Implementation alpha across the fixed income spectrum

Implementation alpha is the cumulative benefit of systematic, risk‑aware security selection decisions that reduce cost drag and capture micro‑inefficiencies, while always preserving close benchmark alignment. Index investing in fixed income lends itself well to capturing such benefits—effective indexing in this asset class is anything but passive. The market’s fragmented nature, over the counter (OTC) trading, and variable security‑level liquidity create persistent implementation frictions that provide repeatable opportunities for sophisticated fixed income managers to offset them. However, capturing this alpha is not just limited to indexed investing.

The same core toolkit (risk decomposition, proactive and pragmatic sampling, trading effectiveness) can be scaled along a spectrum as follows: (i) Indexing focuses purely on efficiency and outcome certainty; (ii) Enhanced indexing adds a small yet purposeful risk budget that seeks to generate incremental excess returns; and (iii) Active/systematic active uses an explicit risk budget to maximize alpha, net of costs.

In practice, the opportunity set varies by sector. In sovereign bonds, where liquidity is high, disciplined execution and index event management can add approximately zero-to-five basis points (bps) of implementation alpha. In investment-grade credit, where greater fragmentation and liquidity premia persist, a well-run process that pragmatically and proactively manages the exposure, can add 5–15 bps (annualized) over a full market cycle. As fixed income exposures become more complex from an idiosyncratic and liquidity perspective, the “appropriate” implementation approach shifts away from higher replication toward greater sampling. A sampling approach is highly informed by increasing breadth and frequency of data, as well as by more tailored trading and execution approaches/trading plans.

Why fixed income indexing creates opportunities for Implementation Alpha

Bond markets differ from equity markets. Unlike equities, the same issuer typically has many bonds with different coupons, maturities, and liquidity profiles; trading is decentralized and largely OTC in nature; and liquidity is time‑varying at the security level. These features make full index replication either impractical or uneconomic in many fixed income exposures and create the need for a pragmatic approach to portfolio construction.

This presents challenges and opportunities for fixed income investors—from both portfolio construction and exposure management perspective. These are as important to index managers as they are to active managers, despite them operating under very different objectives and constraints. When properly understood and controlled, these market features can be exploited very effectively by index managers to target highly reliable sources of incremental excess returns, or what we at State Street Investment Management call our ‘implementation alpha’.

The Implementation alpha spectrum: Indexing → Enhanced → Active

Rather than treating implementation alpha as a single concept, it is more useful to place it on a spectrum defined by objectives and constraints. The key difference is not whether the process is systematic (it often is across the spectrum), but how much risk budget is deliberately allocated and how it is utilised. In moving across this spectrum from indexing through enhanced to active, the portfolio construction “dial” typically turns depending on a number of factors:

- how significantly you sample versus replication;

- how explicitly you allow security‑level deviations, based on perceived relative value and systematic selection;

- how you translate implementation insights into deliberate, well-rewarded risk-taking (high information ratios).

Figure 1: Defining characteristics on the spectrum

Dimension | Indexing | Enhanced | Active / Systematic Active |

Investor goal | Efficient benchmark exposure with minimal outcome uncertainty | Benchmark returns after costs, with potential for additional excess | Maximize excess returns vs benchmark or liabilities |

Investment objective | Track benchmark as closely as possible, after implementation costs | Deliver consistent incremental excess return over benchmark | Maximize alpha within a defined risk budget |

Benchmark alignment | Tight Benchmark‑neutral positioning across all risk dimensions | Close Benchmark‑aware with marginal latitude to add implementation alpha | Loose Benchmark is a reference exposure |

Risk budget | Very low Primarily to enable efficient sampling | Low Used purposefully to exploit inefficiencies to add incremental excess returns | Medium to high Explicitly allocated and intentionally utilized |

Trading objective | Minimize absolute transaction costs | Maximize incremental value after trading costs | Maximize expected alpha net of costs |

Source: State Street Investment as of May 25, 2026. For illustrative purposes only.

How sampling and portfolio construction change across the spectrum

To mitigate the shortcomings of full replication, sophisticated fixed income index managers such as State Street have traditionally employed a top-down portfolio construction approach known as stratified sampling. However, at some stage in the process, the index manager—like an active manager— has to make bottom-up security selection decisions. While the degrees of freedom are typically narrow (and vary by exposure), they are intended to provide sufficient latitude for an experienced investment manager to add incremental value through implementation alpha, helping to offset the inherent costs of managing the exposure. The question then becomes: how should a portfolio manager think about these degrees of freedom across the spectrum, and what do they entail in practice?

Core indexing: Stratified sampling plus disciplined implementation

In core indexing, the objective is to deliver benchmark beta as efficiently as possible. Stratified sampling decomposes the benchmark into its key risk dimensions “buckets”—currency, duration/curve, sector, rating/quality, etc.—and selects a representative set of bonds to match those risk exposures within reasonably tight tolerances. The portfolio manager’s latitude is intentionally narrow and is primarily used to manage liquidity and turnover, avoid uneconomic bonds, and handle index events prudently and pragmatically.

Enhanced indexing: Active sampling around the index

Enhanced indexing uses the same risk decomposition foundation, but allocates a small yet deliberate risk budget to seek to systematically improve returns. The key shift is that security selection is no longer only flow driven and risk-neutral; instead, it becomes essentially active sampling around index constituents—tilting toward better liquidity, better relative value, and more attractive carry/roll opportunities while remaining very benchmark aware. This typically requires additional data inputs and a more systematic portfolio construction approach and trading decisions by the portfolio management team.

Active/Systematic active: Explicit risk budgets, broader opportunity sets

At State Street Investment Management, we think of systematic active as active portfolio management delivered within clearly defined—and tightly governed—risk constraints. As you move along the spectrum from indexing to enhanced and into active, the portfolio manager’s role expands from implementing benchmark exposure efficiently to deliberately allocating risk in pursuit of alpha. On the active end of the spectrum, risk is an explicit input, not just a limit: the strategy operates with a stated tracking-error budget that is intentionally deployed across compensated sources of return. Security selection and, where applicable, macro positioning are used to maximize expected alpha (net of costs), with position sizes, factor exposures, and liquidity—all managed on a holistic basis. Implementation discipline remains essential, but the portfolio construction problem shifts from efficient benchmark alignment to now optimizing the trade-offs between expected return, cost, and risk.

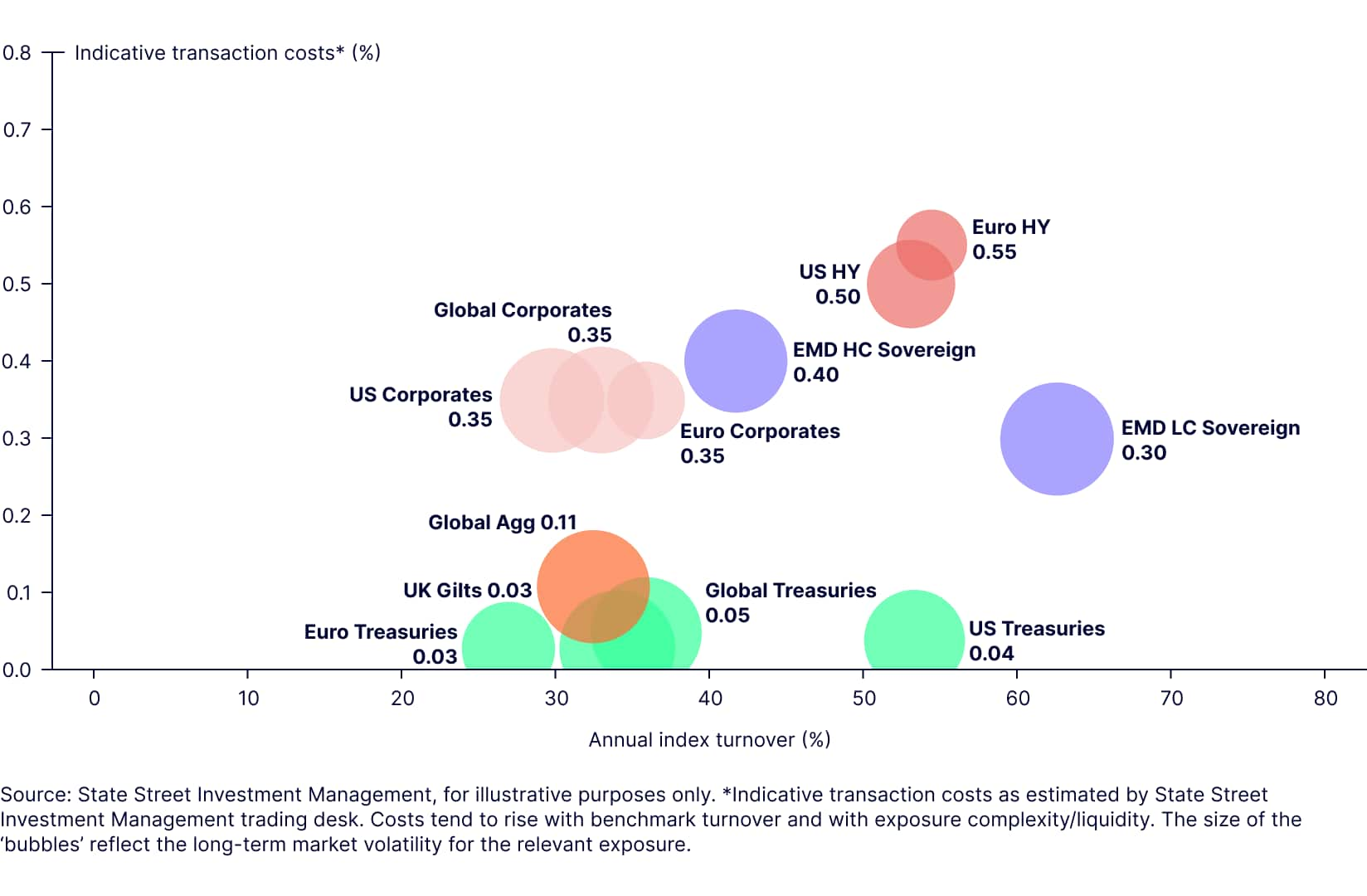

As market complexity increases, turnover and transaction costs become a more binding constraint—making portfolio construction and trading discipline increasingly important. In more liquid, homogeneous sectors, a tight benchmark-aware process can deliver the objective efficiently and reliably. As you move into more fragmented and liquidity-challenged sectors such as high yield and emerging market debt, the same index outcome can require materially more expensive trading—and consequently a very different implementation playbook. Figure 2 summarizes why the spectrum framework matters in practice.

Figure 2: Navigating complexity: turnover and trading costs vary by sector

For portfolio managers, the implication is that “tracking the index” is not a uniform task across sectors: the marginal cost of precision rises as turnover increases and liquidity declines. This is where stratified sampling, index-event management, and security-selection discipline become differentiators in core indexing. Moreover, a modest and deliberate risk budget in enhanced strategies can be used to improve net outcomes (for example, by avoiding forced trades or harvesting carry/roll), while remaining benchmark-aware.

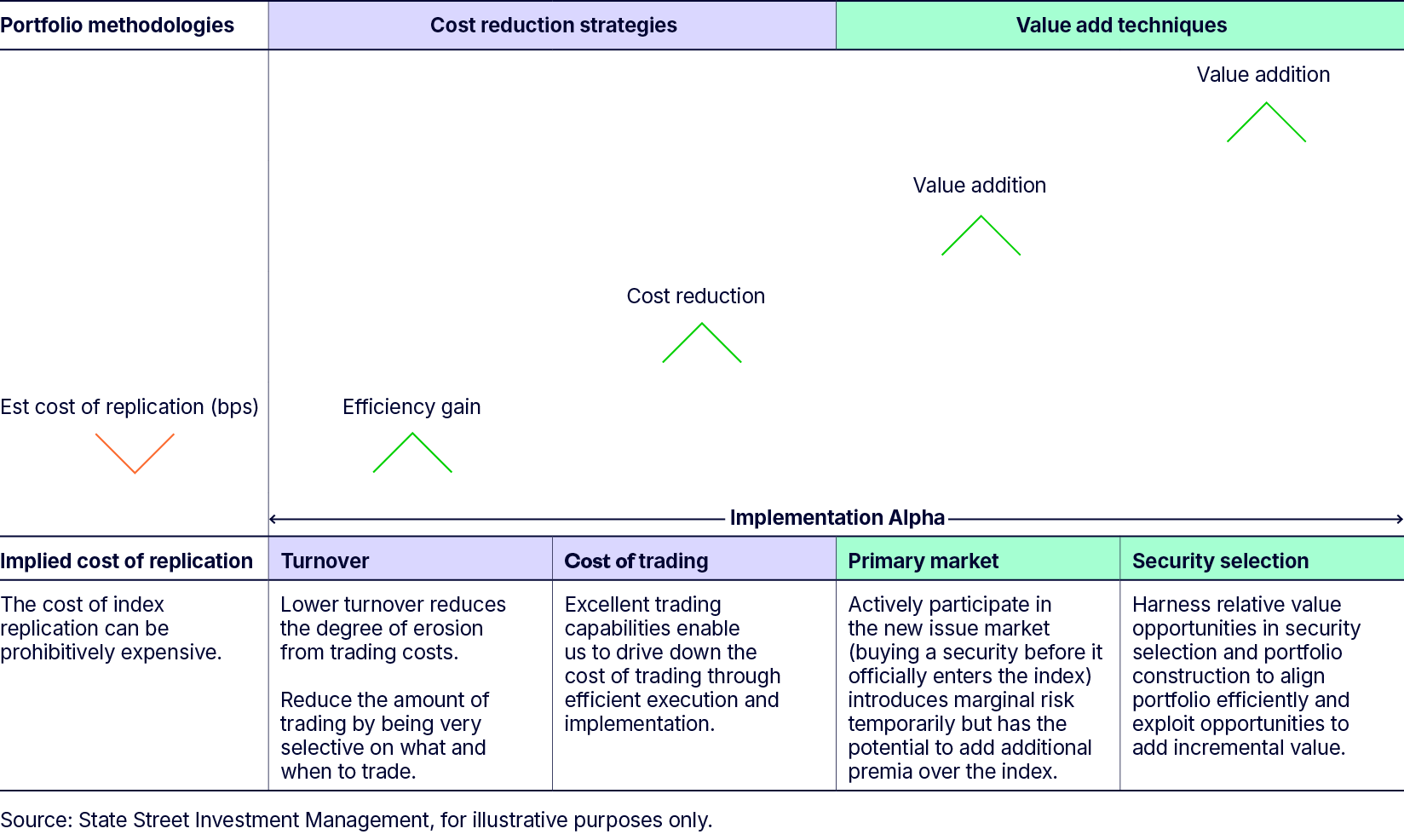

The implementation alpha toolkit (and its position on the spectrum)

1. Cost-reduction strategies

Reducing drag from transaction costs (and implied cost of replication)

The first source of “value” is in fact cost management: in fixed income, full replication is often impractical or uneconomic because liquidity varies materially by bond and through time, and turnover can be meaningfully higher in more complex sectors (e.g., credit and emerging markets). A pragmatic implementation approach therefore focuses on reducing the implied cost of replication by (i) minimizing unnecessary turnover (including being deliberate about when to trade and when not to trade and, where appropriate, retaining bonds that may have fallen out of the index, when doing so preserves risk alignment, reduces cost and therefore improves net outcomes); (ii) staging and timing rebalances to avoid forced trading windows; and (iii) maximizing execution quality by adapting trading protocol depending on the situation - via dealer axes, counterparty competition, and the use of electronic venues where suitable. A decentralised trading model with regional hubs also ensures local price discovery and execution in local time zones where liquidity can be highest, while diversified and granular index flows can improve our ability to transact inside the full market bid/offer. Together, these techniques and disciplines seek to reduce performance drag from transaction-cost while maintaining tight and efficient benchmark alignment.

2. Value-add techniques

Harvesting structural market premia (primary market)

New issue participation can be both a cost-efficient way to gain exposure and a source of excess return. For index portfolios, participation is typically framed as the cheapest route to gaining benchmark exposure. For enhanced and active strategies, the latitude to increase participation is provided where the expected new issue premium is attractive and within the risk budget.

Systematic, informed, and risk-aware security selection

Even within tight index constraints, managers must select which bonds to own and not to own. An effective and efficient approach is to prioritize bonds as follows:

- Core holdings: largest contributors to tracking error due to size or volatility

- Semi‑core holdings: medium contributors to tracking error but desire to substitute and proxy between names

- Non‑core holdings: low contributors to tracking error, low need to own, and used for fine‑tuning portfolio exposures.

Liquidity metrics are key in determining the above, along with relative value indicators to establish when the marginal tracking error reduction is worth the marginal trading cost.

Proactive index event management

Upgrades/downgrades, corporate actions, and maturity roll‑down can create forced‑trade pressure. Proactive management—crossing where possible, staging trades intra‑month, and avoiding congested month‑end windows in illiquid sectors—help reduce cost drag while pragmatically preserving benchmark alignment.

Figure 3: Implementation alpha in action

Scaling the process with data and technology

As index universes have expanded and security level data has become ubiquitous and along multiple dimensions (i.e., liquidity measures, risk factors, value signals, and sustainable investing metrics etc.), industrial‑scale portfolio construction tools and optimisation are increasingly required to maintain precision. Fixed income workflows today are generated and executed at increasing speed and efficiency, enabling faster, more consistent rebalancing—while keeping portfolio managers firmly in the driving seat for oversight, judgment and ultimate decision making.

The Bottom Line

The index-to-active spectrum is a helpful way to frame and understand the differences and appropriateness of each approach. Implementation alpha is real, scalable, and—when structured correctly—quite intuitive for investors. It is a systematic set of decisions that reduces the natural drag of fixed income implementation and captures persistent micro inefficiencies. Crucially, even a “passive” fixed income approach requires an active mindset as liquidity changes, index events creating forced trade pressure, and small security selection choices accumulate into meaningful outcomes over time.

The goal is not to eliminate discretion, but to apply it appropriately—using risk decomposition, disciplined sampling, and strong trading governance to make deliberate trade offs between tracking precision and total cost. The most effective way to communicate this is not as a single approach, but as a spectrum of portfolio construction choices and risk budgets, ranging from tight indexing through enhanced to active/systematic active. Clear definitions, disciplined governance, and the right data and trading infrastructure are what transform this from a concept into reliable investment results.

This paper is part of a broader Income, Engineered for Outcomes series.

➡ Visit the Fixed Income Hub to continue the series