Why various market risk metrics tell different stories

The geopolitical climate has become more unstable globally, but developed markets often appear less unsettled than investors might expect. One question is: why haven’t stocks sold off more? Another is: why are volatility indicators showing different market reactions to geopolitical events? We explore this apparent disconnect through the lens of two representative indicators: the VIX index, a measure of US market volatility, and the GPR index, a measure of geopolitical risk.

Market reactions in question

The start of the year has been marked by a series of significant geopolitical events:

- January 3, 2026: The kidnapping of Venezuelan President Nicolas Maduro.

- January 17, 2026: President Trump announces a 10% tariff on eight EU countries due to their lack of support for US control of Greenland (later reversed).

- February 17, 2026: The impeachment of President Jose Jeri of Peru.

- February 28, 2026: The Iran war begins following months of escalating violence against protesters.

Despite the severity of these developments, the initial reaction in US financial markets has been surprisingly muted. Only the onset of the Iran war triggered a market response comparable to that seen at the start of the Russia–Ukraine conflict in 2022.

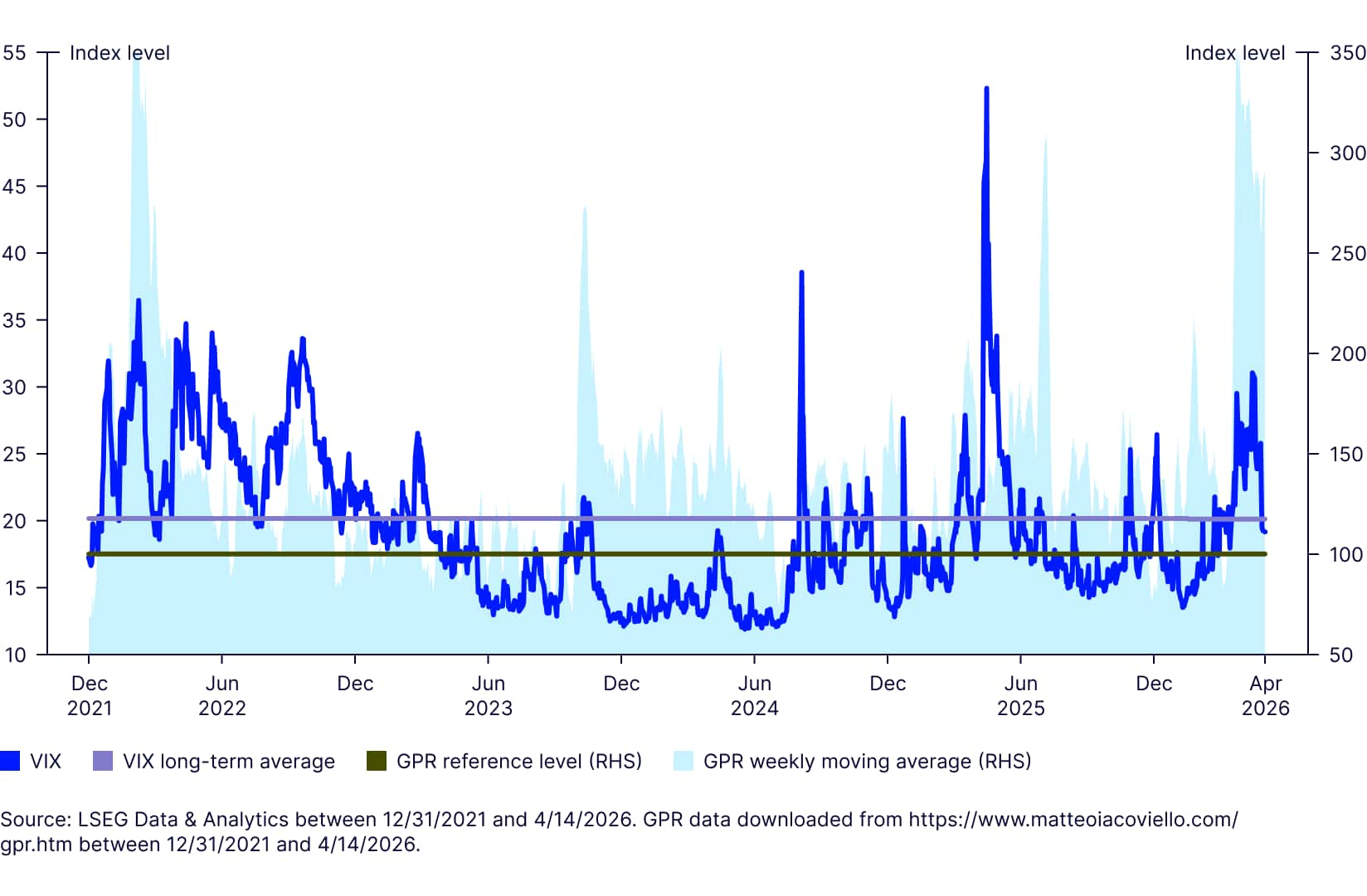

The VIX Volatility Index, often referred to as the “fear index,” remained below its long term average through most of the start of the year and only showed a meaningful reaction in early March as the Iran conflict escalated. In contrast, the Geopolitical Risk (GPR) Index responded to each of the events listed above. It reached a local peak on January 8, 2026, following President Trump’s renewed and more explicit ambitions regarding Greenland, and then climbed to a new high one week into the Iran invasion. This divergence raises an important question: why does the VIX—the US equity volatility index—not necessarily move in tandem with rising geopolitical risk?

Defining the risk indices

The standard reference index for geopolitical risk is the GPR, developed by two researchers at the Federal Reserve Bank.1 The VIX index, by contrast, is based on the implied volatility of the S&P 500 Index. The correlation between the VIX index and the GPR index appears low (Figure 1).

In this piece, we take a closer look at their dynamics, as well as those of the Trade Policy Uncertainty (TPU) index, in the context of historical events.

Figure 1: The VIX index and the GPR index do not appear to move in tandem.

The GPR Index: Broad, but timed on the news cycle

The researchers who created the GPR index started with a definition of what constitutes geopolitical risk. Since then, the GPR index has been used in many studies2 that examine geopolitical risk as a source of systemic risk.

The GPR is a media frequency (or density) index. It is based on the density of keyword counts (for example, “terrorism” or “war”) in Western newspapers (such as the Herald Tribune or the Financial Times). As a result, it is best suited to events that receive coverage in those outlets. We note that country-specific GPR indices are now also available.

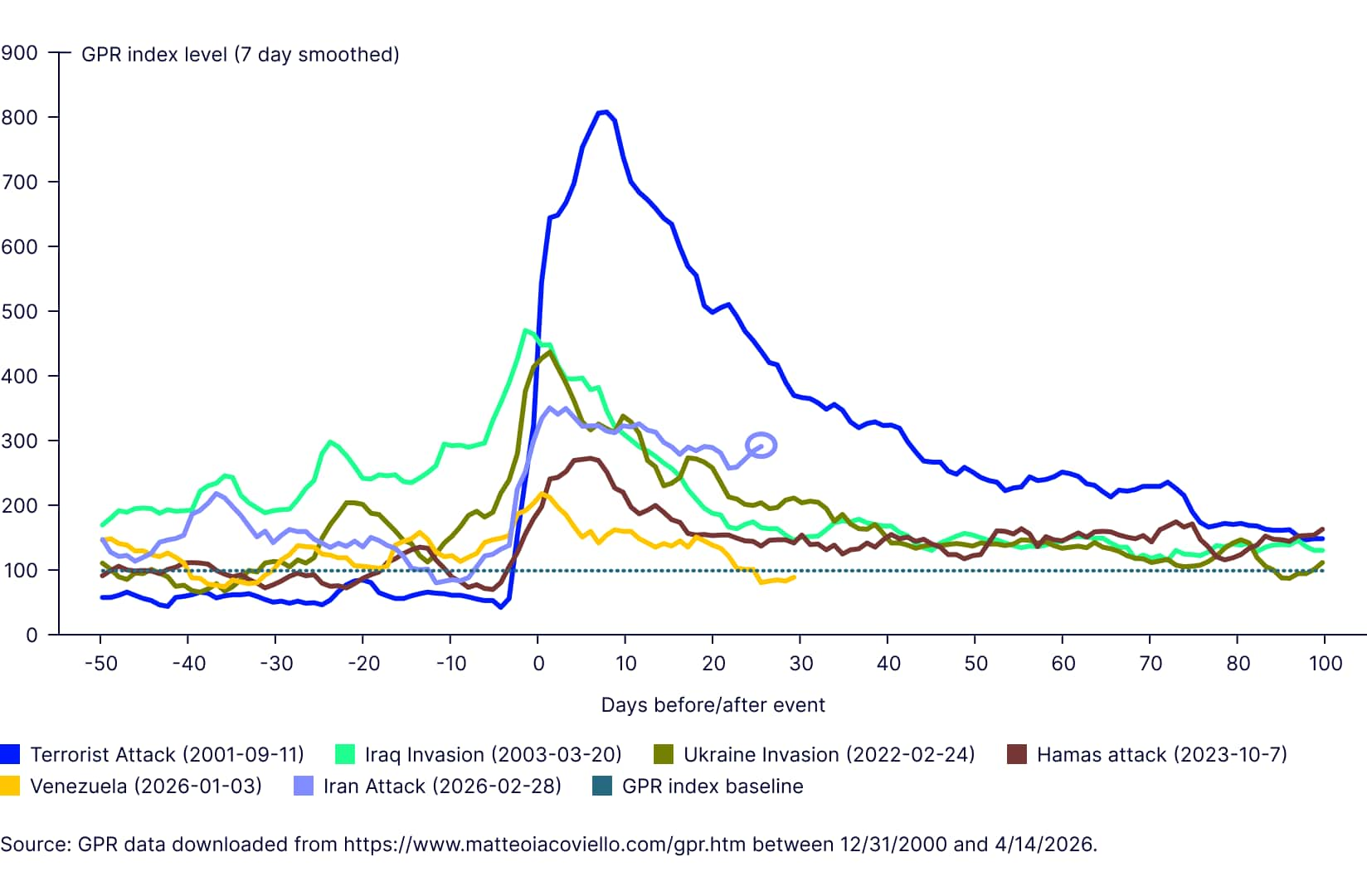

The GPR index tends to spike when there is a threat of—or an actual—geopolitical event anywhere in the world. In that sense, it is a practical, broad-based indicator. However, the GPR index is not designed to track the ongoing evolution or broadening of a geopolitical event. As Figures 2 and 3 show, an initial event generates a surge in headlines that pushes the GPR index higher, but the index often falls back as news flow declines. However, that does not mean the underlying threat has disappeared. For example:

- Israel-Hamas. The GPR index peaked shortly after the Hamas attack on Israel on October 7, 2023, but it declined after that—even though the conflict between Israel and Gaza remains unresolved, despite a U.S.-brokered ceasefire that took effect in November 2025.

- Russia-Ukraine. Russia’s invasion of Ukraine led to a peak in the GPR index in early 2022, but the GPR normalized shortly thereafter. The conflict, however, broadened into developed markets as Russia cut off gas supplies to Western Europe—contributing to higher inflation, falling European equity markets, and falling bond prices (Figures 2 and 3).

- Iran-US. In the case of the Iran conflict, elevated geopolitical risk appears somewhat more persistent, reflecting President Trump’s shifting stance,3 and potentially significant consequences if the Strait of Hormuz were to remain closed for an extended period.4

The GPR index is a useful tool for identifying threats or the start of a geopolitical event. Subsequent systemic developments—and their transmission into developed markets—can take time, and may not be captured by the GPR index.

Figure 2. The GPR Index may normalize before conflicts resolve.

The VIX Index has the pulse of US markets

The VIX index reflects the implied volatility of short-dated put and call options on the S&P 500 index.5 A sudden shock to US markets can cause the VIX to jump as the cost of insurance against price volatility rises. Once markets bottom, the VIX typically declines and markets can recover as bargain hunters move in.

We point to two recent historical events with notable differences in the way the VIX and GPR reacted:

Venezuela.

- The VIX did not react.

- The GPR index reacted immediately, signaling a meaningful rise in geopolitical uncertainty.

This divergence can be partly explained by the US’ trading position. The US economy does not depend much on Venezuelan oil, and neither does Europe. Moreover, the US has been a net oil and petroleum products exporter since 2019,6 which partly explains why the VIX did not spike in response to this event.

Iran.

- As with Russia’s invasion of Ukraine, the VIX did react at the start of the Iran war.

- The GPR index did initially react, flagging the geopolitical event.

Even though the US has reduced Middle East oil and gas exposure, this is not the case for Europe and the rest of the world. This has driven up global oil prices, leading to economic and inflation uncertainty, and pushing up the VIX (Figure 4).

The TPU index is a better fit for trade wars

Markets reacted strongly to Trump’s Liberation Day tariff announcements in April 2025, which were larger than expected and primarily aimed at China. Fears of a global trade war drove US markets lower and pushed the VIX index higher. Both the TPU index and the VIX index reacted to Trump’s tariff threats over Greenland (Figure 5). Meanwhile, the GPR index did not react to the tariff or Greenland headlines because the word “tariff” is not included in the keyword list used to construct the index.

The concern was that tariffs create economic uncertainty, although their impact on inflation is not clearly established.7 As a result, the same Fed researchers who created the GPR constructed the Trade Policy Uncertainty index (TPU index), which explicitly includes the word “tariff.” 8

The bottom line

The GPR index and the VIX index may not necessarily spike at the same time—unless a geopolitical event directly affects US markets. The 9/11 terrorist attacks in 2001 is one example. Otherwise, there is no reason to expect a synchronized shock: a geopolitical event in a distant region may take time to reach the US market as a whole, or it may simply be less relevant. By the time broader effects emerge, markets may have already adjusted so no immediate shock occurs in the US, and the VIX shows little movement.

Tariffs are another story. Tariffs can create economic uncertainty that affects companies’ expected performance, prompting reactions in the S&P 500 and, in turn, the VIX. This VIX move is not captured by the GPR index, but it is reflected in the TPU index.

Ultimately, the VIX, GPR, and TPU are built from different inputs and methodologies, and they are designed to capture different channels of risk; near-term US equity volatility (VIX); headline-driven geopolitical stress (GPR); or trade-policy uncertainty (TPU). Because these measures will not always move together, investors should be thoughtful about how they interpret and integrate them into portfolio risk models, including how each index maps to exposures and allocations across regions.