Aligning emerging market equity allocations with growth and dollar cycles

Explore the historical relationship between emerging market growth differentials versus developed markets and US dollar cycles—and how these macro forces can help inform strategic emerging market allocation decisions.

Emerging markets (EM) have long held a compelling place in global portfolios. Younger demographics, rising consumption, rapid urbanization, and structurally faster economic growth built a powerful long-term investment case. For many investors, the expectation has been straightforward: stronger economic growth should eventually translate into stronger equity returns.

But post-global financial crisis (GFC) outcomes have challenged that assumption. Despite economic expansion, EM equities have underperformed developed markets for much of the post-GFC period.

What explains the disconnect?

Growth alone wasn’t enough—what mattered was how growth interacted with the broader macro environment.

In fact, two variables have tended to play an important role over longer cycles:

- EM growth advantage vs. developed markets

- Direction of the US dollar

Historically, EM has outperformed when stronger relative growth and a weaker US dollar have aligned. When they move in opposite directions, outcomes have been more challenged.

This dynamic provides a useful framework for investors considering EM positioning as macro conditions evolve.

Growth and dollar cycles shape EM outcomes

Macro trends tend to evolve gradually, and turning points are often identifiable with confidence only in retrospect. Importantly, this analysis is not intended as a precise forecasting tool. Rather than attempting to predict near-term market movements, the objective is to offer investors a lens through which to assess whether macro conditions are favorable or less supportive for EM relative performance over longer horizons.

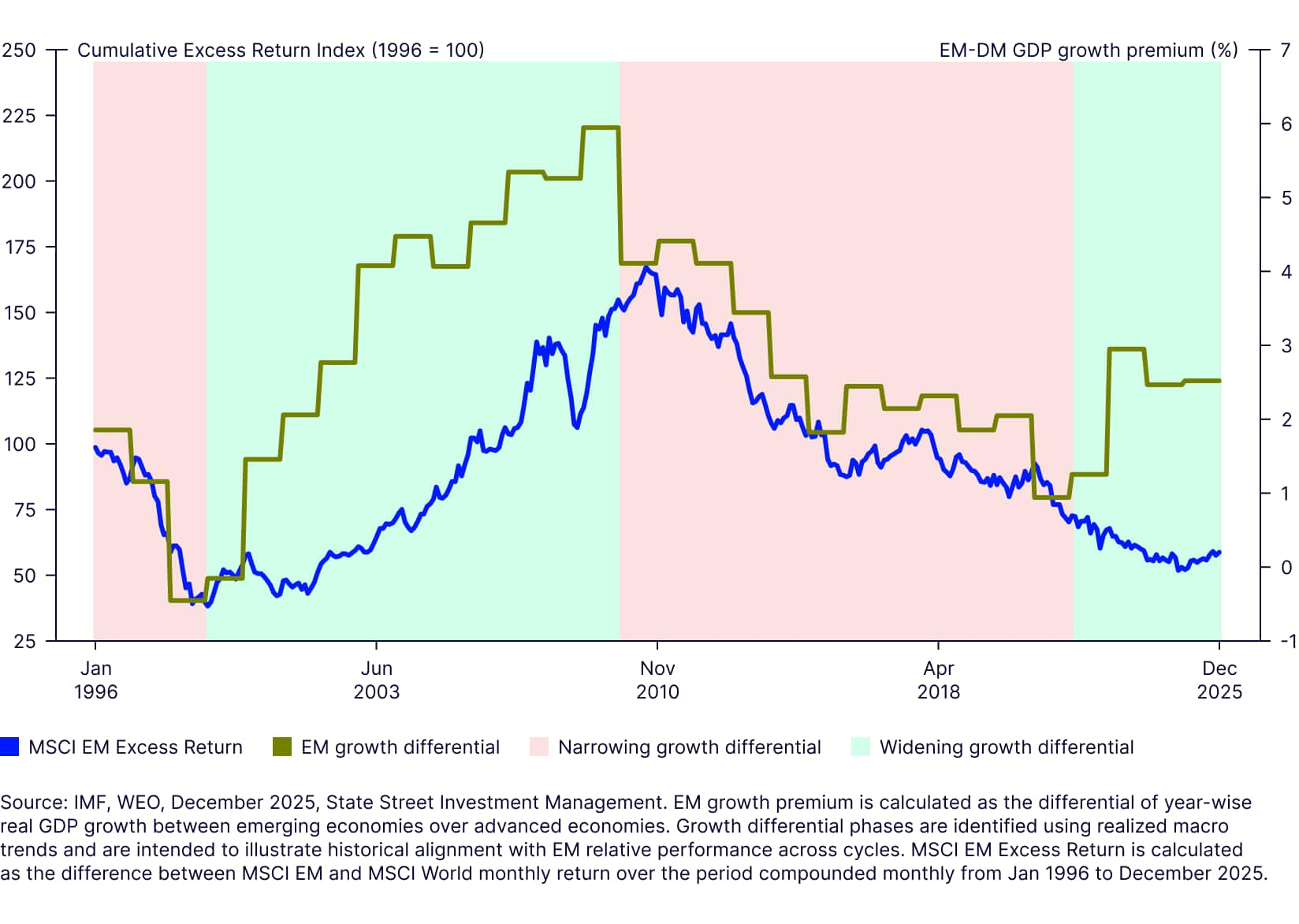

When EM growth leads, relative returns tend to follow

Economic growth is generally viewed as a fundamental driver of equity market performance, as it supports corporate revenue and earnings growth, which underpin long-term returns. While the transmission from macroeconomic growth to corporate earnings is neither perfect nor uniform across economies—reflecting differences in economic and market composition, global nature of corporate revenue streams, and the impact of share dilution over time—stronger growth conditions have generally supported a more favorable backdrop for earnings and equity returns over time.

For relative equity performance—EM equities excess return over developed market (DM] equities—the relative growth differential (EM growth premium over DM) becomes relevant. Periods where this differential widened have tended to align with stronger EM relative equity performance, while periods of narrowing differentials often coincided with weaker outcomes (Figure 1).

Figure 1: Economic growth differential and EM relative performance

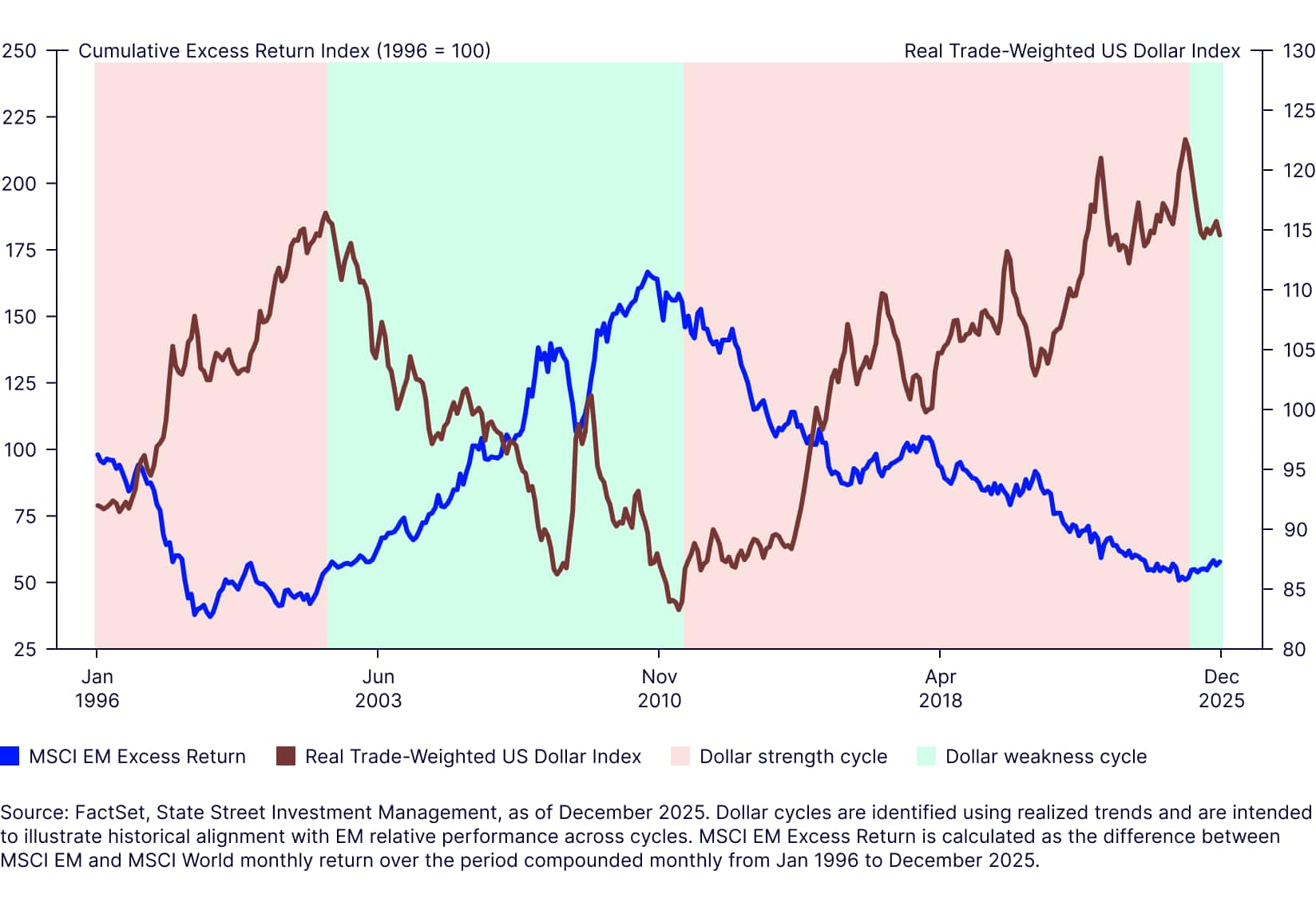

When the US dollar weakens, EM equity relative performance tends to strengthen

EM equity relative performance has historically tended to weaken during periods of broad US dollar appreciation, reflecting the close relationship between dollar cycles and global financial conditions. And a weaker dollar has historically supported EM relative returns (Figure 2).

Currency appreciation has often improved EM returns in US dollar terms, while weaker dollar environments have often coincided with stronger global liquidity, improving financial conditions, and greater investor willingness to allocate toward higher-beta markets; conversely, periods of dollar strength frequently aligned with tighter liquidity conditions and more challenging environments for EM assets.

Figure 2: Dollar cycle and EM relative performance

Focus on the interaction of EM growth and the dollar cycle

Neither growth nor the dollar cycle alone explain EM outcomes—but together, they define the macro backdrop for EM relative performance across cycles.

Viewed through a lens of a discounted cash flow framework,1 relative growth dynamics influence the earnings and cash flow outlook for emerging markets relative to developed peers, while dollar cycles influence the financial conditions, investor sentiment, and risk premia through which those future cash flows are discounted. While the two variables can influence one another across cycles,2 they do not always move in tandem.

The strongest periods of EM relative performance historically have been often associated with environments in which both forces were aligned in a supportive direction—when emerging market growth was strengthening relative to developed economies while the dollar environment simultaneously became more favorable, like 2002/03-2009/12 and 2025/02-2025/12 (Figure 3).

By contrast, periods in which both variables moved in a less favorable direction have generally been accompanied by weaker EM relative outcomes (like 1996/01-1998/12 and 2011/08-2021/12). Outcomes in more mixed environments have been less uniform. Periods of strong relative growth alongside dollar strength or dollar weakness alongside a narrowing EM growth advantage have not consistently delivered the same degree of relative outperformance.

Figure 3: Macro scenarios and EM relative performance

| 1996-2025 | Macro environment | Annualized return | Excess annualized return | |||

|---|---|---|---|---|---|---|

| Start date | End date | Dollar cycle | GDP differential cycle | EM | DM | EM-DM |

| 1996/01 | 1998/12 | Strengthening | Narrowing | -11.2% | 18.2% | -29.5% |

| 1999/01 | 2002/02 | Strengthening | Widening | 5.5% | -4.1% | 9.6% |

| 2002/03 | 2009/12 | Weakening | Widening | 18.1% | 5.0% | 13.1% |

| 2010/01 | 2011/07 | Weakening | Narrowing | 12.2% | 10.1% | 2.0% |

| 2011/08 | 2021/12 | Strengthening | Narrowing | 3.5% | 11.8% | -8.3% |

| 2022/01 | 2025/01 | Strengthening | Widening | -0.9% | 7.9% | -8.7% |

| 2025/02 | 2025/12 | Weakening | Widening | 35.3% | 19.2% | 16.2% |

Source: FactSet, State Street Investment Management, as of December 2025. Figures are annualized for periods longer than one year. Returns are annualized. Excess annualized returns show the emerging market relative performance over developed market. Combined growth and dollar phases are based on the interaction between growth differentials and dollar cycle, identified using realized macro trends to illustrate historical alignment with EM relative performance across cycles.

It’s important to note that the two drivers don’t explain every period of EM performance. Valuations, geopolitics, policy decisions, sector composition, and country-specific developments all matter. But over long cycles, growth differentials and dollar conditions may provide investors with a useful lens for positioning EM exposure within a global portfolio context.

Position EM with the cycle, not against it

For many investors, benchmark representation remains a reasonable starting point for long-term EM exposure, with the precise allocation reflecting a combination of return objectives, diversification needs, risk tolerance, or regulatory constraints.

This strategic allocation can serve as a policy-neutral anchor, with macro conditions informing measured positioning around that baseline.3

Periods where both growth differentials and dollar conditions aligned favorably historically tended to justify greater confidence in EM allocations, while periods where both moved unfavorably often warranted greater caution. Mixed environments may justify allocations closer to strategic neutral.

Importantly, these variables tend to evolve over medium-to-long horizons rather than short tactical windows. While identifying turning points in real time remains inherently difficult, the persistence of these factors means alignment can still matter meaningfully for medium-to-long-term allocation decisions once broader trends become established. Investors having strong convictions on the direction of these variables can align earlier to take advantage.

For investors navigating increasingly complex global markets, considering EM exposure through this dual macro lens may offer a more flexible approach than maintaining a uniform allocation across differing market conditions.