US–China trade truce holds, but for how long?

President Trump’s recent China visit suggests the trade-war pause will hold, but normalization remains unlikely as China’s manufacturing dominance grows. Meanwhile, its ballooning surplus risks new trade conflicts.

A year after the “Liberation Day” tariffs, the US–China trade relationship looks more peaceful than many expected. The constraints of mutual dependence have proven strong enough for both parties to keep the current trade-war ceasefire. President Trump’s recent Beijing visit reinforced that impression, with both sides agreeing to build a “relationship of strategic stability.”

Nevertheless, so long as China perpetuates its overdependence on external demand, this can only be a stalemate, not a true end of hostilities. Other countries, meanwhile, may become more active in seeking to counter China’s manufacturing dominance.

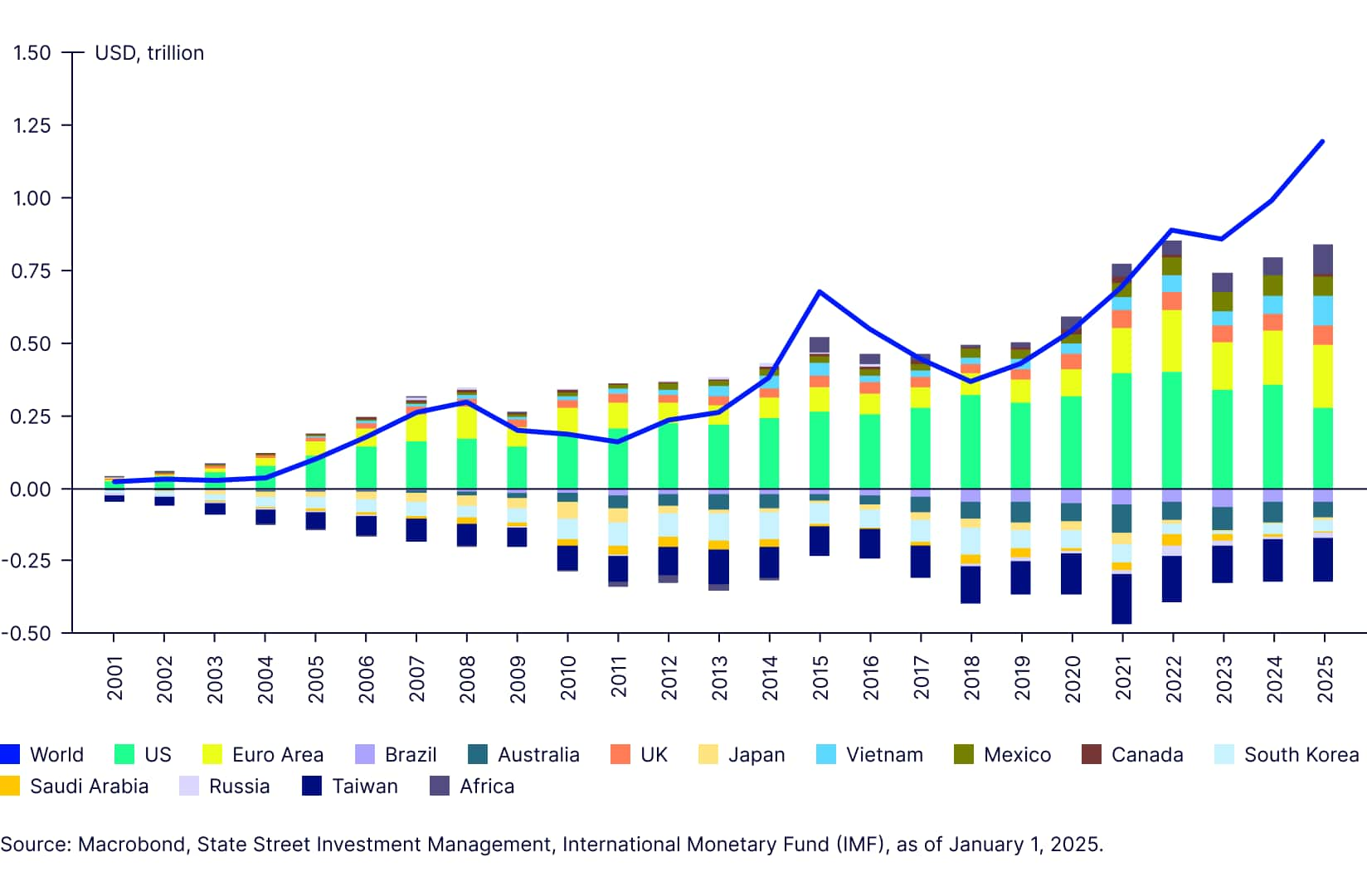

Imbalances continue to widen

Despite headwinds from US tariffs, China’s 2025 trade and current account surpluses as a share of China's gross domestic product (GDP) reached their highest level since 2009 (Figure 1).

When assessed against global ex-China GDP (to adjust for China’s growing weight in the world economy), the imbalance looks even starker. Last year, the rest of the world ran a trade deficit with China equivalent to 0.8% of its combined GDP, a new record high (Figure 2). By comparison, at the peak of Japan’s manufacturing dominance, the rest of the world’s trade deficit with Japan reached a one-time peak of 0.6% in 1986.

China’s domestic demand deficit

China’s external surpluses are the combined result of both its impressive manufacturing prowess, on one hand, and its languishing domestic demand, on the other. Indeed, while China’s growth rate has been relatively stable around 5% over the last several years, trade has accounted for a larger share of that growth than had been the case pre-Covid. With the property sector still languishing, consumer spending seems unlikely to rebound meaningfully. If so, Chinese growth will either naturally moderate further, or external demand will have to continue to act as a bridge.

China’s external surpluses are problematic

While this dynamic can temporarily work, if prolonged, it could become an existential threat to China’s trading partners’ manufacturing ambitions. The modest (though uneven) decrease in China’s external imbalances that characterized the second half of the last decade has more than reversed. Despite stated intentions to reorient the economy towards domestic demand, there is no compelling evidence that this is occurring. Instead, the data suggests a geographical redistribution of a growing imbalance across a wider group of economies (Figure 3).

Figure 4: China's trade balance with select trading partners

Is Europe the next front?

While China’s trade surplus with the US has indeed shrunk greatly in recent years, its trade surplus with the Eurozone has more than doubled since 2020 (from USD 95 bn to 216 bn). The relative shift is even starker. In 2020, China’s trade surplus with the US was more than three times the size of its surplus with the Eurozone; by 2022, it was roughly twice as large. Last year, it was just 30% larger.

This is an extraordinary shift that does not appear to receive sufficient attention in European capitals, nor, for that matter, in many other capitals around the world.

On current trends, an EU–China trade war seems only a matter of time, though it may still take a while to snowball. Geopolitical fracturing means more reliance on domestic/regional demand everywhere. The US is a more closed economy than a decade ago, and Europe will have to follow suit.