This makes it particularly important that employers, master trusts and policymakers work together to support decision making and reduce the likelihood of retirees facing problems later in life.

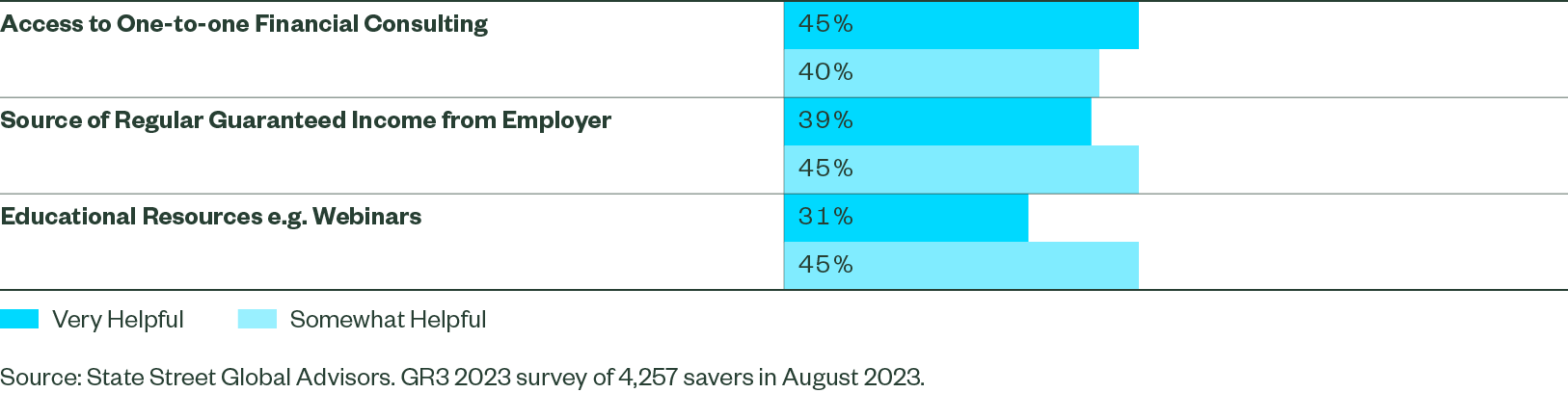

Respondents agreed strongly that services such as one-to-one advice or guidance would be helpful when managing their retirement finances, as would educational offerings such as webinars.

Figure 10: How helpful would each of these resources be in helping you manage your finances in retirement?

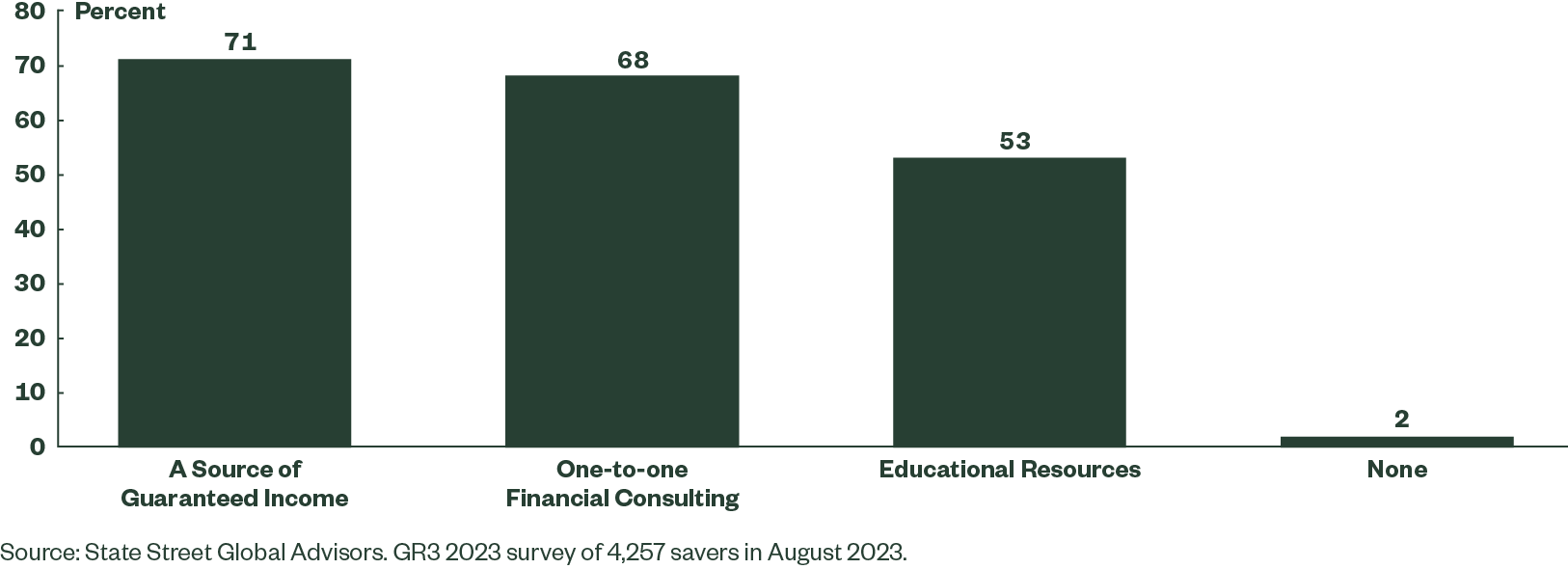

Figure 11: Which of the following resources would you like your employer to offer? Select all that apply.

Auto-enrolment alone is not a panacea for Ireland’s pension savers and retirees. It must come with additional resources and services for individuals and families to help them make these crucial financial decisions and prepare them for the future.

Key finding 5: The importance of phased retirement

Almost a third (31%) of respondents indicated that they would like to or expect to work past their normal retirement age, which is 66 for the state pension in Ireland.

However, this is a contentious issue in Ireland in some areas, as the law is changing around mandatory retirement ages and there are several court cases pending or ongoing related to individuals challenging forced retirement.2

In 2022, Ireland changed its state pension rules allowing people to work up to age 70 in exchange for a higher (deferred) state pension. For some industries and jobs, mandatory retirement ages are in force that preclude individuals from taking this option – some of which are being challenged in court.

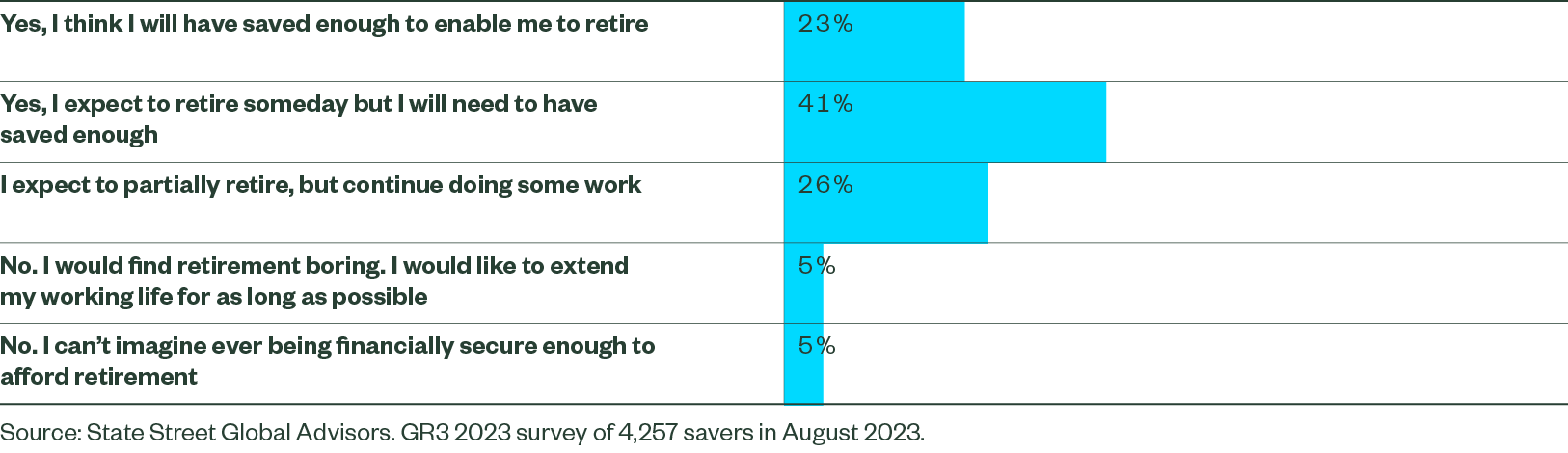

Clarifying the rules and how they apply to different industries and roles will be important to many Irish savers. More than a quarter (26%) of respondents said they expected to only “partially retire”, while another 5% wanted to extend their working life “for as long as possible”. An additional 5% said they did not expect to be able to afford retirement, presenting an additional consideration for policymakers when making decisions on retirement rules.

Figure 12: Do you expect that you will retire?

Allowing phased or gradual retirement may help with the affordability of retirement. It can also help people adjust to the change in lifestyle, while also helping employers transition roles more smoothly.

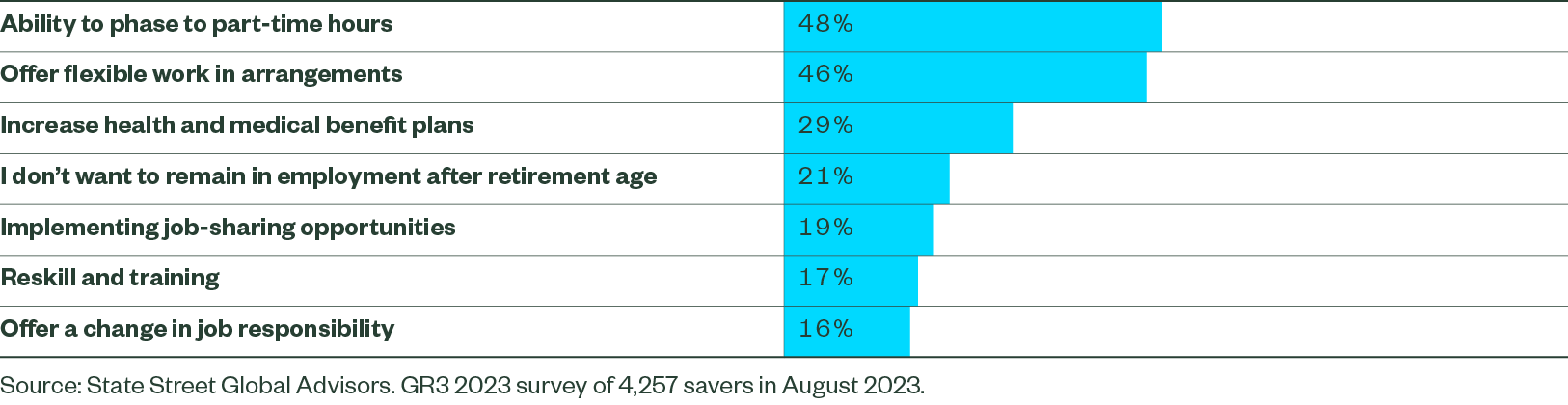

Flexible working – which has become more prevalent following the pandemic – and supporting part-time hours were the two most popular types of support selected by respondents.

Figure 13: What support would enable you to remain longer in the workplace?

Ultimately, however, the decision to retire can depend on a variety of factors, often outside of an individual’s control. Illness, family situations and cost increases can all affect when people can afford to retire.

“Difficult to retire at 65 now. Will need to work until 70 to pay the mortgage.”

“Following a family illness, I have reviewed all our financial investments and I had hoped to retire in 15 years but it’s more likely to be 20 years now.”

Key finding 6: The importance of sustainable investment

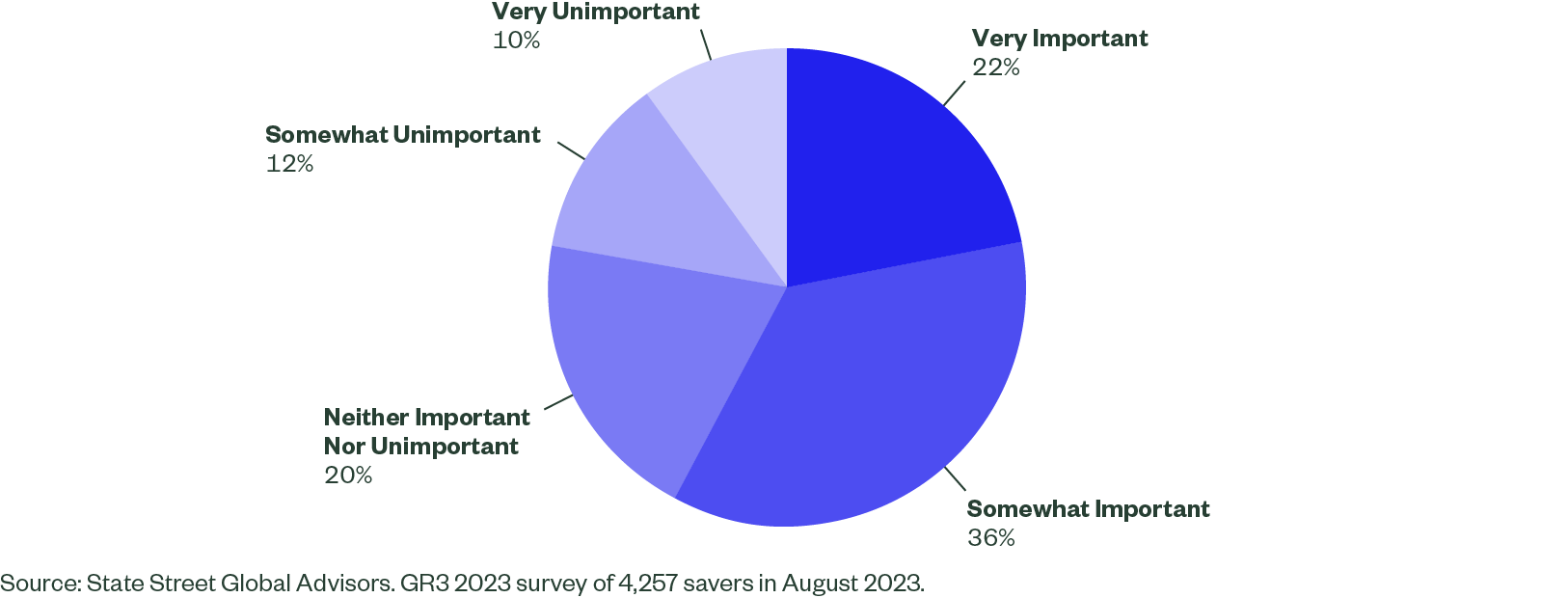

In common with investment trends observed worldwide, Irish respondents place a high level of importance on sustainable investing, which takes account of environmental and social impacts. More than half (58%) said this was either “very” or “somewhat” important, and just 22% said it was not important.

Figure 14: How important is it that your pension is invested sustainably (also known as investing which takes into account environmental, social and governance considerations)?

Half (54%) of Irish pension investors expect sustainable investing issues to be implemented as standard by their pension provider on their behalf. This makes it important to understand what priorities investors have.

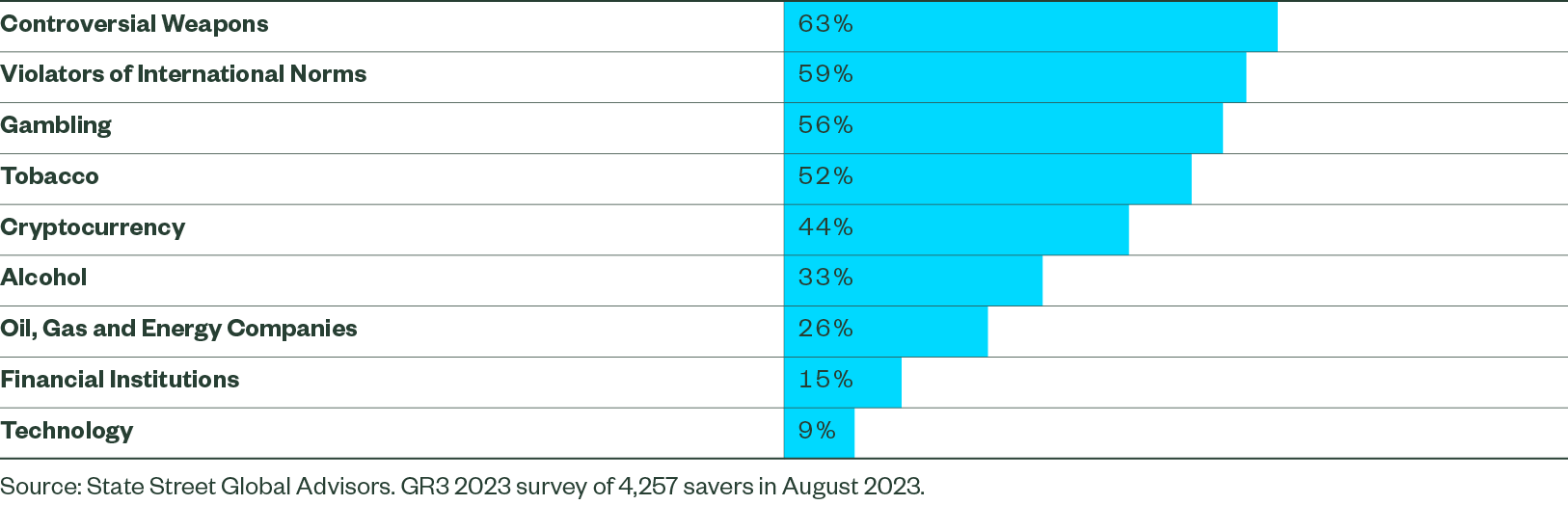

Figure 15: Which sectors would you not want your pension invested in? Please select all that apply.

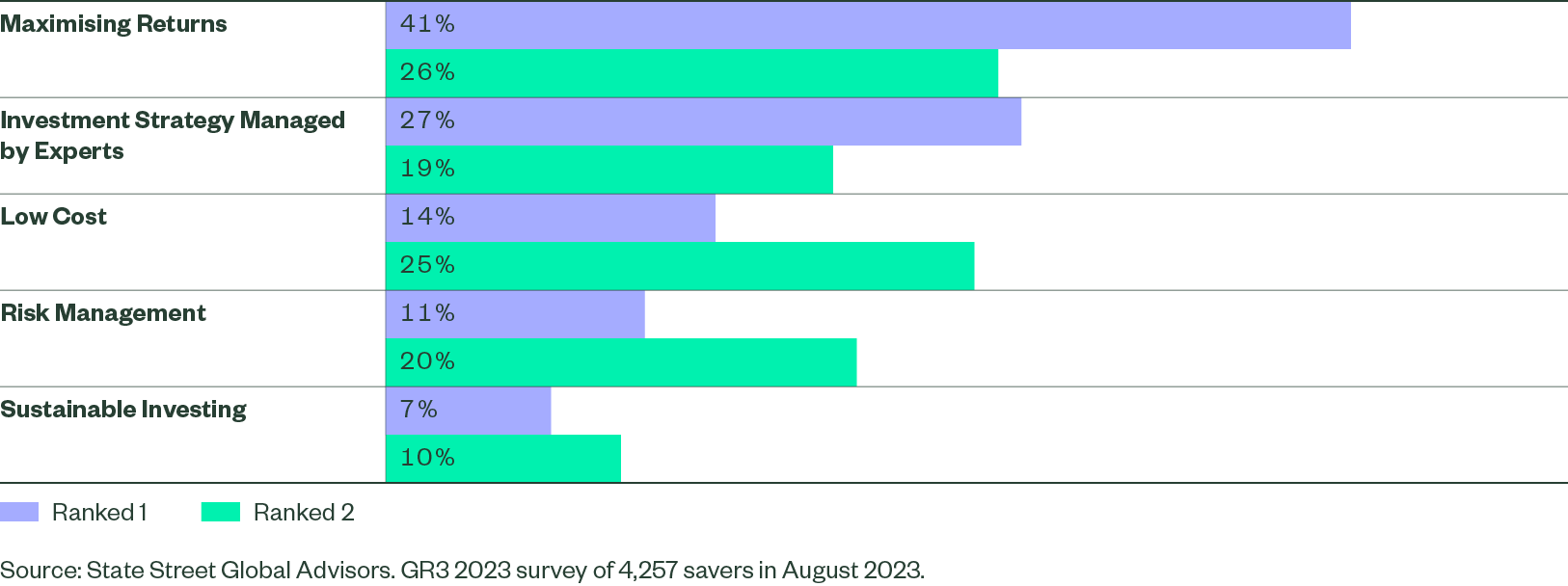

There is an important balance to be struck between accounting for sustainability concerns and considering other factors such as investment returns, risk management and costs. Sustainability tends to rank lower on investors’ priorities, but many still expect pension providers to take environmental, social and governance issues into account.

Figure 16: Please rank the following priorities (ranked 1-5)

Closing thoughts

Automatic enrolment and the master trust system together are set to revolutionise the Irish pensions landscape. While it has taken a while to get to this point, the changes are timely as our research demonstrates – the cost of living has undermined people’s confidence in their ability to retire, and they need a boost to their savings.

This will not be a quick fix. It will take many years to see the full impact of the changes, during which other challenges may arise. However, with a robust system and providers in place, policymakers and the pensions and investment industries can help to ensure people understand their retirement savings, options and how to make informed decisions.

Survey Methodology

Our global online survey, conducted during August 2023 with international data analytics firm YouGov, engaged a total of 4,257 individuals participating in workplace-sponsored savings plans (or the market equivalent) in Canada, Australia, Ireland, the UK and the US. Surveyed countries represent a range of retirement systems. Gender, age, and regional quotas were balanced to reflect employed populations within each country.

By gaining saver sentiment, we’re seeking to further our global goal of making retirement work for people, plans and policymakers in a changing world.