How the Iran War could impact Australia’s infrastructure

Australia faces a meaningful risk of a prolonged inflationary impact stemming from the conflict in the Middle East. What was previously a tail risk is morphing into a central case with the potential for demand destruction. While our base case remains a ceasefire by end April, we believe markets continue to underprice the risk of a prolonged conflict and a larger energy shock. Given Australia’s capacity constraints and its unique economic structure, the risk is that inflationary pressures spill into broader secondary effects. These second order effects could be far more damaging to growth than the initial petrol price shock.

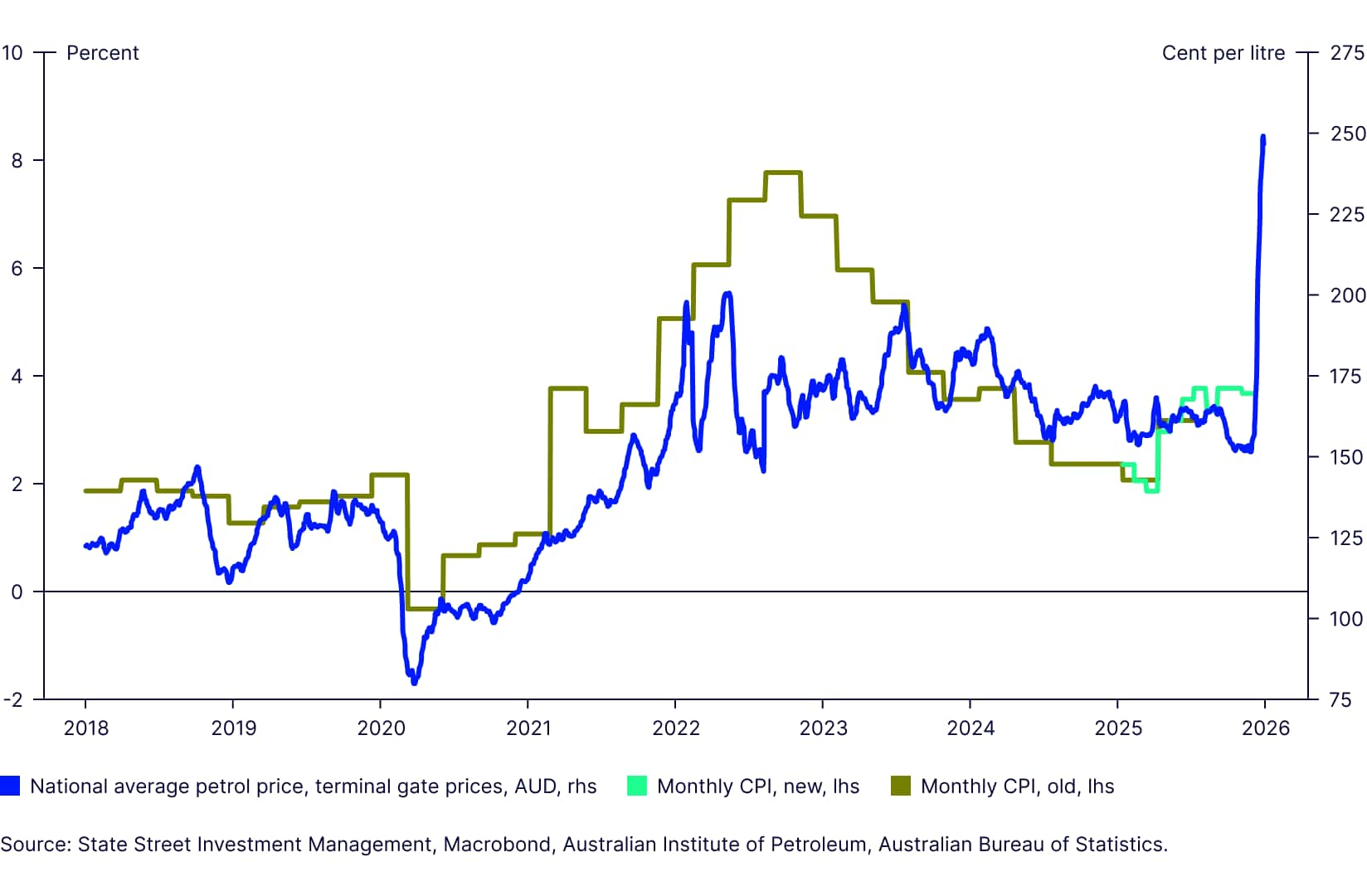

Treasury modelled the impact of two cases –if oil stays at US$100 for H1 2026 and if it hits US$120 and stays there for three years. Treasurer Jim Chalmers announced that the updated models as of March 19 indicated that the war could add between 0.5 to 1.25% to headline inflation and may subtract between 0.2 to 0.6% off GDP growth.1 This is the exact outcome we fear for Australia. As such, fuel prices at the pump in Australia have spiked considerably more than its peer group (Figure 1).

Against this backdrop, the Reserve Bank of Australia’s (RBA) back to back rate hikes look appropriately proactive, even as most global peers treaded cautiously in March. The risk now is that a rate hike hat trick comes into play in May, with the possibility of further hikes should the conflict escalate or inflation risks intensify. Even if the Iran war ends in the short-term as our base case, inflation risks still remain front and centre for Australia.

Figure 2: Upside risks for Australia’s Inflation

One mitigant should be LNG; Australia should benefit from LNG disruptions in the Middle East through increased demand for its gas exports. So far however, the benefits are running via higher prices and unsurprisingly not through expansion of volumes, which means that these benefits may not be durable. Natural gas production is dominated by offshore Western Australia and Queensland coal seam gas, but with export plants running near capacity and limited pipeline and storage flexibility, the current supply shock underscores the need for sustained investment in infrastructure, which is paramount for Australia’s long-term prosperity.

Data from the Institute for Energy Economics and Financial Analysis shows that Australia’s LNG facilities have been operating above 90% for several years, leaving little headroom to raise exports.2 Pipeline constraints were acknowledged by the International Energy Agency and the ACCC Gas Inquiry in September 2025.3 More worryingly, the ACCC warns of ‘structural shortfalls from 2028 without new infrastructure and upstream investment.4 Even the Government Gas Market Review from December 2025 identified bottlenecks in transport capacity.5

These issues circle back to the problem that we have consistently spoke about – the lack of sufficient investments, prima facie due to high interest rates and a shortage of skilled labor.

Infrastructure needs

The Middle East conflict could exacerbate Australia’s already deep seated structural challenges. Weak productivity growth has constrained living standards over time and limits the scope for sustained real wage gains without adding inflationary pressure.6 At the same time, persistent shortages of skilled labour, subdued wage growth, deteriorating housing affordability, and infrastructure gaps have dominated successive policy cycles. These challenges are not independent. Rather, they reinforce one another, leaving the economy more vulnerable to external shocks.

Infrastructure sits at the centre of this nexus and is arguably the most critical constraint. Conventional macroeconomic theory highlights infrastructure as a key enabler of productivity, by raising capital intensity, improving connectivity, and lowering economy wide costs. In practice, infrastructure shortfalls amplify labour market frictions by limiting worker mobility, worsen housing affordability by delaying enabling works, and entrench weak productivity and wage outcomes by keeping transport, energy, and logistics costs elevated. These issues do not simply coexist with Australia’s long standing economic problems, they actively magnify them.7

Australia has historically benefited from strong public support for economically significant infrastructure projects, which has helped mitigate some of these pressures. This institutional strength remains visible today. The government’s framework for identifying and supporting priority projects is well established, with 27 Major Projects given the Status (MPS) currently. These projects span capital expenditures ranging from roughly A$50 million to as much as A$60 billion with well defined timelines but many are facing delays.

Australia is also recognized for its detailed and rigorous approach to project preparation, ranking ninth globally in international assessments supported by the World Bank, while in select cases demonstrating an ability to expedite approval processes. Against this backdrop, any external shock that raises costs, tightens capacity, or delays execution risks compounding Australia’s structural challenges rather than alleviating them.

Infrastructure Australia, a federal advisory body, identified 136 pressing challenges over the next 15 years across various sectors in 2019.8 which are likely accentuated by capacity constraints and higher interest rates.

Furthermore, Australia’s population estimated to rise by 12 million people over the next 25 years. Given ongoing housing industry cost spirals and affordability issues, building and financing housing and infrastructure needs will be an enormous challenge. Such projects are gaining attention from policymakers, with the government committed to a five-year Major Public Infrastructure Pipeline of about A$250 billion (FY 2025-2029) with a notable 14% rise from the previous year’s plan.9 This is different from the MPS projects, which are primarily funded privately.

Table 1. Australia’s major public infrastructure pipeline (FY2024–25 to 2028–29)10

Category | Projected 5-Year Investment | Share of Total Pipeline |

Transport (roads, rail, ports, airports) | A$129 billion | 53% |

Buildings (housing, health, education) | A$77 billion | 32% |

Utilities (energy, water, telecom) | A$36 billion | 15% |

**Total Major Public Infrastructure Pipeline | A$242 billion | 100% |

However, public finances are strained (as much as private finances are, more on this below) and are under the pressure in the wake of the spending during the pandemic. 50 federally funded projects were cut as a result of an independent review in 2023.11 Australia’s unique advantage is the private interest in building such critical infrastructure.

Critically, there is substantial room to improve productivity in infrastructure delivery. The wider construction and infrastructure sector accounts for around 9% of Australia’s GDP and over 1 million jobs,12 but its productivity performance has stagnated for decades.13 Complex approval processes, costly tendering, skill shortages, and low adoption of new technologies have kept construction productivity growth flat or declining even as other industries advanced.14 The Institution of Civil Engineers notes that “stagnant productivity…does not appear to be improving” and points to a need for systemic reforms in project selection, delivery models, and innovation adoption. One analysis by Oxford Economics estimates that raising Australia’s construction productivity to the economy-wide average could unlock an extra A$56 billion in capacity each year, equivalent to over 1,000 new schools or 10,000 km of roads annually.15 Clearly, maximizing the impact of every infrastructure dollar is as important as raising more dollars.

Another critical need is building Australia’s datacentres and related infrastructure for AI. Success in AI depends on investments in areas where Australia has a comparative advantage, mostly renewable energy. Australia is projected to reap annual productive gains of the tune of A$115 billion if investments in such critical infrastructure bear fruit.16

However, energy infrastructure is under pressure to transition toward renewables and to upgrade aging electricity grids. Digital infrastructure (broadband networks, 5G, datacentres) must expand to support a modern, technology-driven economy. Australia ranks 47th in the IMD World Competitiveness Index in efficiency of its energy infrastructure; a critical problem that must be addressed.

The real impediment: Higher rates and capacity constraints

There are evident gaps due to capacity constraints and higher interest rates across sectors. Our analysis finds that nearly 45% of the 27 MPS are facing delays. Of those, three projects with a combined capex of A$73 bn are delayed primarily due to difficulties in securing affordable finances, affecting nearly 6,000 jobs. Furthermore, six delayed projects with a combined capex of approximately A$108 bn have higher rates as a contributing factor. The list gets longer when we add capacity constraints to the list of contributing factors. The remaining delayed projects are affected by technical factors including regulation.

The rapid monetary tightening episode post-Covid hit the infrastructure industry hard and contributed to cost blowouts and delays, especially when combined with concurrent rises in material and labour costs. The cancelation of 50 projects worth A$7 bn was a result of such episodes. The Australian Constructors Association reported that construction firm insolvencies have climbed to more than double the rate of other industries, a trend attributed in part to contracting firms being squeezed by fixed-price contracts in an era of rising input and financing costs.17 Australia’s Productivity Commission has previously noted that poorly executed infrastructure projects – those delivered over-budget or late – can “financially burden the community for decades” with higher user costs and taxes.18 In short, an environment of expensive capital amplifies the importance of rigorous project selection, efficient delivery, and risk management, since the tolerance for material or labour cost overruns is much lower. Beyond cost impacts, a sustained period of high interest rates could have a more subtle but significant effect: dampening the overall rate of capital formation in Australia, including both public infrastructure and private business investment. The RBA itself has observed that slower growth in the capital stock per worker (i.e. less capital deepening) has been a contributor to Australia’s sluggish productivity growth in recent years.

What’s next?

All these concerns feed into the shorter-term debate on how far the RBA should go with hikes versus how much they should accommodate to help build the infrastructure needs. Solving these problems needs a broader scope than the RBA’s narrow mandate, but the RBA can play a crucial role at least around the financing needs. While we think the RBA has rightly taken a proactive stance against inflation due to the Middle East conflict, we also think they would do well to rapidly accommodate once inflation peaks and becomes more manageable. Most importantly, we think the time is approaching for a clear and sustained dialogue between the RBA, government (federal and state), and other key players including Infrastructure Australia and the construction industry. The objective of this dialogue would be coming up with a coordinated policy response to build momentum for infrastructure.

Investment implications

The near‑term inflation and interest‑rate uncertainty in Australia, exacerbated by the Iran war, has tightened financing conditions and increased execution risk across infrastructure. However, these cyclical headwinds do not diminish the long‑term investment case. Australia’s infrastructure shortfall—across transport, housing, energy networks and digital infrastructure—remains a constraint on productivity and growth. For long‑horizon investors, infrastructure continues to offer a compelling combination of defensive cash‑flow characteristics today and structural growth optionality over the medium term, with private capital increasingly critical in partnering with stretched public finances.

In the short term there is considerable uncertainty about the timing of the resolution of the conflict and the resultant investment impacts. It would therefore be prudent to ensure sufficient portfolio hedges to weather a deeper or more sustained oil supply shock. To that end we would recommend increasing allocations to fixed income, particularly floating rate notes – which provide some offset to the RBA’s rate hikes while also providing a hedge for equity exposures. Gold allocations should also be considered with geopolitical tensions likely to remain high for the foreseeable future.