Understanding markets in the new world order: A geopolitical framework for investors

Geopolitics and its impact on markets have been increasingly in focus over the past year, as trade policy, industrial policy, and military conflicts have dominated headlines. Even before that, the Russia–Ukraine war (2022–present), the Israel–Gaza conflict (2023–present), and rising U.S.–China tensions were among many investors’ top concerns. At the same time, a growing body of geopolitics-related investment research has emerged, along with a range of new geopolitical risk indices and indicators. But do these actually matter for most investors? Which geopolitical forces move markets, and what should investors be paying attention to?

The short answer is: it depends on the time horizon. For hedge funds and other short-term arbitrageurs responding to overnight moves in markets and currencies, day-to-day developments in the Middle East can matter. For long-term investors, however, we generally advise focusing on important structural shifts rather than short-term, impermanent noise.

What follows is an excerpt of the full white paper. Download the full piece here.

Conflict in the current decade

In the history of geopolitics, we believe the 2020s marks a crucial structural break. In this paper, we go beyond single conflicts or individual headlines, and identify the long-term forces we believe investors should pay attention to.

Key takeaways for our long-term geopolitical views include:

- We are moving away from familiar territory and entering a new world order, one with important implications for the growth-inflation mix, and for long-term investment outcomes.

- The continued fragmentation of the global order damages the supply side of the global economy.

- The resulting stag-flationary impulses require repeated fiscal interventions by governments to mitigate their effects, with high sovereign debt burdens eventually creating a drag on macroeconomic performance as borrowing costs creep up over time.

Why it’s different now

This decade differs fundamentally from recent history, and therefore, a new framework for geopolitical risk is required (Figure 1).

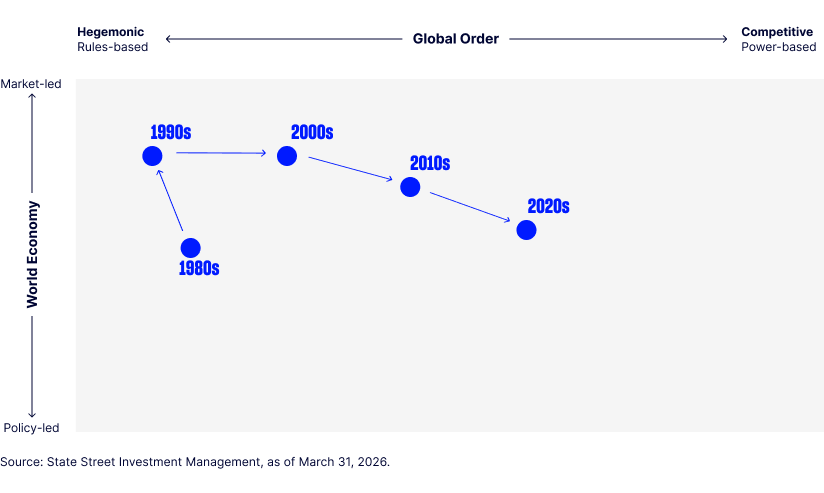

Figure 1: The 2020s are unlike other decades and trending away from familiar territory

Figure 1 illustrates how the world has evolved in recent decades. It places each decade along two intersecting axes: a vertical axis running from market led (top) to policy led (bottom), and a horizontal axis that moves from a hegemonic, rules based global order on the left to a competitive, power-based order on the right. The historical trajectory depicted—1980s, 1990s, 2000s, 2010s, and finally the 2020s—moves diagonally downwards and rightwards. This path indicates a gradual but persistent weakening of the global rules based order and a simultaneous increase in the role of domestic policy intervention relative to market forces.

Historical evolution, by decade

In the 1980s and 1990s, the global environment was broadly characterised by U.S.-led hegemony, expanding trade liberalization, and deepening globalization. Markets largely dictated outcomes, capital moved across borders with increasing ease, and multilateral institutions—from the WTO to the IMF—played a stabilizing and rule setting role. Figure 1 shows these decades in the upper left quadrant, signalling an environment in which markets, rather than states, set the rhythm of economic growth, and where the global order was coherent, predictable, and anchored in shared rules. This backdrop optimally plays to a classic 60-40 portfolio, as market prices maximise efficiency, correlations are consistent and known, and conventional portfolio hedges worked as expected.

As we progressed to the 2000s and 2010s, we entered a period that is represented by the markers shifting modestly downward and rightward. The 9/11 terror attacks and the 2008 financial crisis were accelerants of this shift. The G7 governments expanded interventionist policies, particularly in monetary and regulatory spheres, while China’s economic ascent challenged the Washington consensus. Consequently, while globalization continued, it no longer deepened at the same pace, and the consensus around a rules based order began to fray.

The 2020s started with the Covid-19 pandemic, exacerbating the need for state involvement in the economy and the divergence of experiences for China and G7 economies.

The current decade marks a decisive shift toward a policy-led global macro regime embedded within a competitive, power-based global order.

One feature of this new world is the formation of geopolitical blocs and the return of proxy wars, as states prioritize supply chain security, technological sovereignty, and strategic autonomy over global integration. Another is the erosion of global rules, treaties, and organizations, such as the declining effectiveness of the WTO and the reduced authority of judicial or arbitrational bodies like the International Court of Justice (ICJ). These changes reflect not only geopolitical rivalry, but also ideological divergence, economic nationalism, and regional re-alignment.