Active and Index: Fixed Income Building Blocks

While the active versus passive management debate persists, the real question is how to combine the best of both approaches. We look at how active managers have performed, the shift towards indexing, and how a blend of active and index strategies can be incorporated into a fixed income portfolio.

The performance of fixed income active managers has historically been mixed and often inconsistent. The lack of consistency in the performance of actively managed strategies, where most managers have typically failed to beat their benchmark in consecutive years, underpins the argument for diversifying into indexed strategies. The shift towards indexing is also driven by technological advancements across fixed income markets, providing investors more efficient access to market liquidity, thereby potentially eroding traditional sources of alpha. Index strategies may be considered where active managers have difficulties generating adequately large and consistent net-of-fee alpha. In markets where sustained and sufficient alpha can still be found, an active or a hybrid approach can be considered to optimize risk and cost-adjusted returns.

When it comes to the adoption of indexing in broader institutional fixed income portfolios, levels vary across regions. Australia and Japan have the highest exposure to indexing, followed by EMEA and the US, while the rest of Asia is still predominantly investing in active fixed income. Hiring active managers to run global aggregate bond mandates is a popular approach to investing in global fixed income across Asia. This approach has largely been justified by performance, although recently performance has been somewhat challenged. However, as fixed income markets become more efficient, investors are starting to utilize a modular approach to select the most effective way, across active and index solutions, to access each fixed income exposure to achieve their portfolio requirements.

By utilizing a building block approach to fixed income portfolio construction, investors can select the most effective way to access each fixed income segment in order to achieve their objectives. A blend of active and indexing building blocks can be used to replicate a fully active global aggregate mandate as well as broader global fixed income portfolios that incorporate emerging market debt or global high yield sleeves. Our findings show that utilizing a mix of active and indexing can often create better, more consistent return outcomes, while reducing overall portfolio risk and costs.

The Global Shift to Fixed Income Indexing

- Fixed income indexing strategies have continued to see global inflows. Technological advancements across fixed income markets are providing investors more efficient access to market liquidity while eroding alpha opportunities which has been a contributor to the shift towards indexing.

- Three key drivers for a shift towards indexing we see are fees, tracking error budgeting, and a disaggregation in fixed income exposures. As fixed income markets become more efficient, investors are starting to utilize a modular approach to select the most effective way, across active and index solutions, to access each fixed income market.

- Asian institutional investors have been slow to incorporate index strategies into their fixed income portfolios as compared to the major developed markets. We would expect this to change as Asian investors also appreciate the benefits of a granular approach to their fixed income portfolios.

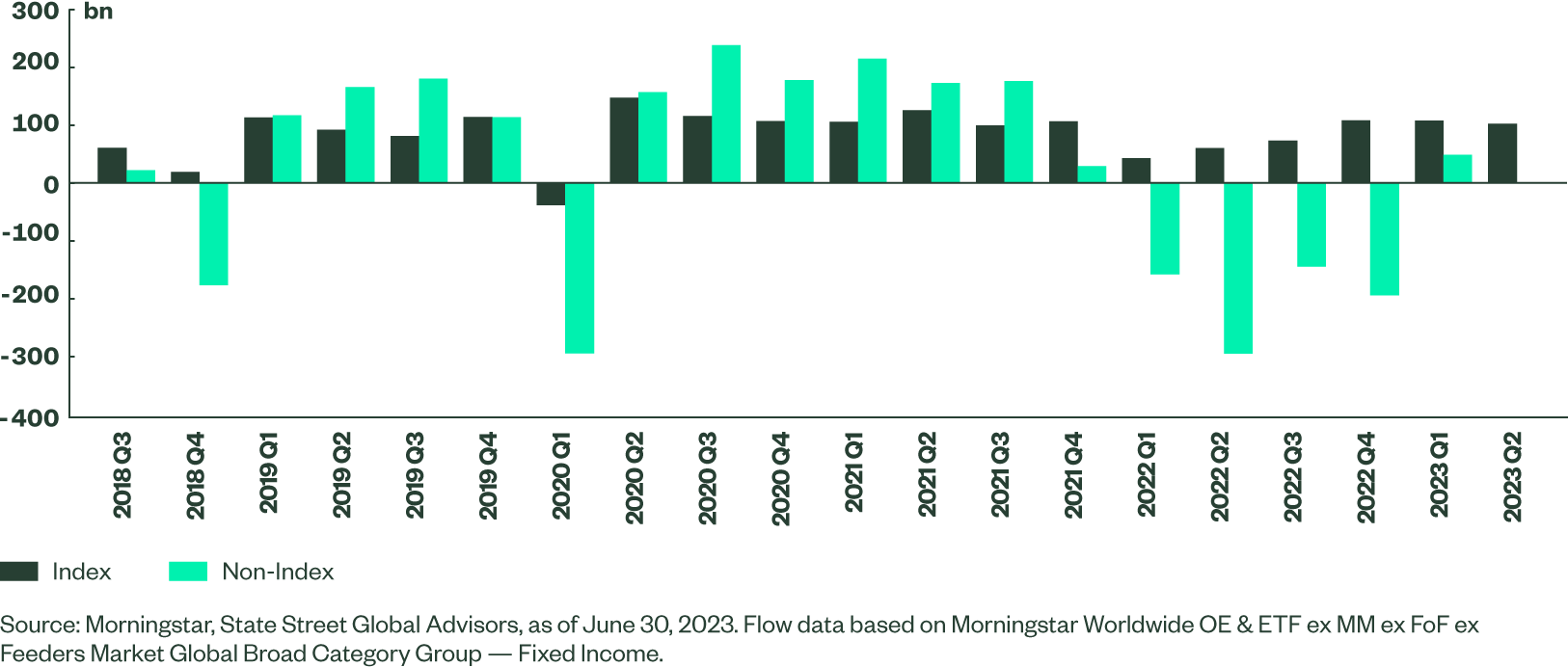

Steady Inflows into Index, While Active Strategy Flows Are Volatile

The shift from active to indexing has been a long-standing trend in equities but has been less prevalent in fixed income. While we have seen continuous flows into indexing, inflows into active strategies remained strong until recently. Over the last few years, flows into fixed income have been poor as global central bank policy has pushed up yields, pulling down returns. Despite this, on a global basis, indexing strategies continued to garner inflows while active fixed income strategies saw significant outflows as shown in Figure 1 below.

Figure 1: 5-Year Net Flows in Fixed Income Open-ended Funds and ETFs

Technological Advancements Aid Shift to Indexing

The structural shift towards index investment has been ongoing for years with the trend accelerating driven by the pandemic and subsequent rate hikes. Cost-efficiency and relative net performance are key drivers of the flows. In the long run, innovation and technology have facilitated the development of fixed income indexing solutions with improving market efficiency. Technological advancements, such as electronic trading systems, have significantly improved market transparency and enhanced information sharing, data analysis, counterparty identification and order transactions, providing investors more efficient access to market liquidity while eroding alpha opportunities. The pandemic was a catalyst of this technological development and we expect the advancement to continue shaping the industry and fixed income markets, driving further efficiencies.

Asia’s Adoption of Fixed Income Indexing Lags

When it comes to the adoption of indexing in broader fixed income portfolios, levels vary across regions. Institutional investors in Australia and Japan have the highest proportion of indexing at >30% while European and US investors are at around 15%, with the rest of Asia lagging at <5% (Figure 2).

Figure 2: Index Investment as Percentage of Total Fixed Income AuM

Three of the key drivers for a shift towards indexing we see are fees, tracking error budgeting, and a disaggregation in fixed income exposures.

In Australia, fees and tracking error sensitivity are heightened as the regulator requires superannuation funds to disclose fees and returns against set benchmarks for comparison with peers. This has led to these funds tightening up on tracking error and fees utilizing indexing in liquid markets while generally allocating more budget to alternative investments.

In Japan, the data is skewed by one large asset owner, which has around 80% allocation to indexing across their fixed income portfolio. Given their size, indexing offers a very efficient way to gain broad exposure at scale to fixed income. However, we have also seen the adoption of a building block approach in their fixed income portfolio, combining active and indexing solutions to achieve their objectives.

Outside of the region, asset owners are utilizing indexing in various ways. Some are utilizing indexing for liquidity against their private exposure (usually high yield). Some are disaggregating their fixed income exposures to meet investment objectives such as building out portfolios for liability matching. Others are utilizing a building block approach that enables them to take a more active approach with the ability to tilt portfolios in one direction or another (e.g. taking more or less credit exposure based on return expectations).

As fixed income markets become more efficient, investors are starting to utilize a modular approach to select the most effective way, across active and index solutions, to access each fixed income market.

Active vs. Index Across Different Fixed Income Market Segments

- As we expect to see a shift towards a more building block approach across fixed income, we analyzed where investors may consider active and where they may consider indexing. Higher outperformance consistency is observed in global investment grade credit (the only market to see positive returns for median managers), emerging market debt (EMD) local currency and global high yield active managers versus the rest.

- While active strategy may generate positive excess return, the excess return drawdown is typically large during market sell-offs. Index strategies in most cases offer more stable performance across market cycles.

- On the basis of excess returns and performance persistency, investors can consider an index approach for global government and EMD hard currency segments, and an active or a hybrid approach for global investment grade credit, global high yield credit and EMD local currency segments.

When Does Active or Indexing Make Sense?

The case for index approach is strong in markets where active managers have difficulties generating adequately large and consistent net-of-fee alpha. Index strategies tend to thrive in highly efficient markets in which indexing costs are low or where effective processes to reduce indexing costs can be achieved.

In markets where sustained and sufficient alpha can still be found, an active or a hybrid approach can be considered to optimize risk-adjusted returns. For high alpha seekers, it makes sense to concentrate on a small number of active managers. However, choosing a persistent top-performing manager may be difficult and stability of excess return can be challenging.

Complementing active managers with index managers can help to satisfy asset allocators’ goals of portfolio diversification and enhancing performance stability, especially during market sell-offs. A hybrid approach can also enhance the flexibility of the portfolio with the addition of the index sleeve allowing investors to rebalance more efficiently.

Active vs. Indexing Performance Across Different Fixed Income Building Blocks

If we are going to see a shift towards a building block approach in fixed income portfolios, how should investors think about the mix of indexing and active in their portfolios? While we are seeing some global allocators taking a very granular approach by segment, region and duration, we have opted to conduct an empirical analysis on some of the more common segments in portfolios.

For each block, we examine and evaluate the following over the 10-year period from July 2013 to June 2023:

- The net-of-fees performances of median managers’ excess returns versus manager preferred benchmarks. We examine and compare statistical measures of active and index managers.

- The performance persistency of top and outperforming active managers. We group strategies based on lagged 3-year returns and examine the association between past and future performance.

Global Government: Highly Efficient Markets Suggest an Index Approach

We would expect the global government bond segment to be a highly efficient market in the fixed income universe, typically exhibiting high liquidity and low idiosyncratic risks. As seen in Figure 3 below, net-of-fee excess return performance for median active global government bond managers was similar to that of median index managers. The monthly excess returns of median active managers were negatively skewed (i.e. a tail to the left), with significant underperformance in periods of market stress, such as in early 2016 and the 2020 Covid periods. By comparison, median index managers demonstrated more stable returns with lower drawdown.

Figure 3: Performance Overview of Median Active and Index Global Government Managers

We also found that it was difficult to identify consistent top-performing funds and persistent outperformers. Using the 3-year evaluation period, the rolling average percentage of top quartile (Q1) funds staying in the top quartile for the next period was only 33%. Top quartile funds also failed to show persistently higher average excess returns versus funds in other quartiles (Figure 4).

Figure 4: Performance Persistency Overview of Active Global Government Managers

Over the 10-year period, not only did median active funds fail to generate positive average excess returns, but monthly excess returns also exhibited sizeable dispersion and were negatively skewed with large drawdowns in bear markets. Looking at individual active manager performance, excess returns lacked persistency. Therefore, investors should consider index solutions for this building block.

Global Investment Grade Credit: An Active or Hybrid Approach Can be Considered

Compared to global government bonds, the global investment grade credit universe is more diversified across sectors, issuers, credit quality, seniority and liquidity. We would expect these additional dimensions of risks to create alpha opportunities for active managers. In Figure 5 shows, the net-of-fee annualized excess return of median active managers was positive, while median index manager returns were negative. Both median active and index managers’ excess returns were slightly negatively skewed. Maximum drawdown performance was better for both active and index global investment grade managers relative to global government bond managers.

Figure 5: Performance Overview of Median Active and Index Global Credit Managers

There is a decent persistence in the performance of active managers. On a rolling 3-year basis, the percentage of top quartile managers staying in the quartile was 40%, with outperforming active managers continuing to beat their benchmark over the next three years (77%). On a rolling basis, top quartile managers ranked by past 3-year performance had better excess returns versus bottom quartiles in the next 3-year period, and performance was still positive for the second and third quartiles, showing quite positive performance for all but the bottom quartile (Figure 6).

Figure 6: Performance Persistency Overview of Active Global Credit Managers

This suggests that investors can consider taking an active approach to this building block. But we would argue that a hybrid approach (a mix of active and indexing) can also be considered, as the median index manager exhibited higher excess return stability across market cycles with lower drawdowns providing a measure of risk diversification.

Global High Yield Credit: An Active or Hybrid Approach can be Considered

Global high yield, like global investment grade credit, exhibits dimensions of risks that can present market inefficiencies, preventing potential excess return opportunities. However, in high yield markets, transaction costs are typically higher with greater idiosyncratic risks, given the higher risk of default. Quite often, active managers are underweight credit beta with outperformance driven more by avoiding defaults.

In our analysis, median active funds failed to beat the benchmark but did outperform median passive funds. The distribution of median active excess return has a negative skew, but with a thinner tail versus normal distribution data. Maximum drawdown for median active managers was slightly worse than index managers but not dramatically so, which we would expect given the generally more risk-averse tilt active managers tend to take. Passive managers performed more consistently, exhibiting lower drawdowns, but lagged the benchmark after fees over the long run.

Figure 7: Performance Overview of Median Active and Index Global High Yield Managers

Similar to global investment grade credit, we observe a decent persistence in performance of active managers, particularly in top players. On a rolling 3-year basis, the percentage of top quartile managers staying in the quartile was 41%, with outperforming active managers beating their benchmark regularly (60%). While top quartile managers demonstrated fairly steady outperformance versus their benchmarks, bottom managers underperformed significantly. The average rolling 3-year annualized excess return of first quartile active managers (ranked by previous 3-year performance) was positive, net of fees, with the other quartiles having negative returns.

Figure 8: Performance Persistency Overview of Active Global High Yield Managers

Average 3Y Excess Return of Active Managers by Quartiles of Previous 3Y Performance

On this basis, an active solution could be utilized in this building block. However, this requires the careful picking of top-performing managers. For risk diversification, a hybrid approach should be explored.

EM Hard Currency Debt: Difficulties in Idiosyncratic Risk Management Suggest an Index Approach

Emerging Market Hard Currency (HC) offers alpha opportunities isolated from developed market fixed income. The information asymmetry, country-specific risks, and long periods of unhinged volatility is the right mix for active management appetite. However, historically, active management has not been able to take advantage of the idiosyncrasies. Primarily, the single country risks are pervasive and difficult to manage for this category. Geopolitical risks can occur quickly and undermine fundamentals. Operational challenges add to the complexity of the investment opportunity.

Median active managers in this segment had the worst annualized excess return (-0.53%) in the 10-year period versus all other segments with a negative skew and a large maximum drawdown (Figure 9). Active managers in this space are often overweight risk with higher-yielding securities to outperform the benchmark. This can lead to crowding and high concentrations in risk exposures, which can result in the highly cyclical performance of active managers as shown in the analysis.

Meanwhile, with improvements in liquidity throughout the years, index managers were able to track the index return more effectively and even deliver incremental value via security selection from the sampling process with a positive skew and relatively stable performance.

Figure 9: Performance Overview of Median Active and Index EMD Hard Currency Managers

The performance persistency of active managers has been weak. Top quartile managers do not exhibit high continuity of outperformance while bottom ranked managers on average have consistently underperformed.

Figure 10: Performance Persistency Overview of Active EMD Hard Currency Managers

Average 3Y Excess Return of Active Managers by Quartiles of Previous 3Y Performance

In the period examined, median active funds failed to beat the benchmark and lagged index managers in both return and risk metrics while performance persistency was poor. Therefore, investors could consider index solutions for this building block

EM Local Currency Debt: An Active or Hybrid Approach Can be Considered

Emerging Market Local Currency (LC) debt is a more currency-volatile version of Emerging Market Debt investment. The return drivers for hard and local currency are different. Active investment of emerging market currencies can potentially enhance returns, but currencies are highly volatile and vary considerably by country. Although the average bond quality of local currency debts is generally superior, the scope of investment is smaller than the EM hard currency debt universe (typically less than 20 for the LC indices and 60+ countries for the hard currency (HC) indices). This makes it a challenging category for both active and index managers with the drag from tax and the narrow investment scope.

In our analysis, the median active fund manager’s excess returns are flat relative to their benchmark. The monthly excess returns are positively skewed but exhibit large outliers and fatter tails. However, it is noteworthy that there was an unprecedented outperformance (+1.89% excess return) of median active managers in February 2022 due to the Russian-Ukraine War, which is unrealistic to expect under normal market circumstances. This unusual geopolitical event has uplifted the average annualized excess return by 0.20% and shifted the skewness of the median active managers performance. After the removal of impact from this one-off event, the annualized return of median active managers still shows an advantage, but to a lesser extent, over median index managers. Of all the different segments analyzed, this is the only case where the median active manager saw lower maximum drawdowns compared to the median index manager (although only modestly lower in this case).

Figure 11: Performance Overview of Median Active and Index EMD Local Currency Managers

Looking at the stability of performance, there has been a decent persistence in performance of active managers. As shown below in Figure 12, the average percentage of first quarter funds remaining as top quartile was about 42% while the outperforming funds continuing to outperform was slightly higher at 58%. Top quartile managers also generally showed higher performance versus bottom quartile managers.

Figure 12: Performance Persistency Overview of Active EMD Local Currency Managers

Average 3Y Excess Return of Active Managers by Quartiles of Previous 3Y Performance

Based on our analysis, returns were better for the median active manager, and top quartile manager performance consistency was relatively high. While bottom quartile manager performance was weaker, after-fee returns tended to be on par or somewhat better than the median index manager. This suggests that investors can consider taking an active approach for this building block. However, we do note that over longer-term time horizons, the performance of active managers is less consistent under normal market circumstances. Therefore for risk diversification, a hybrid approach can be explored.

Blending Index and Active to Improve Returns and/or Portfolio Efficiency

- Hiring active managers to run global aggregate bond mandates is a popular approach to investing in global fixed income across Asia. This approach has largely been justified by performance. However, the outperformance has tended to be driven by excess exposure to credit risk, which has led to underperformance during market sell-offs.

- Using a building block approach, we show that by combining a portfolio of global government bond index managers and active global investment grade bond managers, investors can improve on performance while reducing risk, compared to using only active global aggregate managers.

- To show the benefits of combining active and index exposures for a broader fixed income portfolio allocation, we compare an all active versus a blended approach that uses active for global investment grade credit, global high yield and EMD LC, and index for global government bond and EMD HC blocks. While returns were similar, realized tracking error and drawdown were significantly lower for the combined portfolio.

Replicating the Global Aggregate Index using Index Global Government and Active Global Credit Enhances Return/Risk Metrics

Hiring active managers to run global aggregate bond mandates is a popular approach to investing in global fixed income across Asia. This approach has largely been justified by performance, although recently performance has been somewhat challenged. Using the same analysis in the last section, we found that median active global aggregate managers generated a positive annualized excess return of 0.12% relative to their benchmark, although the distribution was skewed to the negative side with a fat tail.

Figure 13: Performance Overview of Median Active and Index Global Aggregate Managers

One of the main reasons for this outperformance is that many of these active managers take out-of-benchmark credit exposures in order to generate alpha. This can be evidenced by the average holding data of active managers. Over the past 10 years, the monthly average Treasury exposure of median active global aggregate managers was 10% lower than their benchmark (Figure 13), while active manager beta is higher (Figure 14). The higher exposure to (credit) risk has led to even higher average bear market beta compared to bull market beta. For example, median active global aggregate managers underperformed the benchmark by 3.09% during the first quarter of 2020 (Covid period) while median index manager performance was about flat (-0.03%).

Figure 14: Average Monthly Weight (%) of Government Bonds, Global Agg Median Active and Index Managers, 7/2013-6/2023

Figure 15: Average Beta in Bull & Bear Markets, Global Agg Median Active Managers, 7/2013-6/2023

In an earlier paper , we showed that the performance of global aggregate active managers can be replicated using 100% indexing by increasing the credit tilt with around 88% global aggregate and 12% global high yield index exposure (on a hedged basis), and that by taking a hybrid approach (using a mix of global aggregate active and indexing), investors can improve the return/risk in a multi-asset portfolio. But what if investors can take more credit risk to improve returns while reducing tracking error and drawdowns?

In Figure 16 below, using our building block approach, we compare global aggregate active manager performance with an equal weighted portfolio of median index global treasury managers and median active global investment grade credit managers (50/50). Our mix of index global government and active global investment grade credit managers generated an additional 5 basis points (bps) in alpha per year after fees with considerably lower tracking error and drawdown. A combination of 38.5% index global government and 61.5% active global investment grade credit (providing the same level of tracking error to the median active global aggregate managers) as shown in the same chart, offered a 29bps pick-up in alpha per annum after fees, significantly improving the information ratio while still reducing the drawdown.

Figure 16: Return and Risk Comparison: Active Global Aggregate Managers Versus Active Credit/Indexing Treasury Blends

Fixed Income Indexing: Additive in a Global Multi-Asset Portfolio March 2021

The Benefits of a Blended Approach: Lowers Risks without Sacrificing Returns

To show the benefits of combining active and index exposures for a broader fixed income portfolio allocation, we constructed two portfolios (Figure 17). Portfolio 1 (P1) uses only active building blocks while Portfolio 2 (P2) uses a mix of active and indexing based on our earlier analysis across segments. While we could take a hybrid approach to some segments (global investment grade credit, global high yield and EMD LC), for simplicity of analysis we only use either active or indexing for each segment.

Figure 17: Overview of Broad Fixed Income Portfolio Construction Breakdown

Our analysis shows that while both portfolios generated similar excess returns, the realized tracking error and drawdown for P2 is around a third of the levels for P1. Using building blocks optimized for the investment approach for each segment allows investors to pick and choose the sectors where risks can be best rewarded in order to improve portfolio efficiency and risk without sacrificing returns.

Figure 18: Summary of P1 & P2 Performance Comparison, 7/2013-6/2023

Indexed Performance Comparison

Conclusion

As our analysis in this paper has demonstrated, there are merits to incorporating indexed strategies in fixed income portfolios. The lack of consistency in the performance of actively managed strategies, where most managers have typically failed to beat their benchmark in consecutive years, underpins the argument for diversifying into indexed strategies. However, it is not a case of either/or.

Technological advancements across fixed income markets are providing investors greater pricing transparency and more efficient access to market liquidity, enabling greater precision and efficiency in fixed income management while potentially eroding traditional alpha opportunities. This has been a contributor to the shift towards indexing. Index strategies may be considered where active managers have difficulties generating adequately large and consistent net-of-fee alpha. In markets where sustained and sufficient alpha can still be found, an active or a hybrid approach can be considered to optimize risk-adjusted returns.

As a result, investors are now rethinking how to construct their portfolios optimally to seek balance among return, risk, reliability and cost factors. They are starting to take a building block approach to fixed income portfolio construction in order to select the most effective way to access each fixed income segment in order to achieve their objectives. Our findings show that utilizing a mix of active and indexing can often create better, more consistent return outcomes across fixed income portfolios while reducing overall portfolio risk.