Investing in AI through sectors

Key takeaway: Artificial intelligence (AI) is a major transformational force reshaping the global economy, and sector investing offers a powerful, diversified way to tap into the structural growth opportunities across the economy.

Sector Research Team

Rather than thinking of AI as a single industry or tech theme, AI is proving a long-term catalyst driving enhanced productivity, innovation, and new business models across many sectors. But for investors constructing portfolios, that translates into understanding how to capture the evolving opportunity set—and across which sectors and when?

As AI’s investment potential matures beyond its pure tech beginning, investors can position for the next stage of growth by understanding how value and capital are flowing through the AI ecosystem and then positioning across multiple parts of the value chain through different sectors to capture distinct risk-adjusted return opportunities.

Why invest in AI with sectors?

The sector framework helps investors zero in on the parts of the AI opportunity where earnings growth, capital investment, and pricing power may be more durable—and where a greater and more persistent share of the AI value chain may emerge as deployment scales.

Moreover, a sector-based approach to AI investing can help investors capture growth while managing company-specific volatility and drawdown risk. Rather than trying to identify one company that will dominate a particular layer of the broader innovation cycle, investors can benefit from allocating to a group of companies through sectors that are building, enabling, and/or adopting AI—and positioning portfolios for what’s shaping up to be one of the most significant technological transformations of our time.

With AI deployment still in its early days and future winners and disruptors yet to be determined, allocating to several parts of the ecosystem across sectors can help investors position for growth while smoothing return and volatility relative to individual stock investing.

What sectors to invest in?

AI is no longer just a Technology story; it’s become a broad, multi-sector investment theme spanning:

- Core enablers and builders along today’s AI infrastructure value chain

- Early monetizers where AI is already contributing to revenue and growth

- Emerging use cases where AI is still focused on efficiency, digitization, and incremental operating improvements

Together, these categories form a framework for allocating across the AI ecosystem—spanning infrastructure buildout, near-term monetization, and longer-term adoption.

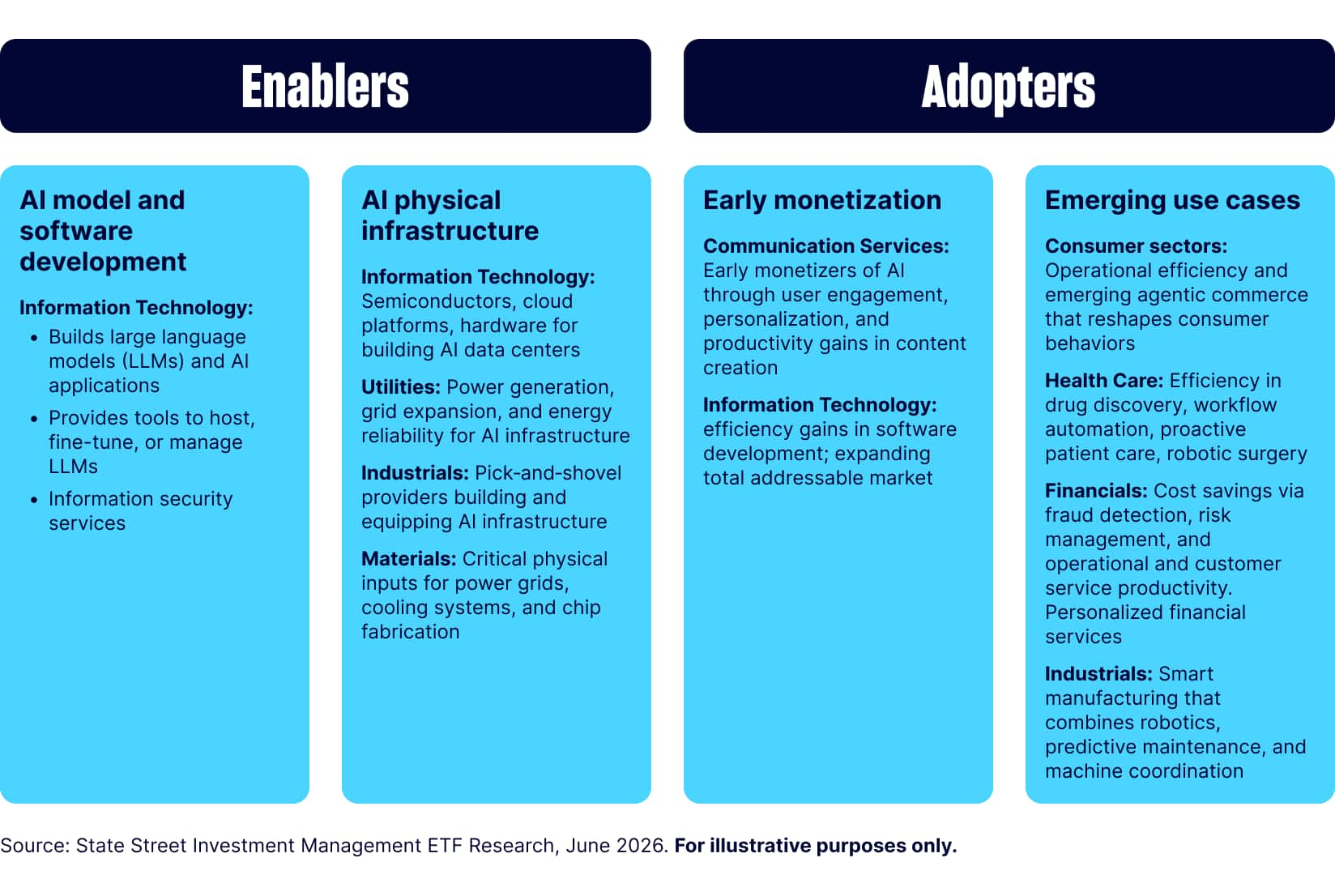

Figure 1: AI value chain

While semiconductors, technology hardware, and hyperscalers remain the most direct expressions of rising AI adoption, Communication Services companies have emerged as some of the key early monetizers integrating AI into their existing business models to improve efficiency, personalization, and advertising effectiveness.

The scale of AI capital expenditure is also creating powerful tailwinds and second-order opportunities across Utilities, Industrials, and Materials that are actively supplying the physical inputs required to build, manufacture, and support AI’s current and ongoing development at scale.

Sectors within the emerging use case category represent early AI adopters that are in a more nascent state of the transformation cycle but represent future potential for AI adoption to crystalize into revenues and investment opportunities.

Technology: The original AI enabler

Technology has been, and is likely to remain, the largest beneficiary from the AI spending boom and rising AI adoption. Building and deploying AI models requires extensive computing power and data infrastructure to meet growing demand, and companies are rapidly scaling capacity to keep pace: from semiconductors powering massive AI workloads, and cloud computing platforms delivering on-demand computing, to hardware companies that store and transmit large amounts of data. The significant increase in revenue growth and backlogs for AI cloud compute services among major hyperscalers offers clear visibility into future revenue as AI demand continues to scale.

Software is another industry that stands to benefit structurally. AI is driving efficiency gains by boosting software engineers’ productivity via coding assistance, reducing time for testing, debugging and maintenance, and accelerating product cycles. Meanwhile, the disruptive nature of AI technology may also function to expand the total addressable market for the industry by enabling new use cases, expanding product categories, and unlocking new demand. Nevertheless, capturing these new growth opportunities requires foundational transformation within the industry, such as modernizing code base, building AI-ready data infrastructure, and changing pricing models.

Communication Services: The early AI monetizers

Top companies in the Communication Services sector, particularly those in the interactive media and entertainment space, are leading early AI monetization. Social media and digital search platforms are integrating AI across existing products to enhance user experience through personalized content targeting, including improved search results and content recommendations that are increasing user engagement and driving digital advertising revenue growth.

In the first quarter of 2026, Gemini Enterprise, Alphabet’s AI-powered conversational platform for businesses, saw 40% growth quarter-over-quarter in paid monthly active users, contributing to the company’s 63% year-over-year revenue growth.1 Meanwhile, Meta Platforms noted usage of its generative AI ad creative tools that it scaled to more than 8 million advertisers, with their video generation feature seeing more than 3% higher conversion rates.2

Media and entertainment companies are also benefiting from AI-driven targeting in ad-supported subscription tiers, which offer a discount in exchange for advertisements during programming and enable personalized ads alongside greater viewer engagement. At the same time, AI is streamlining content creation through automated video editing, content generation, and enhanced 3D modeling for films and clean video games—driving meaningful cost savings and productivity gains.

Finally, Telecom companies are evolving beyond providing traditional connectivity into higher-growth, tech-enabled services. AI-native networks enable autonomous, self-optimizing systems that improve performance, automate decision-making, and unlock new enterprise and consumer applications such as distributed AI inference, IoT, and immersive experiences. Monetization is already tangible, with 67% of telecom operators reporting that AI has delivered more than a 5% increase in annual revenue.3

Utilities, Industrials, and Materials: Infrastructure enablers and second-order beneficiaries

Beyond core technology and monetization, AI is driving a large-scale physical infrastructure build-out, creating demand across multiple sectors tied to power, materials, and industrial capacity.

This phase of the AI cycle represents a shift from digital innovation to physical deployment—extending the opportunity set into sectors that may not generate AI revenue directly today but could benefit from sustained capital investment and resource demand.

Utilities: Innovating to meet AI’s grid demand

We see rising electricity demand from AI-driven data centers as a key driver of ongoing grid expansion and sustained growth in the Utilities sector. AI’s significantly higher computational density compared to traditional computing, combined with rapidly growing demand, are expected to drive US data center electricity demand to grow at a 20% annual rate through 2030.4

To meet this AI-related demand, Utility companies are increasing capital expenditures to expand generation capacity and modernize grid infrastructure. For regulated utilities, this supports rate base expansion, steady revenue growth, and ultimately higher earnings. While regulated utilities benefit through rate base growth, a tighter supply-demand balance tends to push wholesale electricity prices higher, supporting stronger revenues and profits for independent power producers, whose earnings are closely tied to market power prices.

Unlike many industries, Utilities are less likely to face structural disruption from AI, given their regulated nature and hard-to-replace, long-lived underlying physical infrastructure. However, there are concerns regarding rising residential electricity bills that are partly linked to AI-related demand. The growing narrative could serve to attract greater regulatory scrutiny that could potentially limit the sector’s profit growth compared to other less regulated AI sectors. Even so, regulated revenue frameworks, which often have mechanisms to recover costs over time, are likely to continue supporting the sector’s relatively predictable income streams.

Industrials: The “picks and shovels” of the data center build-out

Industrials represent the part of the economy that builds, moves, and maintains material inputs and turns them into finished products. Today, roughly a third of AI capital spending is flowing toward this segment of the AI buildout beyond the core semiconductors and computing hardware.5 The sector’s companies span electrical equipment, machinery, construction engineering that are positioned as one of the early “pick-and-shovel” beneficiaries in the AI infrastructure supercycle.6 Booming data center construction and the ancillary rise in demand for necessary equipment supporting power generation, transmission, and distribution, as well as advanced cooling systems and electric utility equipment is providing tailwinds for the sector.

At the same time, Industrials companies are also integrating AI into real-world systems and emerging use cases with robotics and smart manufacturing to enable more autonomous, flexible, and scalable production and operating systems. Instead of relying on fixed, pre-programed machines, companies can now use AI to help robots see, adapt, and make decisions in real time. AI also helps coordinate fleets of machines and can improve maintenance with enhanced AI driven early detection.

Over time, these smarter systems look to enhance the business and operating model by increasing output, lowering costs, reducing downtimes, and making operations more flexible and profitable, while helping manufacturers respond more quickly to changes in demand—potentially positioning the sector for greater growth beyond the initial build-out phase.

Materials: Suppliers of critical AI elements

The Materials sector also offers targeted exposure to the physical aspects required to accomplish the AI infrastructure buildout, with structurally higher demand and consumption of copper, aluminum, nickel, specialty chemicals, and engineered materials essential for power grids, cooling systems, and advanced chip fabrication. Capacity constraints and underinvestment across mining and processing facilities are amplifying the potential pricing power for producers that can meet the higher demands.

For example, AI data centers require more than three times more copper than traditional facilities, due to higher power and cooling demands.7 Even with announced investments included in supply projections, the deficit in copper could run 10 million metric tons by 2040.8 In other cases, supply is also concentrated in a few countries or tied to by-products of other mining processes. This creates a risk of ongoing shortages, which can support stronger pricing power and benefit select mining and materials companies over time.

As hyperscalers and governments accelerate CapEx to expand computing and energy networks, Materials companies are positioned to capture the volume growth and margin expansion, making the sector a key beneficiary of the AI-led manufacturing and industrial renaissance underway.

Positioning portfolios for AI’s multi-sector growth

AI’s economic impact is unlikely to be captured by a single company, technology, or moment in time. Instead, it will unfold over years as investment, adoption, disruption, and monetization ripple across the economy. A sector‑based approach allows investors to participate in this transformation by gaining exposure to the different parts of the AI value chain—from infrastructure build‑out and power supply, to early monetizers and productivity enhancers—while reducing reliance on any one business model or outcome.

Ultimately, investing in AI through sectors is about building diversified exposure across the full AI ecosystem—spanning today’s investment cycle and tomorrow’s adoption curve.