Insights

The Impact of Crisis-Driven Dividend Cuts

The ramifications of dividend adjustments have been felt up and down the cap spectrum.

The adjustments also underscore the differences between dividend-focused ETF strategy methodologies and why performance may be diverging in our current environment.

With a global pandemic impacting consumer demand and corporate operating models, company cash flow trends have been altered. Some firms have cancelled their dividends to preserve capital to maintain staffing levels, support their workers or meet other operating expenses (i.e., debt service). Others have been forced to suspend dividends, as well as buybacks, as a result of receiving support from the US government under the CARES Act legislation.1

Either way, the ramifications of dividend adjustments have been felt up and down the cap spectrum, with more noticeable trends in certain sectors, irrespective of the size of the company. The adjustments also underscore the differences between dividend-focused ETF strategy methodologies and why performance may be diverging in our current environment.

Broad market dividend data

To facilitate the current dividend trend analysis, companies within the S&P Composite 1500 Index were analyzed and segmented by their respective market cap ranges: large cap (S&P 500), mid cap (S&P 400), and small cap (S&P 600). Any firm where the most recent or projected2 dividend is lower than its prior four-quarter average was counted as a decrease. Suspensions and omissions were much easier to identify, as a dividend was no longer published.

For the S&P 1500, 84 firms have suspended their dividend, roughly 6% of all firms. The actual weight of those firms represents just 1% of the S&P 1500’s market value, as many are small-cap firms. The table below depicts the breakdown for the broader market and the different size segments. Small-cap firms, where 4% of the S&P 600’s market cap has cut their dividend, lead all segments.

Market Cap Breakdown of Dividend Cuts

All-Cap |

Large-Cap |

Mid-Cap |

Small-Cap |

|

Action Type |

S&P 1500 |

S&P 500 |

S&P 400 |

S&P 600 |

Suspended |

84 |

17 |

19 |

48 |

Decreased |

34 |

20 |

10 |

11 |

Total Stocks in Exposure |

1,506 |

505 |

400 |

601 |

Suspended % of Stocks |

6% |

3% |

5% |

8% |

Suspended % of Exposure Market Cap |

1% |

1% |

3% |

4% |

Source: Bloomberg Finance L.P. as of 04/16/2020, calculations by SPDR Americas Research. Total number of stocks are more than 1500, 500, and 600 as a result of dual share class structures.

The greater number of dividend cuts further down the cap spectrum is not surprising. Large-cap stocks, with the stability that comes with mature multinational businesses with diverse revenue sources, may have more reliable cash flows.

Small-cap stocks, however, are unproven, have less consistent cash flows and are also more levered, as measured by net-debt-to-EBITDA ratios.3 But they do offer the potential for further expansion and market penetration if and when growth returns. And mid caps offer a unique combination -- of the managerial maturity associated with large caps and the operational growth of small caps. As you might expect, the number of dividend cuts for mid caps sit in the middle of large caps and small caps.

Sector biases across cap spectrums

Breaking out the dividend actions by sector provides additional context into the current trends; no matter the size segment, Consumer Discretionary stocks had the most suspensions. At the industry level within Consumer Discretionary, the suspensions were driven by Hotels, Restaurants, Leisure, and Specialty Retail. This is no surprise, given the economic fallout from most of the country sheltering in place on businesses that rely heavily on consumer spending. Another interesting trend within Consumer Discretionary is that some large-cap firms, as a result of their likely more stable footing versus their small-cap peers, just decreased, rather than cancelled their dividend.

The depth of cuts within small caps is more apparent when breaking it out by sector, as the small-cap Utility sector is the only small-cap segment not to have a firm suspend their dividend. Across the market-cap spectrums, however, the more defensive noncyclical Consumer Staples sector fared the best – alongside Utilities and Health Care.

Discipline’s impact on dividend strategies

There are over 100 US-listed ETF strategies4 focused on dividend-paying equities, each with its own index methodology and screening process for inclusion. Some strategies focus on yield, while others first screen for dividend growth. Firms with consistent dividend growth over many different market cycles depict an aspect of capital discipline, more reliable cash flows, and more durable balance sheets relative to just pure high-yielding stocks.

In a bull market, those differences are less of a concern if all you are after is yield. However, in a bear market brought on by an exogenous crisis, today’s high yield might be gone tomorrow if cash flows are constrained – and that high dividend is cut to preserve capital.

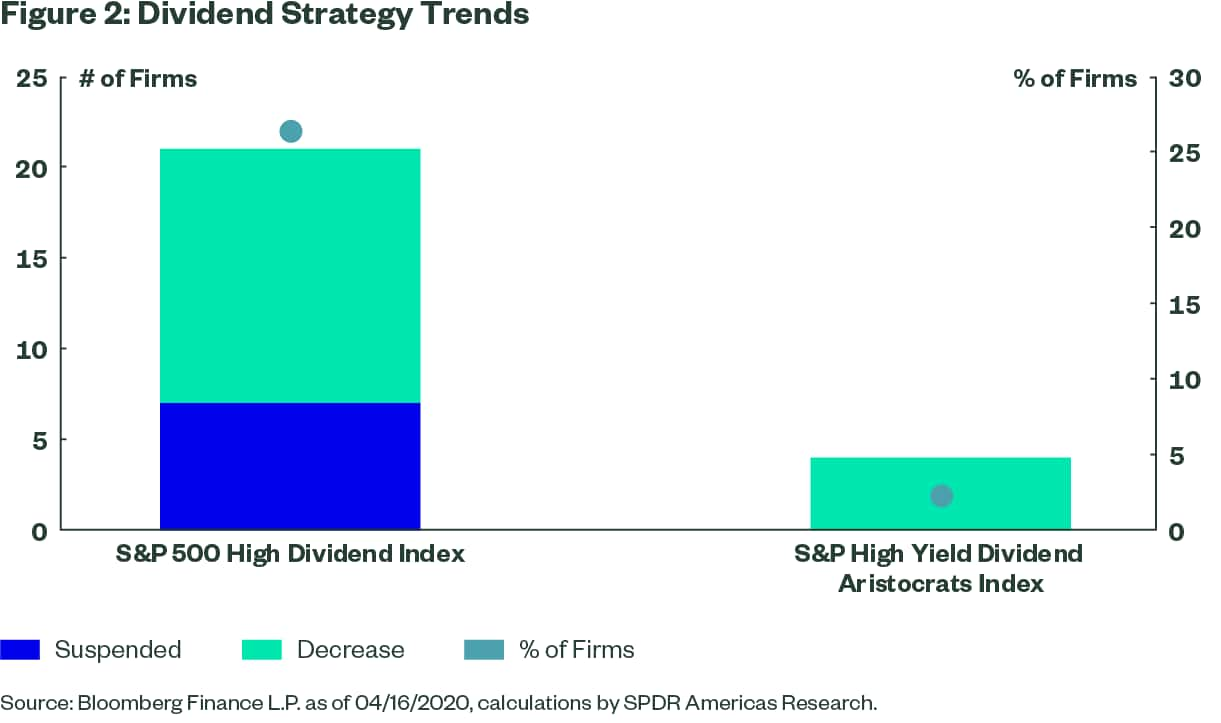

That is exactly what we found when we compared the dividend trends of the constituents of the S&P 500 High Yield Dividend Index (high dividend payers) with the S&P High Yield Dividend Aristocrats Index (dividend growers). The latter includes only firms that have increased their dividend for 20 consecutive years. As shown below, the high dividend yield-focused S&P 500 High Dividend exposure has had nearly a quarter of its holdings either suspend or decrease their dividend since the beginning of March. Conversely, as of now, no “aristocrat” firm has had to suspend its dividend. Only four have decreased their most recent dividend and are, therefore, at risk of being removed if they are unable to reverse course and raise their dividend later in the year.

As shown below, not surprisingly, the dividend strategy with more capital discipline (dividend growers), while down on the year, is down less than the exposure that does not have any fundamental screen (dividend payers),even though they both are focused within the same “style” of dividend-paying firms. From a broader market perspective, capital discipline has been noticeably rewarded in our current environment, as could be expected.

Dividend details in the days ahead

In today’s fast-paced news cycle, reliable information remains the key to decision-making. These dividend figures are likely to change as more firms report quarterly earnings and the depth of the impact of the COVID-19 pandemic is felt in our local economies and businesses of all sizes. We will continue to monitor the situation and provide the data-driven information you need to make sense of a very complex and uncertain time.