Implementation: Going from Theory to Action

In our systematic fixed income investing process, we use factor-driven signal scores from Barclays Quantitative Portfolio Strategy (QPS) as an input to an optimization process for constructing portfolios that maximize exposure to high scoring bonds as we seek to generate excess returns versus client benchmarks (see Building a Portfolio: A Closer Look at Our Process).

In this piece, we discuss our process for translating this optimization process into a portfolio (purchasing the actual holdings), and we share our thoughts about the similarities between systematic investing and index investing. Our goal is to help clients tap opportunities within the tremendous breadth and fragmentation of the fixed income market.

Sourcing the Bonds

Our backtesting indicates that corporate bonds that exhibit favorable exposure to certain style factors (in this case, Value, Momentum and Sentiment factors) tend to outperform those that do not. Hence, one of our goals in managing systematic portfolios is to maximize the combined score of the bonds in the portfolio, subject to risk constraints, while controlling the cost of implementation. In a systematic strategy, it is less about having exposure to a specific issuer or bond, and more about having exposure to bonds that may exhibit high sensitivity to the designated style factors. In this way, a systematic approach is similar to a stratified sampling index replication process, which focuses on controlling portfolio exposure to specific risk factors (as opposed to full index replication) at the level of individual bonds. This approach introduces great potential for security substitutions, and ties closely to our proven process of sampling in the construction of indexed portfolios.

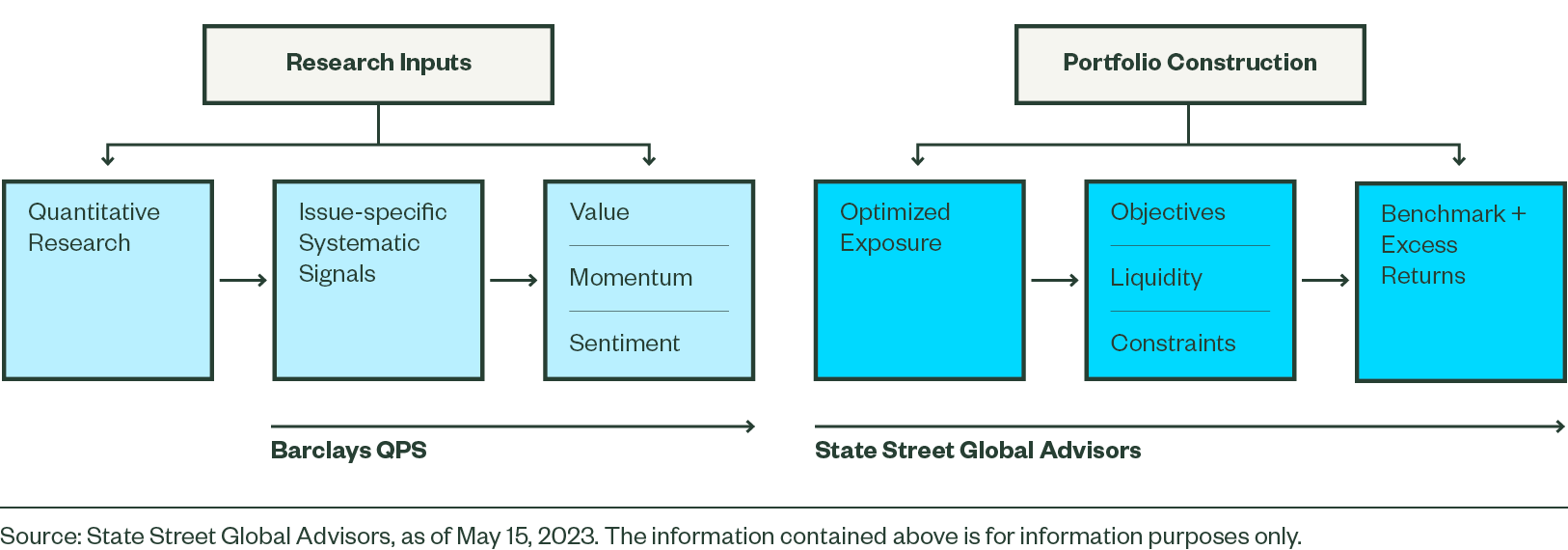

An effective implementation approach must allow for security substitution with flexibility in bond selection. In the selection process, we rely on bond-specific signals while tightly controlling exposure to several key risk dimensions, which include duration, quality and Duration Times Spread, or DTS. (The Barclays QPS team pioneered DTS.) While implementing risk constraints, we can appropriately tradeoff the tolerance of constraint matching with criteria such as liquidity and valuation (Figure 1).

Figure 1: We Use a Disciplined Process to Identify and Capture Outcomes

Meeting the Challenges

The portfolio implementation process requires trading expertise, access to data, and the ability to manage the size of transactions and the nuances of the fixed income markets. For systematic active fixed income, here are three of the most prominent challenges:

Challenge: The bond market is broad, opaque and fragmented.

Solution: We are not passive and see market imperfections as potential opportunities for alpha generation, rather than a problem. The breadth of the market is also an advantage for systematic strategies as it enhances the scope for generating alpha. Given our more than $500 billion in fixed income indexing AUM, we can add value as a specialist in sourcing bonds (even in complex fixed income markets), in taking advantage of liquidity premiums, and in trading bonds that are lacking in price transparency. We have a wide range of techniques already in place for our indexing strategies that are directly transferable to systematic fixed income.

For example, we may look to capitalize on new issue, or primary market price concessions. When a bond launches, it is often offered at a lower price relative to existing bonds trading in the secondary market. Then, the bond price rises, allowing us to “harvest” the premium.

Challenge: Sampling entails a cost-benefit trade-off.

Solution: Portfolio optimizations may indicate exposure to certain issues given risk constraints and scores, but this can come with a cost. For portfolio managers and traders, the key is to determine which criteria can be substituted to efficiently create in practice a portfolio that in total reflects the desired characteristics.

The keys to successfully making this tradeoff is deep collaboration between Barclays QPS and the State Street Global Advisors fixed income team, as implementation is both art and science. Our data capabilities allow us to dynamically model the “costs” of hewing closely to what’s dictated by the signal scores. Using advanced liquidity metrics and feedback from our traders, we can determine a combination of costs and benefits in order to maximize portfolio performance.

Challenge: Risk parameters are dynamic.

Solution: To maintain portfolio positioning through ever-changing market conditions, we monitor bond and issuer characteristics (including equity metrics) each day, as we receive daily feeds from Barclays QPS on all index constituents as part of a custom systematic strategy index developed by Barclays QPS. Understanding the data and adjusting to it is a continuous process. We have instituted an array of processes to make sure that the portfolio not only remains within specified ranges of the benchmark in parameters such as duration, sector, quality and DTS, but also maximizes security selection signals such as value, momentum and sentiment.

In addition, over time, we proactively manage changes/events in held issuers that could impact returns, such as M&A announcements, proxy votes, new issues, or change of control events.

Challenge: Transaction costs in fixed income can be meaningful. How can the benefit of return-seeking turnover be balanced with the associated increase in transaction costs?

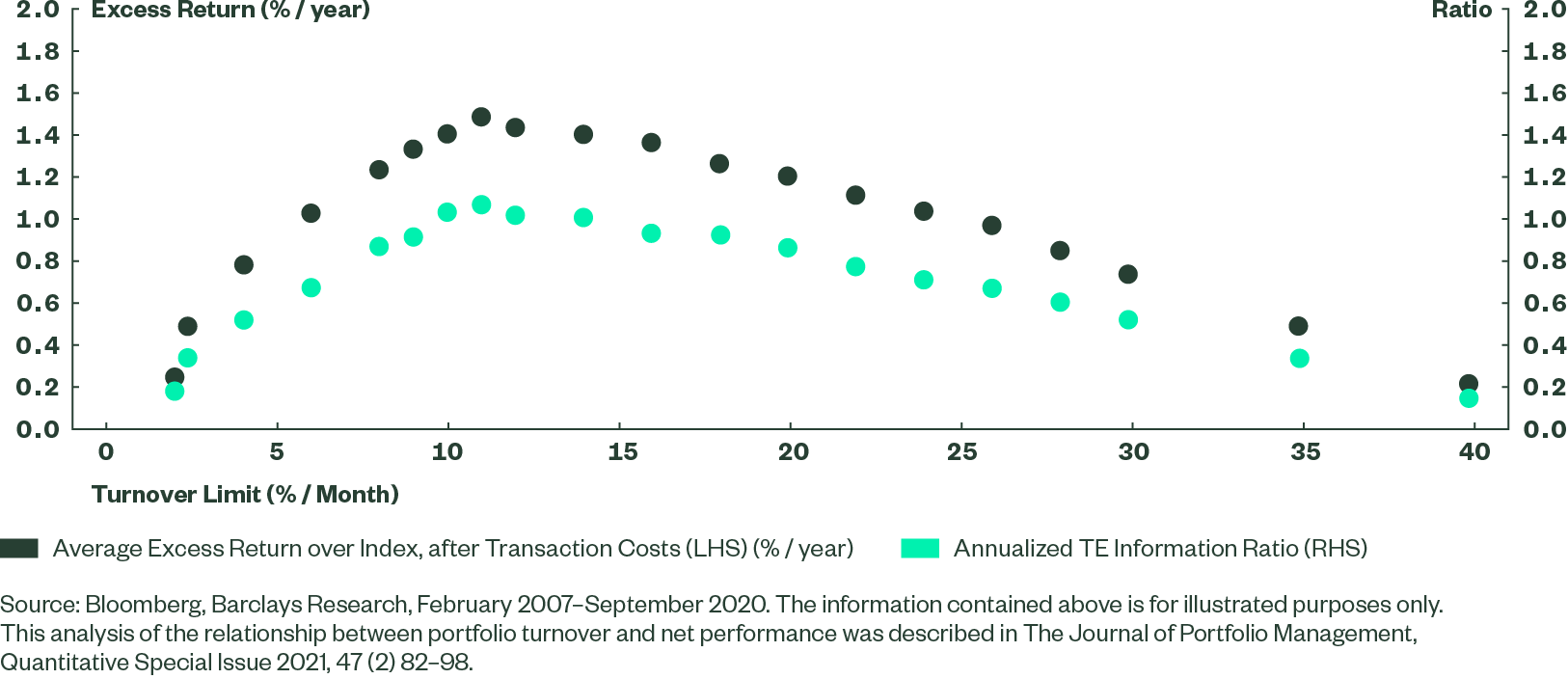

Solution: Barclays QPS has performed analysis to determine the level of turnover appropriate to maximize net realized alpha. Evaluating a proposed strategy in a back-tested portfolio, one can solve for the optimal portfolio expected to generate outperformance relative to the benchmark on a steady basis. Transaction costs can substantially reduce the value generated by the strategy. Our analysis suggests that controlling portfolio turnover may help improve net performance (Figure 2).

Figure 2: Net performance Is Maximized for Intermediate Levels of Portfolio Turnover

We investigated different techniques for potentially maximizing performance net of transaction costs. Research also showed that there is an optimal level of credit portfolio turnover that was about 10%/month on average in recent years. Below that level, the signal value is not fully captured. Larger turnover budgets can result in excessive transaction costs which have the effect of reducing net performance and could even make it negative. Alternatives to a fixed limit on turnover are direct control of transaction costs or optimization of expected alpha net of transaction costs.

State Street Global Advisors Capabilities: Lessons from Indexing

Our clients rely on us as an index manager to source a wide range of market exposures across various fixed income sectors, which vary in liquidity requirements and are often customized. This service requires a continuous, intraday understanding of bond market dynamics, costs, and liquidity. Sourcing bonds is a core part of our indexing franchise, spreading across vehicles such as liquid ETFs to more customized portfolios. The skills we have gained as an index manager and as a financial institution trading massive volumes are equally applicable to implementing systematic active fixed income portfolios. In particular, careful sampling is key to both passive and systematic investing. The process of sampling — turning theory into reality and building portfolios with alternative bonds — has nearly the same skill and data requirements for indexing and systematic active fixed income (Figure 3).

Figure 3: Required Capabilities for Systematic Active Fixed Income Overlap with Indexing Competences

Capability |

Indexed Fixed Income |

Systematic Active Fixed Income |

|---|---|---|

Human capital, technology, and infrastructure to determine appropriate trade-offs |

X |

X |

Tools for comparing risk parameters in target portfolio |

X |

X |

Daily adjustments to changing criteria |

X |

X |

Experience with complex credit exposures |

X |

X |

Data-intensive security selection |

X |

X |

Source: State Street Global Advisors, as of May 15, 2023.

Our core competency as an index manager provides us with the base of knowledge, the people, and the systems to expertly design and implement systematic active fixed income strategies. For fixed income portfolios, despite dramatic improvements in efficiencies and liquidity due to electronic trading platforms, there are still pockets of the market that are quite complex and potentially expensive to trade. This can present challenges in implementing a systematic investment style in asset classes such as emerging market debt or even high-yield debt. Our experience in fixed income indexing allows us to effectively perform sampling informed by quantitative signals— even in less liquid and homogeneous markets—and to implement trading techniques that can improve execution and lower costs.