Systematic Equity – Active Monthly Short shocks, longer echoes

The outbreak of war in the Middle East sparked a reaction from global equity markets that could be viewed as one of controlled retracement. But as events in Iran have showed, how war evolves and how markets respond do not always follow an expected pattern: the dispersion of outcomes can be wide. This month, we look behind the headline moves and interrogate equity performance since the onset of hostilities; we also compare and contrast the current environment with the politically driven market adjustment observed in April 2025.

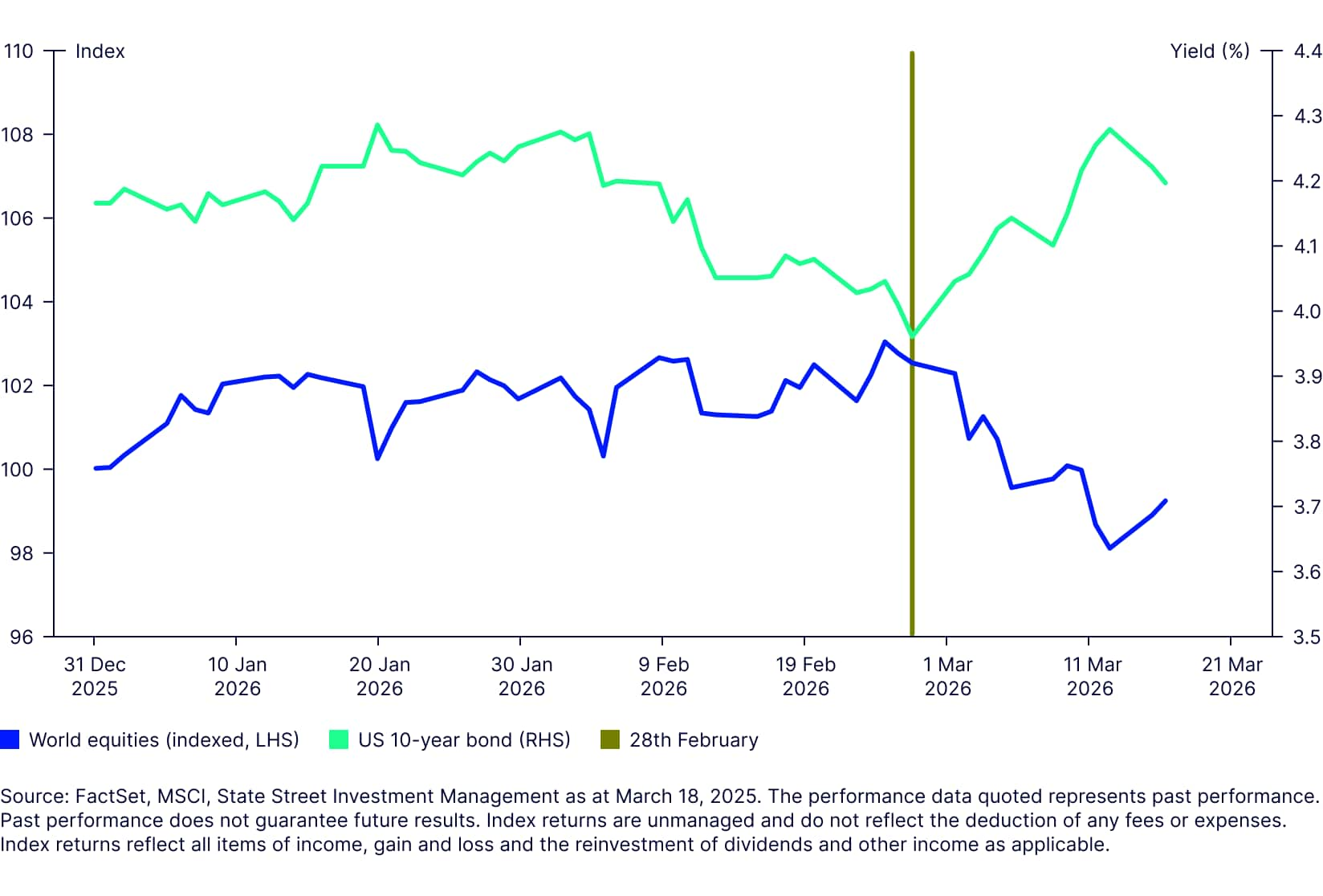

The immediate market response following the attack on Iran by the US and Israel on 28 February was broadly rational. Equity markets declined as risk premia rose, before then fluctuating as the news narrative changed quickly. Arguably the most rational reaction was captured in the sharp oil price increase—the effective closure of a key global supply route through the Strait of Hormuz heightened fears around energy supply, with inflation expectations pushing modestly higher as a result. Bond yields rose in parallel, reflecting a repricing of macro and geopolitical risk. (See Figure 1).

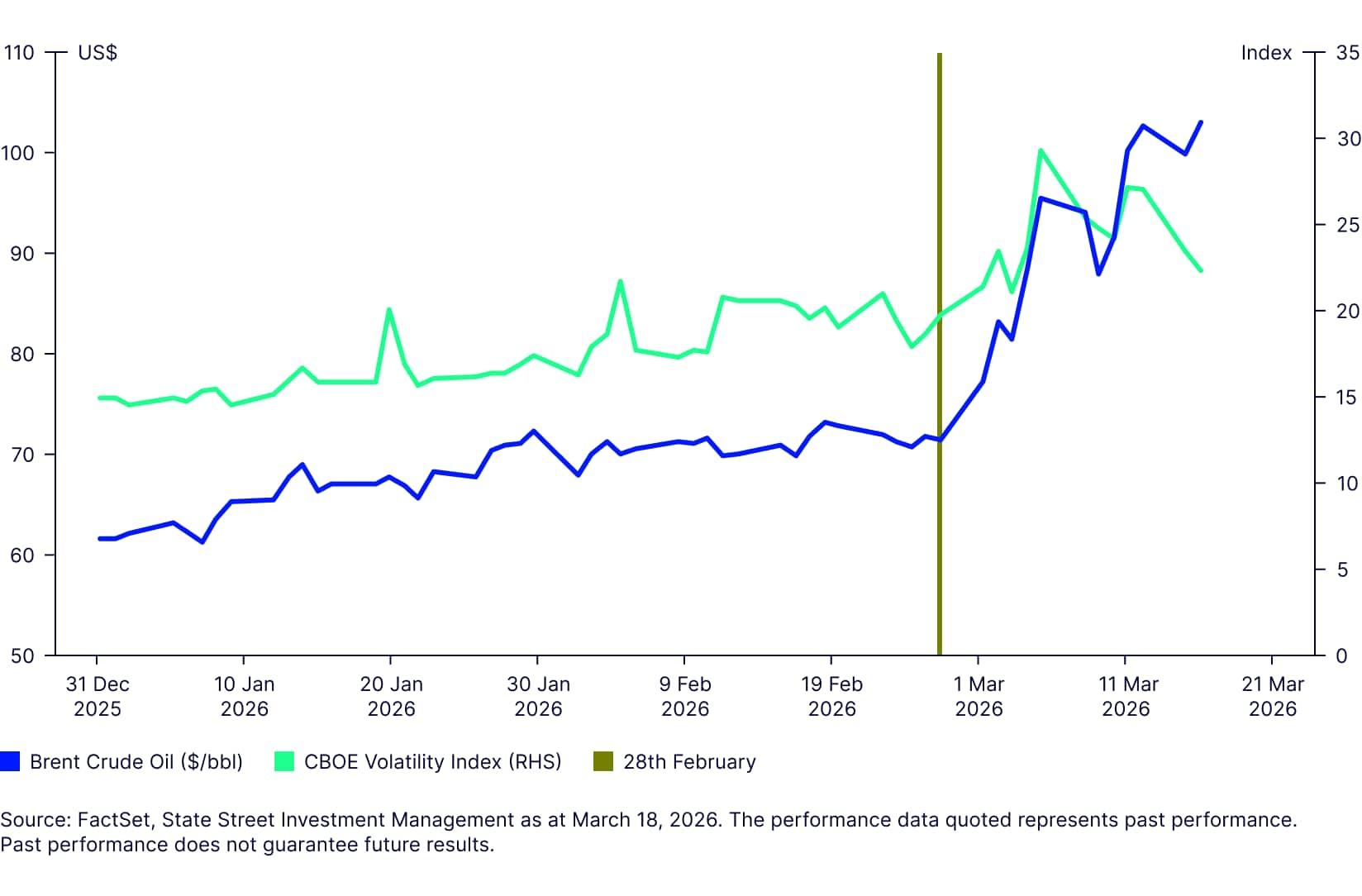

As depicted in Figure 2, market volatility also ticked higher, though the magnitude of the move was contained relative to the scale of the geopolitical shock. Energy stocks outperformed as oil prices surged above $100 per barrel, while investors reversed some recent positioning and gravitated back towards perceived safe-haven assets, including the US dollar and US equities.

From an equity market, factor, and volatility perspective, the initial effects have been directionally consistent with our expectations, but relatively muted in terms of amplitude. This reflects both the market’s increasing familiarity with geopolitical shocks, and the fact that much recent equity performance had already been driven by elevated risk concentration and extended valuations in certain segments of the market.

At the factor level, there are notable similarities between this recent drawdown and the market adjustment in April last year, when the introduction of sweeping US tariffs on global trading partners triggered a sharp but short-lived sell-off. During that episode, cheaper and more volatile stocks underperformed, while Quality 1 stocks and those exhibiting positive momentum held up relatively well (Figure 3).

During the first two months of 2026 high momentum stocks had been performing strongly, with cheaper Value names also delivering positive relative returns. Since the start of the conflict in the Middle East, however, cheaper stocks have been sold off, while Quality stocks have been rewarded—this is broadly in line with our January article where we outlined how Quality exposure can be important for navigating markets during periods of heightened uncertainty and stress. 2

Lessons from geopolitical shocks : Diversification and discipline are key

If we look back a year, the market rebound after the initial softening of the US tariff stance was led by higher volatility names, while higher quality stocks gave back some of their gains. Although there may be some common characteristics in these two environments (from April 2025 and now), we would caution that it is not wise to draw direct inference for returns.

Even in the event of a relatively swift resolution to the current conflict, the economic impacts are likely to be more persistent than those associated with the short, sharp tariff pivot. From an economic—rather than humanitarian—perspective, the key uncertainty now centres on the duration of the conflict. This will largely determine the extent to which disruptions to energy supply persist, and the knock-on effects for inflation expectations, corporate confidence, and ultimately company earnings. These are questions for which we do not yet have clear answers, and may not for some time. Even if markets were to recover back to previous levels, the path from here is unlikely to be smooth and there will be lasting impacts, both economic and political which as yet are unclear.

To invest in this environment, we believe it is critical to design a process that is explicitly long term in nature—one that can look through short-term volatility and geopolitical shocks, rather than attempting to forecast them or trade around short-term market noise. Risk management is therefore embedded in every stage of our systematic active equity process by design. The objective is not to take more risk, but to use risk more efficiently—and only where we believe it will be rewarded. Diversification plays a central role throughout the process, from signal design to portfolio construction. Our focus is on consistency and compounding: disciplined, repeatable decision-making and a collection of small, well-governed active positions, rather than large directional bets on countries or sectors that may be particularly vulnerable to geopolitical stress.

Periods of geopolitical uncertainty inevitably test investor conviction and market resilience. While the immediate market response to recent events has been relatively contained, the longer-term implications for inflation, growth, and earnings remain uncertain. In our view, this reinforces the value of a systematic, risk-aware investment approach—one that is diversified by design, grounded in robust signals, and focused on navigating evolving market conditions with discipline rather than reaction. In a world of rising risks and episodic shocks, we believe such an approach is well positioned to deliver more consistent outcomes for active equity investors over time.

To learn more about the views and investment capabilities of the Systematic Equity – Active team, please visit our website.