Tokenized money market funds (MMFs): Revolutionizing liquidity management

As onchain markets demand speed and 24/7 trading, cash management is evolving. Tokenized money market funds are gaining attention for their potential both as an onchain yield-bearing store of value and as a way to improve collateral mobility, reduce operational friction, and enable more efficient balance sheet management.

Sam ten Cate

Head of Digital Asset Strategy

Liquidity matters most when it’s gone

When markets move up or down, margin calls arrive, or settlement windows close, institutions can find themselves “liquid on paper” but operationally constrained. Liquidity crises are rarely about a total absence of assets—they’re often about mobility: the ability to turn assets into usable cash or collateral fast enough to meet the moment.

Traditional money market funds (MMFs) are a cornerstone of cash management because they aim to preserve capital, provide liquidity, and generate short-term yield at scale. But the way MMF shares move still reflects legacy infrastructure. Intermediated processes, time-based cutoffs, and operational friction can show up precisely when speed matters.

Tokenized money market funds seek to address that mismatch. They keep the familiar MMF exposure, while modernizing how ownership is recorded, transferred, and used—modernization that could provide capital markets participants with greater mobility and operational resilience when it matters most.

What are tokenized money market funds?

A tokenized money market fund is a MMF where fund shares are represented as digital tokens on a blockchain or distributed ledger. Tokenized MMFs are one of the ways to modernize cash management without changing what investors value: liquidity, capital preservation, and yield. What you own is unchanged; you still own a fund share with exposure to a conservative, short-duration portfolio of high-quality government securities and cash.

Tokenized money market funds modernize MMFs and can enable investors to hold shares and transfer them natively in digital workflows, supporting near real time settlement, intraday collateral mobility, and onchain cash movement. This enables the same MMF exposure to be used more flexibly across treasury and collateral use cases without materially changing the underlying fund or risk profile. This is why tokenized MMFs are increasingly described as a next-generation cash equivalent for certain use cases: the asset isn’t new—but the rails are.

Figure 1: Traditional money market funds vs. tokenized money market funds

| Feature | Traditional MMFs | Tokenized MMFs |

|---|---|---|

| Ownership record | Account-based records via intermediaries (e.g., transfer agent) | Token-based record on a ledger (often permissioned/whitelisted tokens). A permissioned or whitelisted token can only be held, transferred, or redeemed by wallets or entities that have been explicitly approved. Eligibility rules are enforced at the token or smart‑contract level to support compliance, investor controls, and regulatory requirements |

| Transfers | Ownership typically changes through subscriptions and redemptions processed by a transfer agent; shares are account‑based and not natively transferable between independent parties | Potentially faster transfer of ownership within whitelisted investor groups |

| Transparency | Periodic reporting; reconciliations common | More continuous visibility into token movement and ownership state |

| Collateral utility | Mobilization can be operationally slow | Portability can improve within permitted venues and workflows |

| Compliance controls | Traditional investor onboarding | Traditional onboarding plus onchain transfer constraints (e.g., whitelists) |

Source: State Street Investment Management.

Why tokenized money market funds are reshaping cash management

As institutions place greater emphasis on time-to-cash, collateral mobility, and operational efficiency, tokenized MMFs are increasingly viewed to bridge traditional cash instruments with modern settlement and treasury needs.

Demand is shifting from “liquidity” to “liquidity you can move”

Institutions increasingly care about time-to-cash and time-to-collateral, not just portfolio liquidity labels. Tokenized MMFs are gaining traction because they enable enhanced access to liquidity, 24/7, without the constraints of traditional banking hours.

Continued adoption of tokenized assets

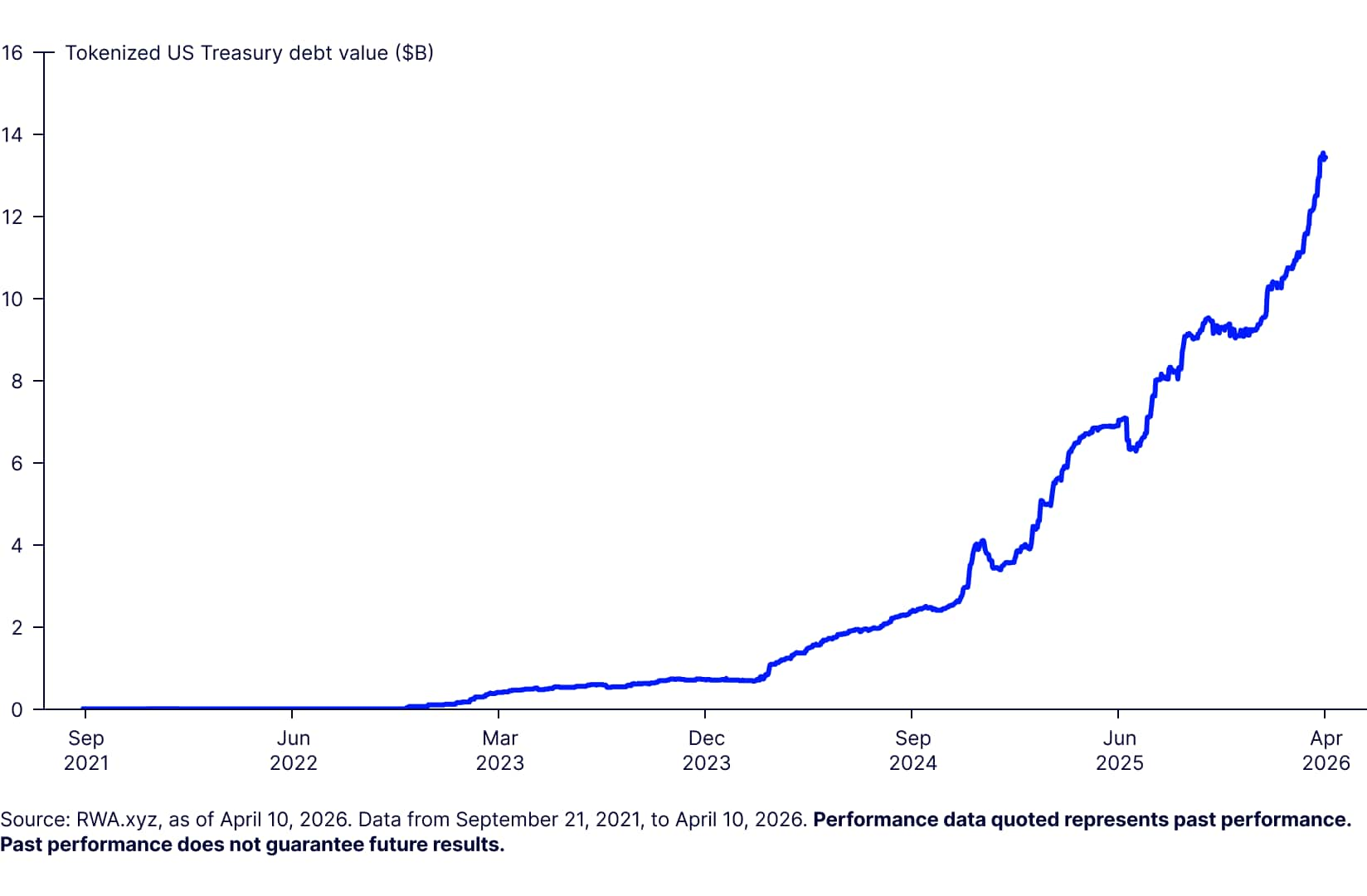

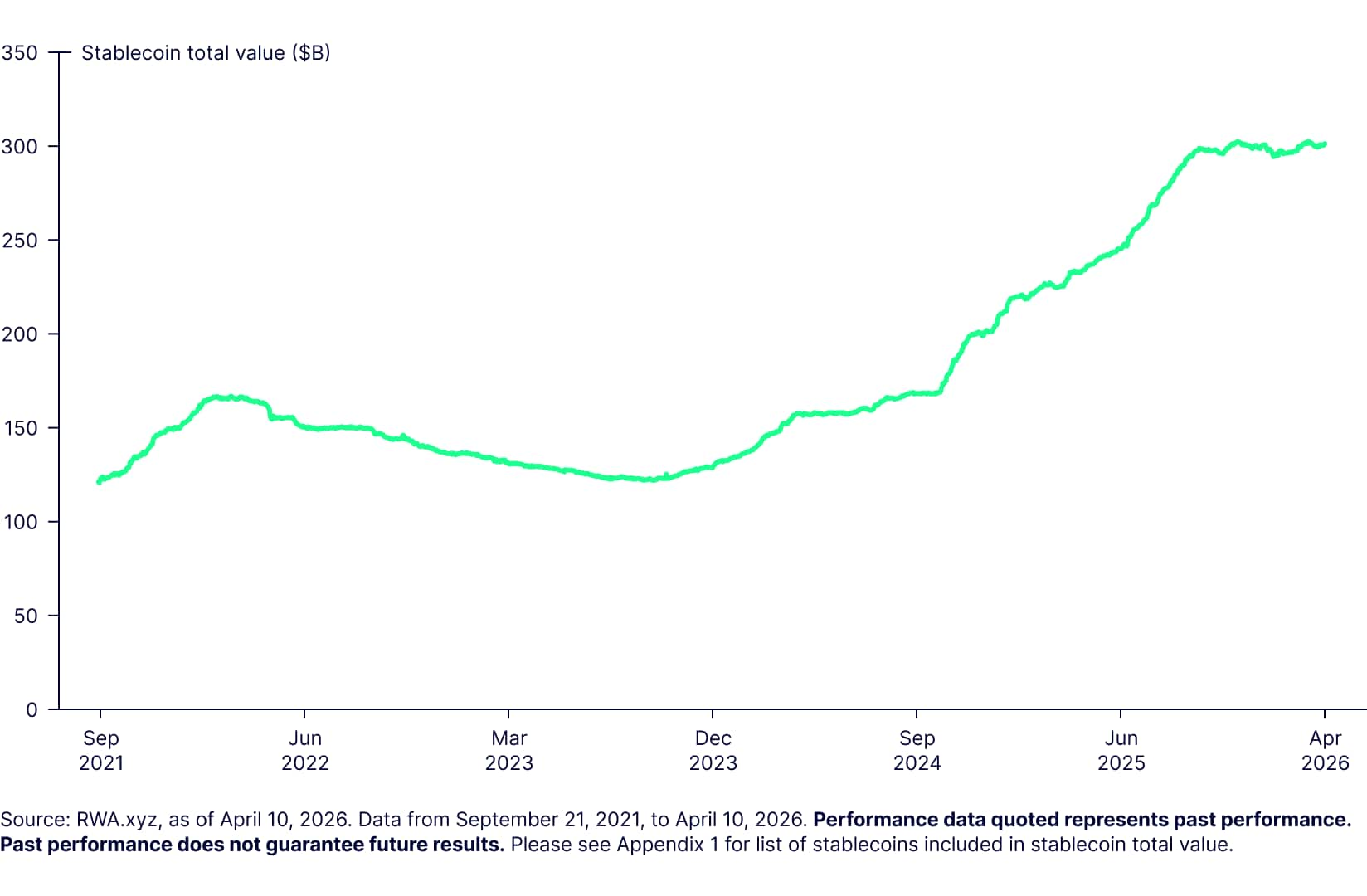

Tokenized cash has grown to a nearly $300 billion ecosystem,1 dominated by stablecoins—which are being supported by recent favorable regulatory structure—with tokenized Treasurys and money market funds at nearly $13 billion after strong year-on-year growth.2

Figure 2: The explosive growth of tokenized Treasurys

Figure 3: Stablecoins continue to see growth

Improving regulatory clarity

Regulatory clarity around the world is also improving. In the US, the GENIUS Act established a framework for stablecoins, and other proposed legislation such as the CLARITY Act aims to reduce uncertainty across digital asset markets more broadly. As these frameworks continue to take shape, tokenized money market funds are becoming more practical as an extension for cash vehicles.

At the same time, regulators and market infrastructure providers are beginning to address how tokenized funds fit into core financial systems. The Commodity Futures Trading Commission has proposed allowing certain tokenized money market funds to be posted as margin and collateral in derivatives markets, signaling growing comfort with their use in regulated risk management workflows. In parallel, clearing and settlement infrastructure players are actively piloting tokenized collateral and shared ledger infrastructure, reinforcing the view that tokenized MMFs are moving from experimental assets toward institutionally usable building blocks within the existing financial system.

Internationally, regulators are also converging on clearer treatment of tokenized fund structures. In the EU, the Markets in Crypto-Assets Regulation and related work on distributed ledger technology market infrastructure are clarifying how tokenized fund interests can operate alongside traditional UCITS and money market fund regimes, reinforcing that tokenization can modernize distribution and settlement without changing the underlying regulatory perimeter. In Asia, jurisdictions such as Singapore have explicitly supported tokenized funds within regulated frameworks through Project Guardian and related guidance. In the Middle East, jurisdictions such as the UAE are also advancing regulatory clarity, with Abu Dhabi Global Market and Dubai’s Virtual Assets Regulatory Authority establishing defined regimes for digital assets, tokenization, and stablecoin activity within supervised financial centers. These frameworks are positioning the region as an institutional hub for regulated tokenized funds and onchain collateral use, particularly for cross border liquidity and capital markets applications.

Institutions are prioritizing operational efficiency

In State Street’s Digital Assets and Emerging Technology Study, respondents cited the top benefits of tokenization and digital trading as better transparency, faster and more efficient trading, and lower compliance costs (Figure 4).3 These are not crypto-native motivations; they are operational and risk outcomes that traditional institutional clients already measure and value.

Potential benefits of tokenized money market funds

The potential benefits of tokenized money market funds are largely operational, showing up in how liquidity is mobilized, managed, and put to work.

Programmable liquidity

Tokenization also opens the door to rule-based controls—transfer restrictions, eligibility checks, and workflow automation—enforced directly at the token level through smart contracts. This can make liquidity programmable: smart contracts can automate onchain cash sweeps, moving idle balances into yield-bearing money market tokens or mobilizing liquidity for settlement or collateral. This is done based on pre-defined thresholds and timing rules, which may reduce operational risk by making controls consistent, transparent, and machine-executable.

Enhanced liquidity and settlement

When you can move ownership efficiently within a controlled network, you potentially improve just-in-time liquidity. That matters in collateral workflows, treasury rebalancing, and periods of market stress when operational friction becomes a cost.

Additionally, tokenization can reduce dead time, even if underlying markets and banking rails still have hours and cutoffs. Tokenized ownership can help institutions pre-position, transfer, and operationally prepare liquidity and collateral with fewer manual steps. It can show up in fewer exceptions, tighter control over timing, and better compatibility with global operating hours and allowing cash to work harder.

Faster mobility

Traditional MMF shares were built for an account-based world, not a world where collateral needs to move quickly across venues, time zones, and counterparties. Tokenized MMFs can make positions more portable within approved networks, and ownership transfers and certain workflows can operate outside of legacy market-hour constraints. This helps convert a “cash equivalent” into a more usable building block for modern liquidity stacks.

Mobility is also about optionality. The more easily an institution can move, use or pledge a cash position, the less liquidity an institution needs to hold “just in case.” Over time, that can reduce idle balances—which can translate to better capital efficiency and more resilient liquidity management.

Potentially lower costs

Fewer intermediated handoffs can mean fewer reconciliations, fewer breaks, and less manual processing which can reduce operational costs. Tokenization may also improve traceability of transfers, which can simplify exception management and operational oversight. Savings will vary by design and scale, but even modest reductions in processing friction and exception rates can be meaningful.

Improved transparency

Tokenized money market funds can provide greater continuous transparency into ownership, transfer activity, and position status than traditional, account based fund records. Because ownership is represented on a ledger, institutions can gain near-real-time visibility into where shares sit, whether they are encumbered, and how they move between different counterparties. This can reduce reconciliation gaps between treasury, collateral, and operations teams, particularly in environments where positions are actively repositioned intraday.

Importantly, this transparency is at a token level, not at the portfolio level: the underlying fund continues to operate with the same NAV process, reporting cadence, and regulatory protections as a traditional MMF. What changes is the efficiency and consistency of the ownership record and transfer trail. For institutions managing liquidity across multiple venues and time zones, clearer visibility into cash positions and movements can translate into fewer exceptions, stronger controls, and greater confidence that liquidity is available—and usable—when it is needed most.

Tokenized money market funds in action: Key use cases

Tokenized money market funds are being used today across several distinct workflows, each tied to a common theme: making cash more mobile without changing its underlying risk profile.

Collateral management

Collateral is a time-sensitive instrument. Tokenized MMFs can make a conservative, yield-bearing asset more usable by improving how quickly it can be posted or repositioned within permitted networks. This is particularly attractive in cash-dominated collateral work flows that limit yield opportunities. The Bank for International Settlements (BIS) explicitly describes tokenized MMFs as a fast-growing collateral asset in the crypto ecosystem, which reflects real demand for portable, onchain cash equivalents.4

Integration into decentralized finance (DeFi) as a yield-bearing store of value

In decentralized finance, liquidity is typically built from a stack of onchain instruments—stablecoins or deposit tokens for settlement and yield-bearing assets for collateral and treasury management. Tokenized money market funds sit alongside stablecoins and deposit tokens as a distinct model, designed to fill the yield-bearing “cash equivalent” role in that stack rather than compete directly on payments or settlement speed.

While stablecoins are optimized for price stability and transactional utility, they generally do not generate yield and can be costly to hold at scale for treasuries, protocols, or market makers. Tokenized MMFs, by contrast, offer exposure to regulated, short-duration government securities in a form that can be held onchain, making them better suited for use cases such as DeFi treasury reserves, margin and collateral posting, liquidity backstops, and automated cash management within smart contracts.

Tokenization of assets: How it’s reshaping finance and markets

See how tokenization is becoming a part of the market structure beyond cash—from art to real estate.

Treasury management and short-term liquidity

For corporate treasurers and institutional cash managers, tokenized MMFs can enable faster repositioning of liquidity and potentially tighter alignment between cash holdings and settlement/collateral needs.

How tokenized money market funds work

While structures vary, the operating pattern is consistent:

- Onboard eligible investors

Potential investors make subscription requests and eligibility is confirmed. Investors then complete Know Your Customer (KYC) and Anti-Money Laundering (AML) checks, and approved wallets are whitelisted (where applicable). This ensures only authorized participants can hold or transfer fund tokens. Note: investors must have the appropriate digital asset wallet in order to hold the fund tokens - Subscribe to the fund

An investor subscribes through an approved platform or channel into a token-enabled share class or to a digitally native token - Mint tokens representing shares

Tokens are issued to the investor’s verified wallet/custody arrangement to represent ownership - Hold and service the position

The fund continues to operate as an MMF (portfolio management, NAV process, disclosures). Token records support ownership state and transfer history - Transfer, pledge, or integrate into workflows

Within approved networks, tokens can move between eligible parties or be used in collateral/treasury workflows - Redeem and burn

Tokens are burned on redemption and proceeds are returned through the applicable settlement route

What to look for in a tokenized money market fund

If you are evaluating tokenized MMFs, focus on the fundamentals:

- Subscription and redemption capabilities and timing: Which stablecoins are accepted for subscriptions and redemptions, whether access is limited to defined windows or available intraday or 24/7, and how liquidity is managed outside traditional market hours. Assess the availability, cutoffs, and settlement mechanics of the tokenized MMFs

- Regulatory perimeter and investor protections: Tokenized MMFs are generally classified as securities; structure and governance matter

- Underlying portfolio investment strategy and liquidity profile: The token is a wrapper; the portfolio still drives risk

- Permissioning model (whitelists, transfer rules): Who can hold, who can receive, and under what conditions

- Operational infrastructure and resiliency (service providers, custody, controls, monitoring): This is where institutional-grade implementation is won or lost

Risks and challenges: What investors should know

Regulations are still developing

Regulatory approaches remain uneven across jurisdictions, and market practices are still maturing. The BIS has noted that tokenized money market funds can replicate—and in some cases amplify—the risks present in traditional MMFs, while also introducing new considerations related to operational resilience, governance, and onchain infrastructure.5

Infrastructure and custody challenges

Tokenization adds a new dependency stack: wallets, key management, smart contracts, and platform governance. That increases the need for strong operational controls and oversight, not less. This is why using a traditional, regulated financial institution matters—you will outsource this to a trusted third party.

Cybersecurity and KYC/AML risks

Onchain liquidity tools must pair speed with identity, monitoring, and enforceable transfer constraints. BIS explicitly calls out operational and AML/CFT risks in the tokenized MMF ecosystem.6 Compliance design is central to adoption.

Transitioning to tokenized: How to get started

Getting started is straightforward if you treat it like any other operational upgrade—clear use case, right access model, and strong controls.

- Pick the use case that matters most. Start where speed and mobility create real value: intraday liquidity, collateral posting, after hours readiness, or treasury rebalancing across entities.

- Set up your access stack (wallet + custody). Choose an institutional-grade wallet/custody model with clear authorization controls and operational governance. This is the foundation that makes onchain cash instruments usable at scale.

- Choose your operating environment. Decide whether you want to operate on a permissioned network or a public chain with whitelisting and transfer controls. The right choice is the one that fits your compliance posture and the venues where you expect to use the asset (Figure 5).

Figure 5: Comparing distributed ledger archetypes

| What matters to an investor | Private-permissioned | Public-permissioned | Public-permissionless | Investor perspective |

|---|---|---|---|---|

| Access and ecosystem use | Access is tightly controlled; use is mostly inside a closed network | Access is controlled, but tokens can connect to a broader digital ecosystem | Open access and widest potential ecosystem connectivity | Architecture affects where investors can hold, move, and potentially use the fund token |

| Privacy and compliance | Strong privacy and clear investor controls | Privacy and controls can be built in | Lower default privacy; controls often rely on added layers | Permissioning generally supports a more controlled investor experience |

| Operational design | More centralized and tightly managed | Blends network reach with defined controls | More open, with greater dependence on public-chain infrastructure | The design shapes reliability, transparency, and how the product functions in practice |

| Best fit for tokenized MMFs today | Well suited for closed institutional use cases | Strong fit for regulated products seeking broader connectivity | Better suited to fully open, crypto-native use cases | Different architectures support different investor use cases |

Source: State Street Investment Management.

4 Evaluate products like you would any MMF—then add token-specific diligence. Look at the underlying assets, liquidity profile, and redemption mechanics, plus token transfer rules, settlement paths, and how ownership is recorded and monitored.

5 Pilot, measure, scale. Start small, track time-to-mobilize and operational exceptions, then expand once the workflow benefits are proven. Institutions are already prioritizing transparency and efficiency as the reasons to adopt tokenization—this is how you capture it in practice.

Tokenized MMFs are about making cash management work the way modern markets actually operate. Tokenization does not eliminate risk, but it can eliminate unnecessary delay embedded in today’s plumbing—such as limited Fedwire operating hours, daylight overdraft constraints, batch-based settlement cycles, and multi-step payment legs that force liquidity to sit idle despite being economically available.

By enabling atomic settlement, extended availability, and programmable transfer of fund interests, tokenization can compress settlement timelines and improve intraday liquidity mobility. In liquidity and balance sheet management, reducing these frictions is a meaningful upgrade: cash can be deployed, recalled, or rebalanced more efficiently across funding, margin, and investment uses. While tokenization introduces new operational and technology risks that must be understood and managed, the net effect is the potential for more precise, responsive, and capital efficient cash management.

Digital assets: Educational resources for investors

Explore expert insights and educational resources to help you navigate crypto, blockchain, and tokenized markets with confidence.