Unlocking the Securities Lending Potential of UCITS ETFs

- Relying on the expense ratio to assess an ETF’s total cost is limiting — it’s important to also consider other factors like securities lending potential.

- Securities lending, an essential component of capital markets activity, facilitates settlement, injects liquidity, and fosters confidence among price makers.

- European UCITS ETFs have seen a steady increase in both availability and demand during the previous 10 years, a trend that looks set to continue into 2023 and beyond.

Securities lending, or the exercise of loaning securities to other market participants, is a key aspect of capital market activity that facilitates settlement, injects liquidity, and fosters confidence among price makers. These benefits are accessible to all types of investors, from long-term stable asset base investors to more transactional participants, such as market makers and hedge funds.

Securities Lending with ETFs

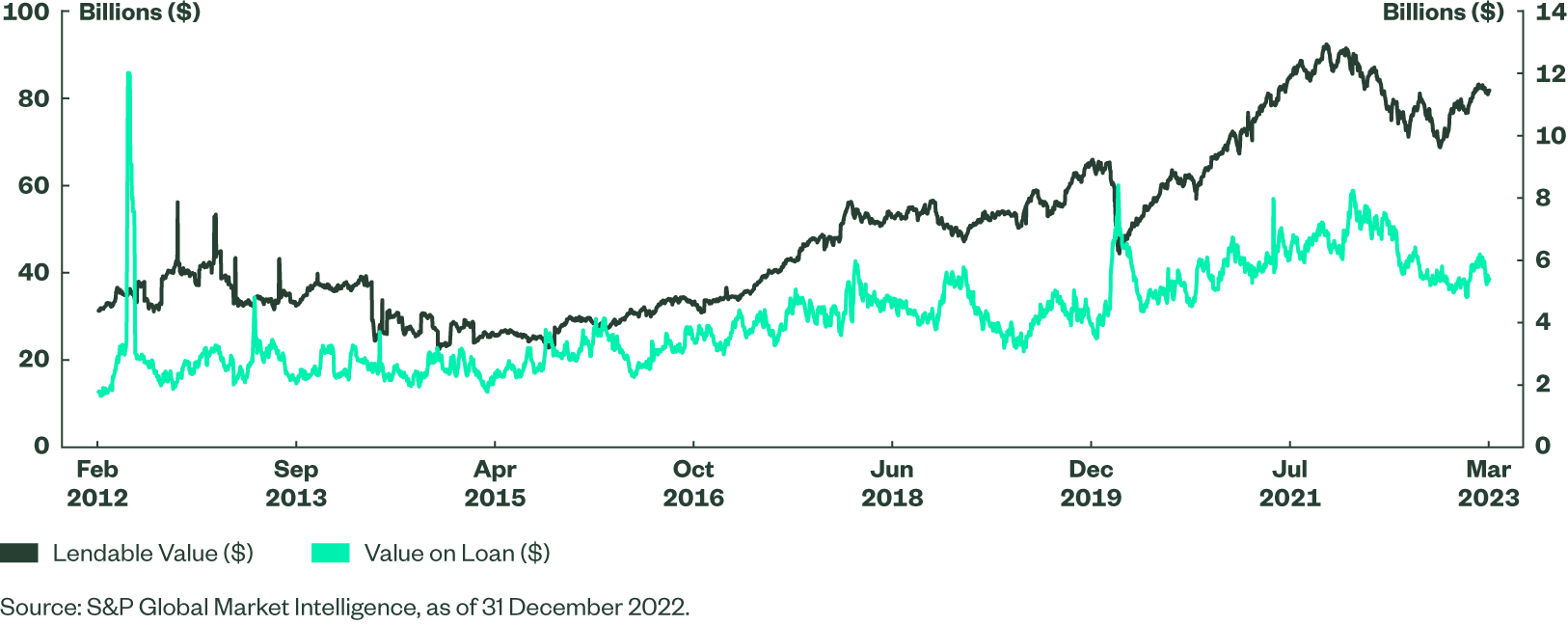

UCITS ETF securities lending has grown alongside broader adoption of the ETF structure in Europe, with lendable values increasing by 41% and values on loan increasing by 37% between 2012 and the end of 2022 (see chart below).

ETF Lending Supply and On-Loan Balances

Many investors may be familiar with “inside” lending, or the practice through which ETF issuers (or their appointed agents) lend out the constituents of the ETF to the benefit of all investors. “Outside” lending, however, refers to when ETF beneficial owners make their ETF shares available for borrowing. Under this scenario, the investor retains the choice and control of their securities lending activities and directly benefits from any returns that may be generated as the result of lending out ETF units.

In some cases, outside lending can actually serve as a more relevant driver of returns, with the potential to earn lending returns that can help offset the total expense ratio of the fund.

Why Market Participants Borrow ETF Units

There are numerous factors driving the demand to borrow. The most common reasons include: investors wish to hedge assets tracked by an ETF, market making activity in the funds themselves, and the small-but-growing lists of derivatives that track them. Borrowers of ETF units are typically market makers, investment managers, options traders and hedge fund managers that are seeking to cover pending settlements to satisfy delivery, hedge, short and/or create arbitrage opportunities.

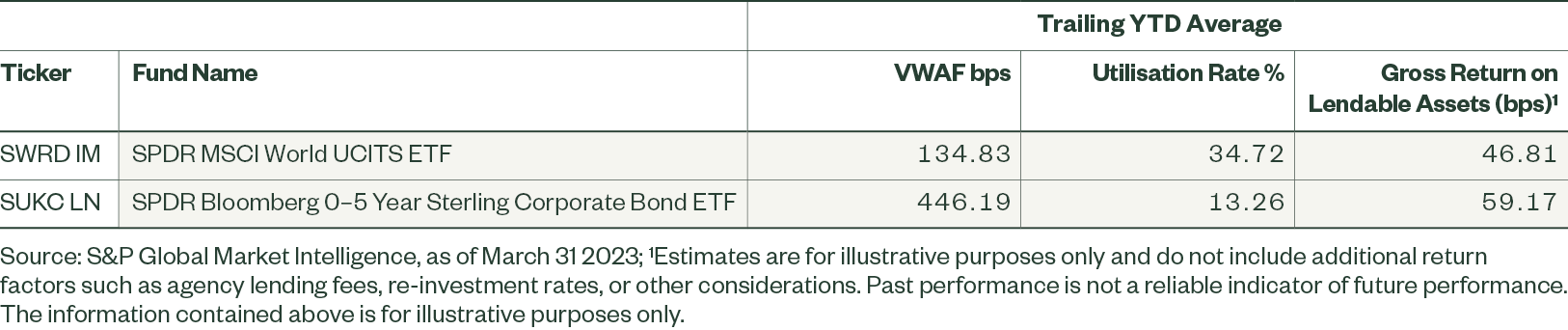

Potential Yield from Lending ETFs?

When evaluating the potential yield generated from securities lending, we can look at the volume-weighted average fee (“VWAF”) and the utilisation rate percentage:

- The VWAF represents the average fee charged by a lender to a counterparty, expressed in annualised terms.

- The utilisation rate is the shares on loan as a percentage of shares made available for loan.

To demonstrate the potential return on shares made available, we can multiply the VWAF by the utilisation rate to determine the historical return on lendable assets, as shown below. Note that fees and utilisation can vary significantly across periods so the below is indicatively only.

Connect with the SPDR Capital Markets Team

Through strong relationships with Authorised Participants, market makers, liquidity providers, execution trading desks/platforms and stock exchanges, the SPDR Capital Markets team plays an active role in supporting competitive markets and maintaining the SPDR ETF liquidity ecosystem.

The team’s insight into primary and secondary market activity – as well as access to numerous proprietary data points – can help investors to evaluate their execution strategies and meet end objectives, even in volatile markets.

Connect with the team them to learn more about the lending potential of SPDR UCITS ETFs or for any general execution-related questions.